I used to feel stressed by unexpected expenses without an emergency fund. But once I learned to build one, that anxiety disappeared. Now, I can handle car repairs, medical bills, and job loss without financial chaos or relying on credit cards.

Building an emergency fund has been transformative. Start today to protect yourself from financial stress and take control of your future. Let’s get started!

1. Assess Your Personal Finance

Before saving for your emergency fund, assess your financial situation. Gather bank statements, credit card bills, and other documents to track your income and expenses over a month or two. Focus on recurring bills like:

- Rent or mortgage

Auto loans

Credit card bills

Student loans

Utilities

Groceries

Transportation

Also, account for non-essential expenses like daily coffee, forgotten subscriptions, and impulsive purchases, as these can add up quickly.

After tracking your expenses, create a budget that separates your income, fixed bills, and flexible spending. In two 2021 experiments involving 685 participants, people who regularly reviewed their own spending-control strategies spent an average of $228 to $236 less over one month than those in the comparison groups.

A budget can provide a similar structure by showing where your money goes and helping you choose realistic areas to cut, although your actual savings will depend on your income and spending habits.

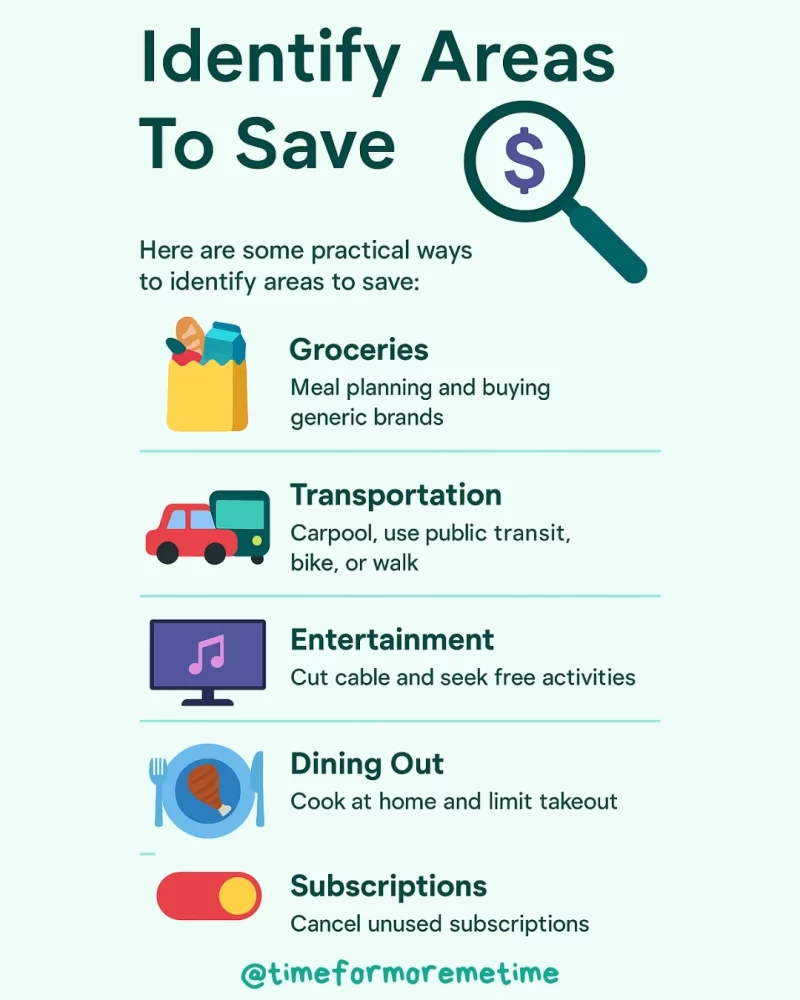

2. Identify Areas To Save

Understanding where your money goes is crucial for finding ways to cut back. Here are some key questions to consider:

- Are there recurring subscriptions you rarely use?

- Can you find more affordable options for groceries or your cell phone plan?

- Are you making purchases just to earn rewards?

Review your recurring charges and remove anything that no longer earns its place in your budget. US fitness members paid an average of $65 per month in 2023, so replacing an unused membership with home workouts or free community activities could redirect about $780 a year into your emergency fund.

Windfalls can move you forward faster since the average federal tax refund reached $3,276 as of May 8, 2026, and saving half would add $1,638 without affecting your monthly budget.

Here are some practical ways to identify areas to save:

- Groceries: Meal planning, buying generic brands, shopping at discount stores, and using credit card rewards can help reduce grocery costs.

- Transportation: Consider carpooling, using public transit, biking, or walking. These options save money and promote health.

- Entertainment: Cut cable TV, seek free or low-cost entertainment, or use cash gifts from credit card rewards for subscriptions.

- Dining Out: Cooking at home, limiting takeout, and planning meals can significantly reduce dining expenses.

- Subscriptions: Cancel unused subscriptions, explore cheaper alternatives, or limit yourself to one account to minimize these costs.

These things aren’t that difficult to do, right?

3. Choose The Right Savings Account

Selecting the right savings account is crucial for building your emergency fund. Consider both accessibility and growth potential. You need a secure place where your money can grow and be easily accessed in emergencies.

High-yield savings accounts are excellent options, offering security and better interest rates than traditional savings accounts. Money market accounts also provide competitive rates and allow limited check writing.

For example, with a $50,000 initial amount, a traditional savings account at 0.05% interest will yield an end-of-year balance of $50,025. Meanwhile, a high-yield with 4.50% interest will let you have $52,250 instead.

The difference is significant: a high-yield account earns $2,250 in interest compared to just $25 with a traditional account. And while it’s wise to keep a small amount of cash at home for minor emergencies, avoid storing large sums due to theft risk. Also, consider consulting a financial advisor to choose the best savings solution for your needs.

4. Make Direct Deposits Automatic

Saving often takes a backseat to other expenses, but in wealth management, your savings should come first—this is known as paying yourself first. To ensure you prioritize saving, set up automatic transfers to your emergency fund.

Treat saving like a bill you owe your future self, rather than waiting to see what remains after spending. A CFPB analysis of 127,243 savings goals found that scheduled deposits, such as transfers on payday or weekly, were associated with average savings of $167.84 per month, more than twice the $80.36 associated with purchase roundups.

Set an automatic transfer to your sinking fund after each payday, since even $50 from every biweekly paycheck would build $1,300 in one year.

5. Monitor And Adjust

After starting your savings, regularly check your progress and make adjustments as needed. Building an emergency fund is a marathon, not a sprint.

Be prepared for fluctuations in your expenses or unexpected windfalls, and adjust your automatic savings accordingly to keep your budget on track. Periodically review your cash flow statement, especially after significant life changes like a new job or salary increase.

This allows you to modify your automated transfers to either accelerate your savings or accommodate changes in income or spending. Regularly monitoring your financial cushion will also motivate you to stay committed to your savings goals.

FAQs

Before I end this post, let me tackle some frequently asked questions first.

What is the best way to create an emergency fund?

Begin by setting a clear savings goal. Next, identify areas where you can cut expenses and set up automatic transfers to a high-yield savings account. Additionally, look for opportunities to increase your income whenever possible.

Is $5,000 enough for an emergency fund?

An amount of $5,000 is a solid starting point for an emergency fund. While it may not cover all individual expenses, it should be sufficient for most common financial emergencies. Remember, starting with any amount is better than having nothing.

How can I build an emergency fund when money is tight?

Start with whatever you can afford, even if it’s a small amount. Over time, these small contributions will add up. As your financial situation improves, gradually increase your savings.

You can also explore additional income streams, such as freelancing or gig economy jobs, to boost your contributions directly to your emergency fund.

Conclusion

Now that you know how to build an emergency fund, it’s time to start. The initial adjustment may be challenging, but it will become satisfying over time. Remember, this isn’t just about saving money; it’s about achieving financial stability and gaining the confidence to handle unexpected situations while making smarter financial choices.

If you find this helpful, be sure to subscribe to our newsletter. Also, follow us on social media and check our videos on our YouTube channel!

Sources

- Photos: Unsplash: Josh Appel

- Journal of Experimental Social Psychology. (2021). Financial self-control strategy use: Generating personal strategies reduces spending more than learning expert strategies. https://doi.org/10.1016/j.jesp.2021.104189

- Health & Fitness Association. (2024). US fitness facility memberships reach the highest level ever as dues rise. https://www.healthandfitness.org/u-s-fitness-facility-memberships-reach-the-highest-level-ever-as-dues-rise/

- Internal Revenue Service. (2026). Filing season statistics for week ending May 8, 2026. https://www.irs.gov/newsroom/filing-season-statistics-for-week-ending-may-8-2026

- Consumer Financial Protection Bureau. (2022). Consumer savings app strategies and savings outcomes. https://files.consumerfinance.gov/f/documents/cfpb_qapital-savings-app-outcomes_report_2022.pdf