It’s the end of the month, and you looked at your numbers and still wondered why money felt tighter than it should. On paper, the budget worked. In real life, it didn’t feel that way.

That gap usually shows up quietly. Bills get paid, groceries get bought, and savings get nudged forward, yet something still feels off. Those moments often point to small budgeting details that stay hidden because they don’t trigger alarms or obvious mistakes.

That’s where these overlooked facts come in. Keep reading to learn about the cool family budgeting facts that many households miss and why these quiet details shape how family budgeting actually feels day to day. Let’s get started!

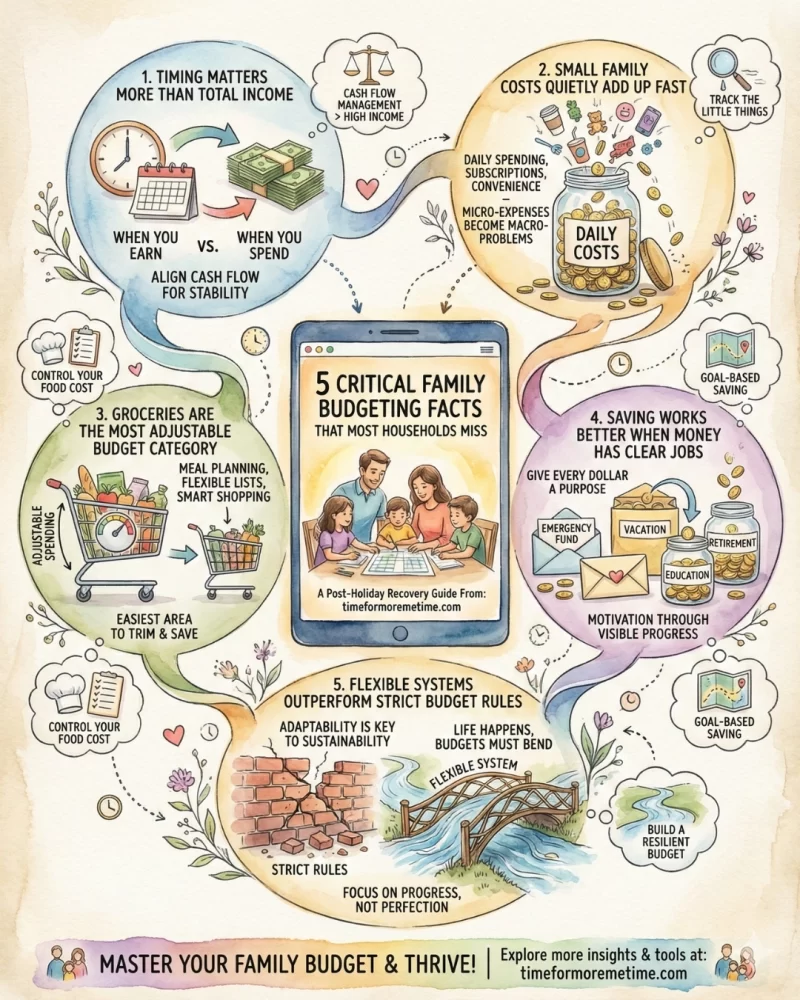

1. Timing Matters More Than Total Income

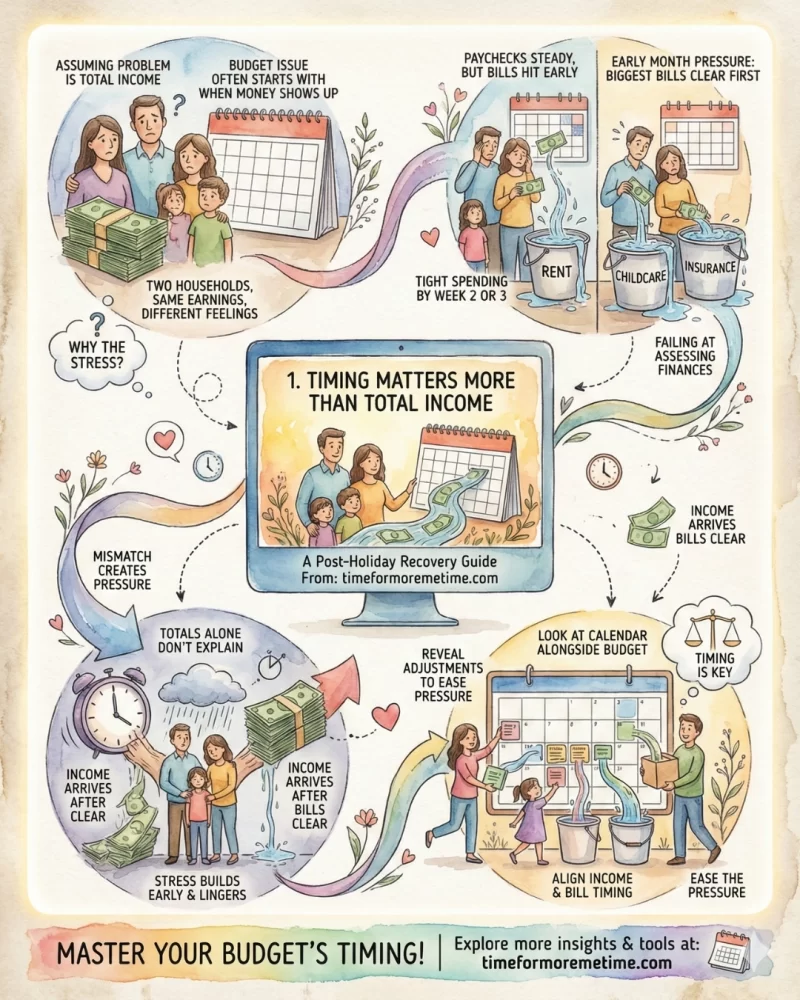

One thing that trips families up is assuming a budget problem always starts with how much money comes in. In reality, it often starts when that money shows up. Two households can earn the same amount and feel very different depending on timing.

I’ve watched my Buffalo neighbors back then deal with this without realizing what was happening. Their paychecks were steady, yet rent, childcare, and insurance all hit at the beginning of the month. By the second or third week, spending felt tight, even though the math worked out by the end. They were failing at assessing finances.

This mismatch creates pressure that totals alone don’t explain. When income arrives after the biggest bills clear, stress builds early and lingers. Looking at the calendar alongside the budget is often enough to reveal where adjustments would ease that pressure.

2. Small Family Costs Quietly Add Up Fast

Big expenses usually get all the attention. Rent gets planned for. Groceries get watched. Basic commodities get expensive. The trouble often starts with the smaller costs that feel harmless in the moment and easy to forget afterward.

My coworkers who were confident in their budgets still felt confused when savings stalled. It was never one big mistake. It was school fees, activity supplies, and quick purchases made during busy weeks. Each one made sense on its own, but together they slowly ate into the margin they thought they had.

That’s how these costs slip through. They don’t arrive loudly or demand a line item, so they rarely get questioned. What usually helps is going back over the last month and grouping those small expenses together. Seeing them side by side often explains where the pressure has been coming from.

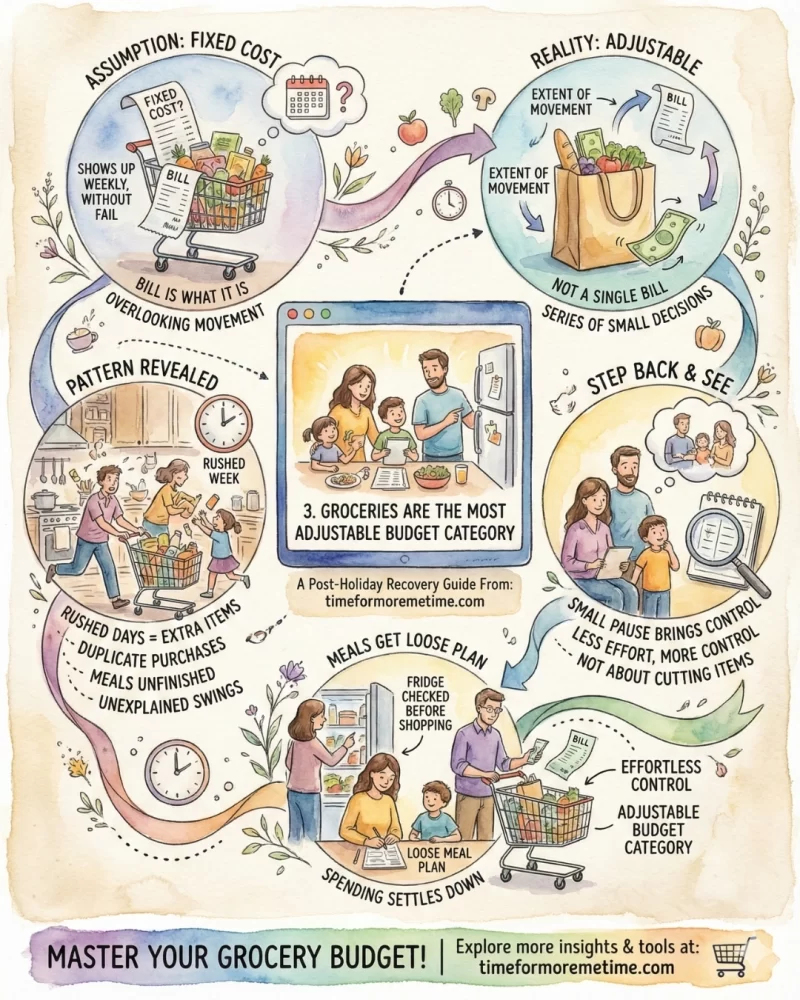

3. Groceries Are The Most Adjustable Budget Category

Groceries often feel like a fixed cost because they show up every week without fail. You buy food, you eat it, and the bill is what it is. That assumption makes it easy to overlook the extent of movement in this part of a family budget.

I noticed this pattern when I started comparing grocery totals from one week to the next and draw up a budget. When I’m done, I couldn’t explain the swings. We weren’t buying luxury items or changing how much we ate. The difference usually came down to how rushed the week felt. Busy days led to extra items in the cart, duplicate purchases, and meals that never quite got finished.

What tends to help is stepping back and seeing groceries less as a single bill and more as a series of small decisions. When meals get even a loose plan, and the fridge gets checked before shopping, spending often settles down without much effort. That small pause brings more control than cutting items ever did.

4. Saving Works Better When Money Has Clear Jobs

Saving often feels frustrating when everything goes into one place, and nothing seems to be moving. You see the balance grow a little, then shrink, then grow again, and it becomes hard to tell whether progress is actually happening. It’s really hard to have an easy life when you don’t even get to save a hundred bucks every month.

Many families wrestle with this, especially when emergency needs, school costs, and future plans all pull from the same savings account. Every withdrawal felt like a setback, even when the money was used responsibly. Once those savings were split by purpose, something shifted. Each goal became easier to track, and progress stopped feeling so scattered.

That clarity changes how saving feels day to day. Instead of guarding a single balance, families start to see multiple paths forward. Giving money a clear role often turns saving from a source of hesitation into something that feels steady and intentional.

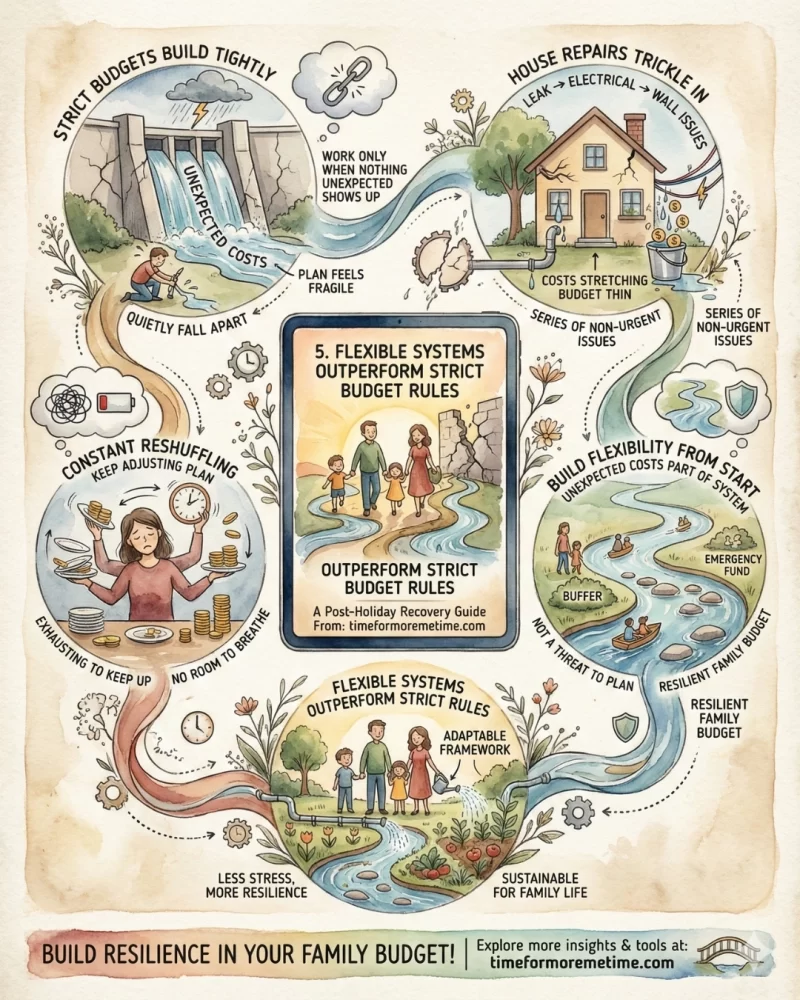

5. Flexible Systems Outperform Strict Budget Rules

Some budgets fall apart quietly, not because of overspending, but because they were built too tightly. Everything works as long as nothing unexpected shows up. The moment it does, the whole plan starts feeling fragile.

This happened to my family personally when my parents ran into a series of house repairs that weren’t urgent enough to plan for but couldn’t be ignored either. A leak led to electrical work, which uncovered another issue behind the walls. The costs didn’t arrive all at once. They trickled in, stretching the budget thin and forcing constant reshuffling just to keep things moving.

What stood out wasn’t the expense itself, but how exhausting it felt to keep adjusting a plan that had no room to breathe. Family budgets tend to work better when you build flexibility from the start, so unexpected costs feel like part of the system instead of a threat to it.

Conclusion

Family budgets often feel harder because small, everyday realities carry more weight when money is shared. Timing, recurring costs, and flexibility all shape how manageable a budget feels from month to month.

If you want to build clearer budgeting habits and understand how to manage family finances with more confidence, read our latest posts, follow us on social media, and visit our YouTube channel for practical guidance you can apply right away.