Budgeting becomes stressful when your money does not grow fast enough for your needs. Many people face this pressure because reports show that many households struggle to save even a small amount each month. This can leave you unsure about your next step when you want more control over your future.

I dealt with the same stress during my early years in San Francisco when prices kept rising and my savings stayed the same. I remember checking my balance at a bank and worrying that I was not doing enough. That moment pushed me to search for better tools that could help my money grow. And that’s through a high-yield savings account.

Since I went through this myself, I will explain how a high-yield savings account (HYSA) works and how it can support your financial goals. Let’s get started!

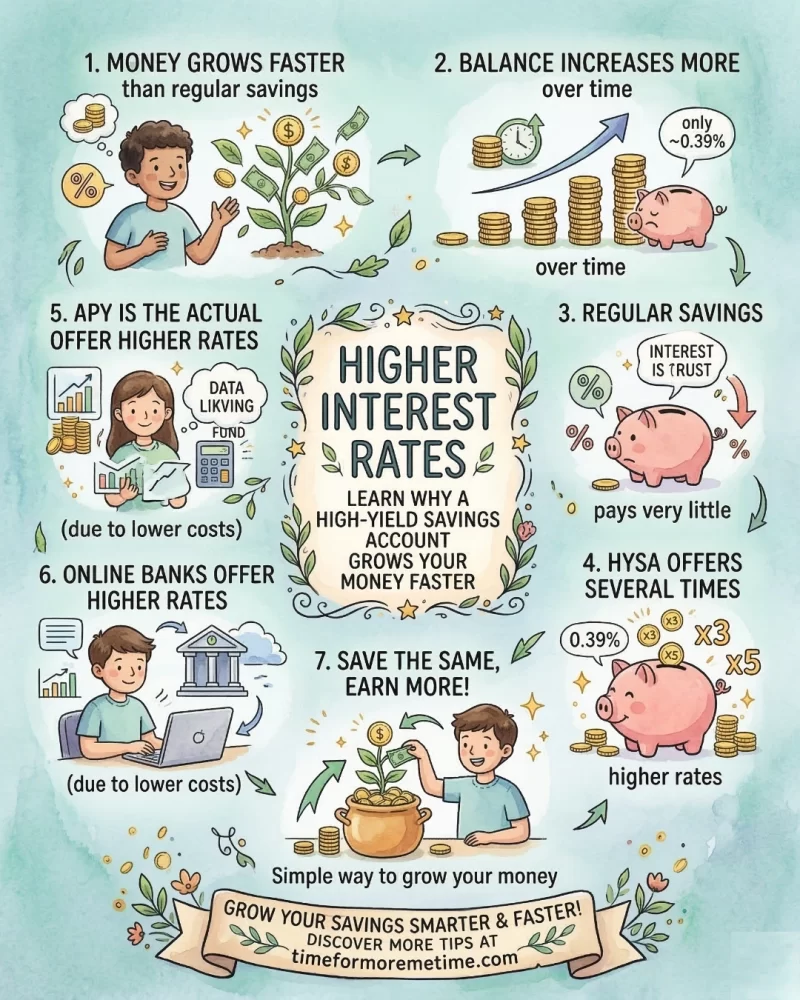

Higher Interest Rates

A high-yield savings account has higher interest rates, which helps your money grow faster than a regular savings account. With one, your balance increases more over time. For example, the national average interest rate for regular savings accounts is only about 0.39% APY (Annual Percentage Yield), while many high‑yield savings accounts offer several times that rate.

I know I said it multiple times, but APY is the actual rate of return you earn on an investment.

Anyway, you can try to get one from an online bank since they can offer higher rates because they do not carry the same costs as traditional banks. This means you can earn more even if you save the same amount each month. It is a simple way to grow your money without extra steps.

Easy Access To Your Money (Liquidity)

HYSA allows you to withdraw money immediately when you need it. You can move funds to your checking account with a few taps, which makes handling surprises easier. I used this when a sudden repair came up in my apartment, and the money was ready right away.

Many banks say most transfers finish within one business day, so you do not have to wait long to use your money. Life can change quickly, and it is important to have savings that are safe but still easy to reach. Quick access makes saving less stressful and gives more control over your money.

In my case, this is also helpful for blog monetization because having fast access to my funds means you can reinvest earnings or cover business expenses, primarily paying my team, without delays.

This is one reason a high-yield savings account works well. It gives speed, security, and flexibility, which helps you manage your finances more confidently.

FDIC Insurance

A high-yield savings account protects your money if the bank ever “loses” it (for example, due to robbery or natural disaster). This is because FDIC insurance covers deposits up to the insured limit, keeping your funds safe even if the bank encounters problems. I trusted this protection when I first opened an online account, which allowed me to focus on growing my savings without worry.

I remember my friend, whom I helped with his business, loving FDIC insurance. Having this security helps him manage his earnings from digital products on Etsy, as he knows his funds are protected while he reinvests in his business.

FDIC insurance acts like a shield around your money. It gives strong protection and helps you take the next steps with confidence. Knowing your savings are safe makes it easier to plan for the future.

No Monthly Fees

An HYSA often has no monthly fees, which lets you keep more of your money. This makes saving easier because you do not lose money to charges that add up over time.

Many banks show that fee-free accounts help customers save more each year because nothing is taken out for maintenance. Not having fees makes a big difference because every dollar you keep adds to your progress. It also removes the worry of surprise charges. Clear and simple rules help you stay consistent with your savings. This is especially useful for applying efficiency tips for freelancers, since keeping costs low lets you focus more on growing your income and business.

Online Management

A high-yield savings account is easy to manage online, which keeps your money organized. You can check your balance, transfer funds, and track your progress anytime. I used this feature during busy workdays at the hospital in San Francisco when I only had a few minutes. It made saving simple even on hectic days.

Many surveys show that about 53% of the world’s population, or over 4.2 billion people, use online banking because it saves time, gives quick account updates, and feels convenient, reliable, and secure. Simple access helps people save more regularly and stay aware of their money. Online tools give control and clarity, which makes it easier to reach your financial goals.

Financial Flexibility

A high-yield savings account gives you more flexibility because it can support several goals at once. You can use it for emergencies, short-term plans, or future projects without opening new accounts. I relied on this when I saved for travel while keeping my emergency fund in the same place. It helped me stay organized and ready for anything.

Having flexibility makes it easier to manage your money because you do not have to move funds between multiple accounts. This keeps your savings simple and gives more control over how you use it. One account can handle multiple goals, which makes planning less complicated.

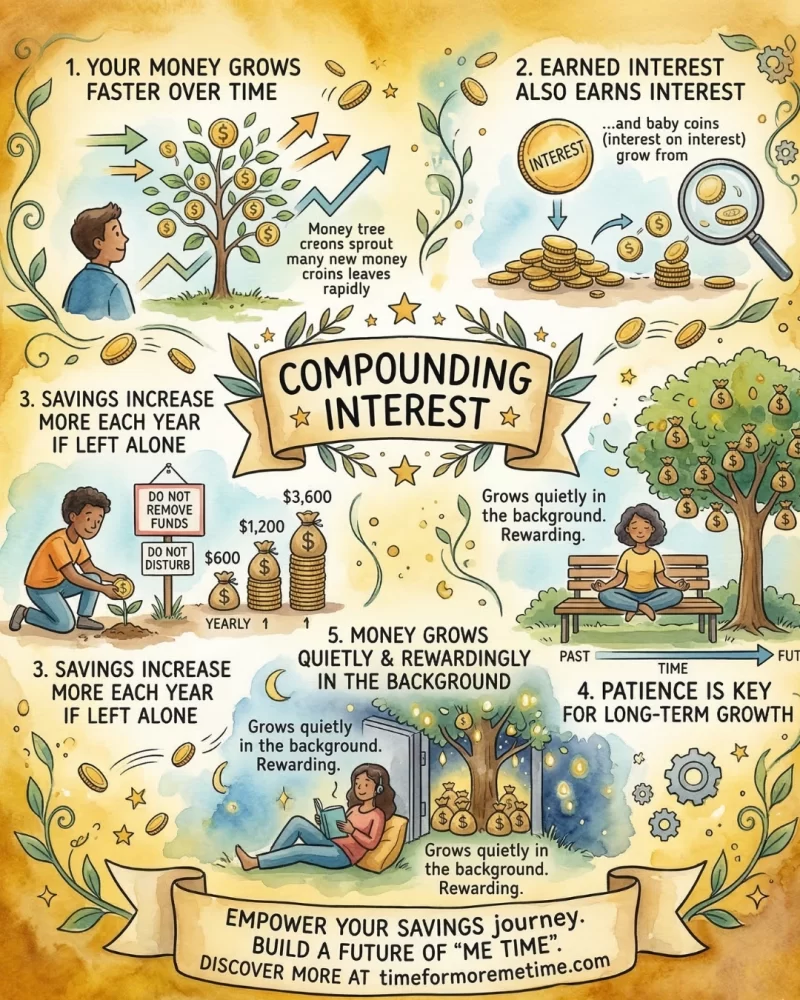

Compounding Interest

A high-yield savings account uses compounding interest—on top of high interest rates—which helps your money grow faster over time. The interest you earn also earns interest. I noticed this clearly during my first full year with an online savings account. My balance grew more than I expected because the interest kept adding up on itself.

Many guides explain that compounding helps your savings increase more each year if you leave the money in the account. Patience matters for long-term growth. Compounding also makes saving more rewarding because your money grows quietly in the background.

Is A High-Yield Savings Account Worth It?

A high-yield savings account offers benefits that help your money grow and stay protected. The features it has make you better prepared for both expected and unexpected expenses, helping you plan for a secure financial future.

If you like this content, share it around. Subscribe to my blog and my socials. Also, check out my YouTube channel. See you there!

Sources:

- NerdWallet. (2026). Average Bank Interest Rates for Savings Accounts, CDs and More. nerdwallet.com/banking/learn/average-rates-for-deposit-accounts

- FDIC. (2024). Understanding Deposit Insurance. fdic.gov/resources/deposit-insurance/understanding-deposit-insurance

- FindBanks. (2026). Best High-Yield Savings Accounts 2026. findbanks.com/high-yield-savings

- CoinLaw. (2026). Online Banking Usage Statistics 2026: Shocking Growth. coinlaw.io/online-banking-usage-statistics/

- ResearchGate. (2021). Customers’ Opinions on Reasons for Using Online Banking: Experience of Customers in Tanzania. researchgate.net/publication/353035559_Customers’_Opinions_on_Reasons_for_Using_Online_Banking_Experience_of_Customers_in_Tanzania

- Investopedia. (2025). The Power of Compound Interest: Calculations and Examples. investopedia.com/terms/c/compoundinterest.asp