Budgeting can get really frustrating if your income and expenses change a lot. Many families find that their money can go up and down from month to month, which makes sticking to a fixed budget hard. If your budget keeps falling apart even when you try hard, the issue might not be your effort but the budget itself.

I faced this problem a few years ago when my HVAC system was acting up, leading to high and unpredictable utility bills. On top of that, our grocery costs were all over the place. My fixed budget just didn’t work. This experience pushed me to look for more flexible budgeting methods, which I now use and teach.

In this post, I’ll introduce you to dynamic budgeting. You’ll learn how to start by focusing on things that change, set flexible limits, and make changes without having to start your budget from scratch. Let’s get started!

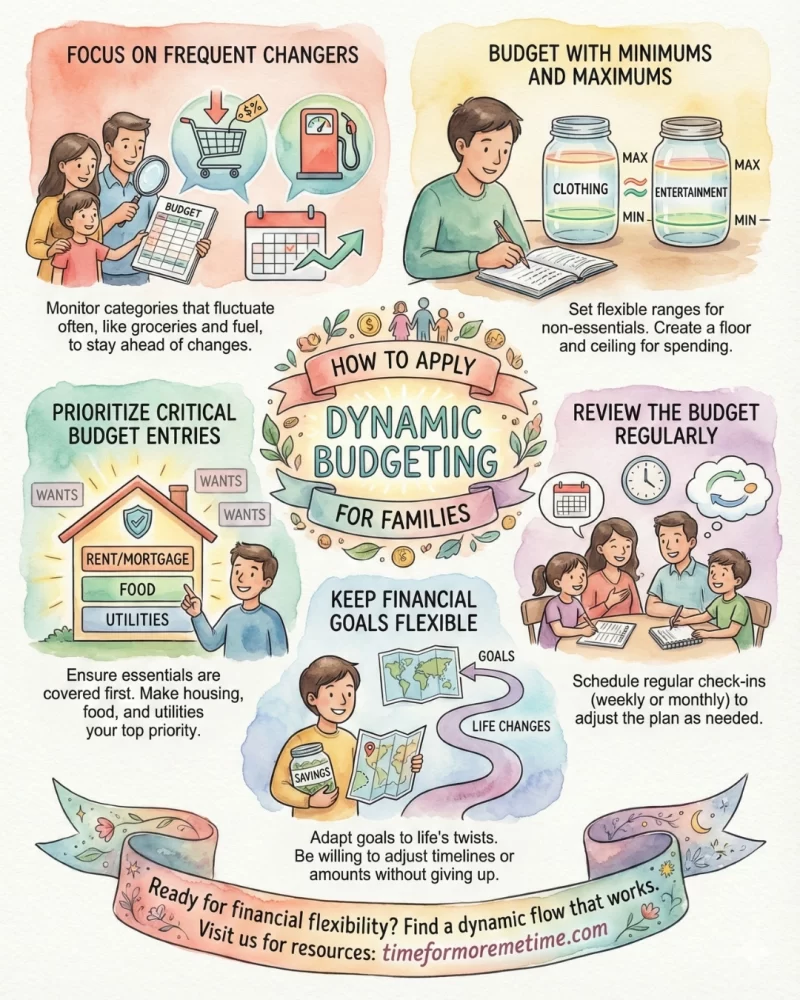

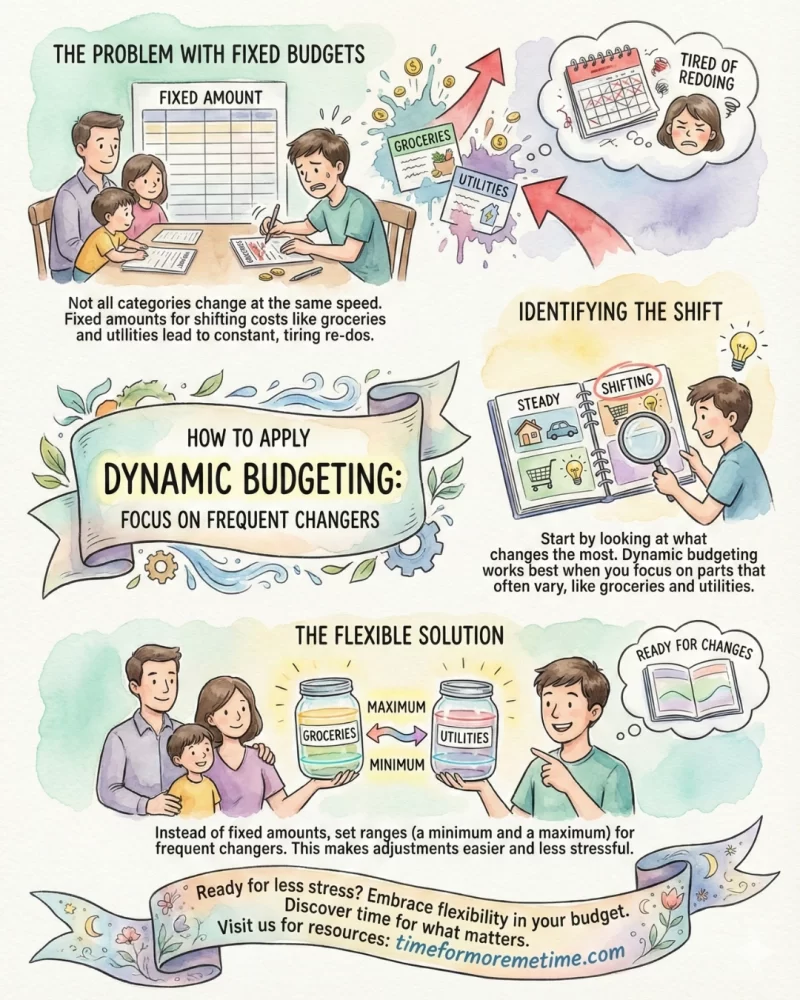

1. Focus On Frequent Changers

Start your budget by looking at what changes the most. Dynamic budgeting works best when you pay attention to the parts that often shift. Not all categories change at the same speed. Some stay steady, while others can vary each week. By focusing on these changing parts, making adjustments becomes easier.

In my old budget, groceries and utility costs were the first to change frequently. Often, the increases were small, but sometimes I will be hit with a sudden spike. I wasn’t ready for it and often ended up redoing my budget over and over.

It got tiring, so I stopped making last-minute fixes. Now, I set ranges for my budget instead of fixed amounts on my utilities and groceries. I decide on a minimum amount and a maximum amount for each of them. I’ll explain how this works in the next section.

2. Budget With Minimums and Maximums

Set clear minimum and maximum spending limits for each category. Budgets are harder to follow when you rely on one exact dollar amount. Some costs, like rent, are fixed. Others change based on prices, seasons, or how your household runs that month. Treating all costs as fixed can create unnecessary pressure.

I’ve seen people struggle with this, especially when budgeting for groceries and utilities. For example, my brother set his grocery budget at $600 for the month. When his spending jumped to $650 because of higher prices due to the recently imposed tariffs and hosting dinners for the family and relatives occasionally, he felt off track, even though nothing unusual happened.

Instead of aiming for a single number, set a minimum and a maximum amount. For groceries, a range of $550 to $700 makes more sense. For utilities, you might budget between $180 and $260, depending on the season. As long as spending stays within these limits, your budget remains solid. This makes dynamic budgeting easier because adjustments are clear and not just guesswork.

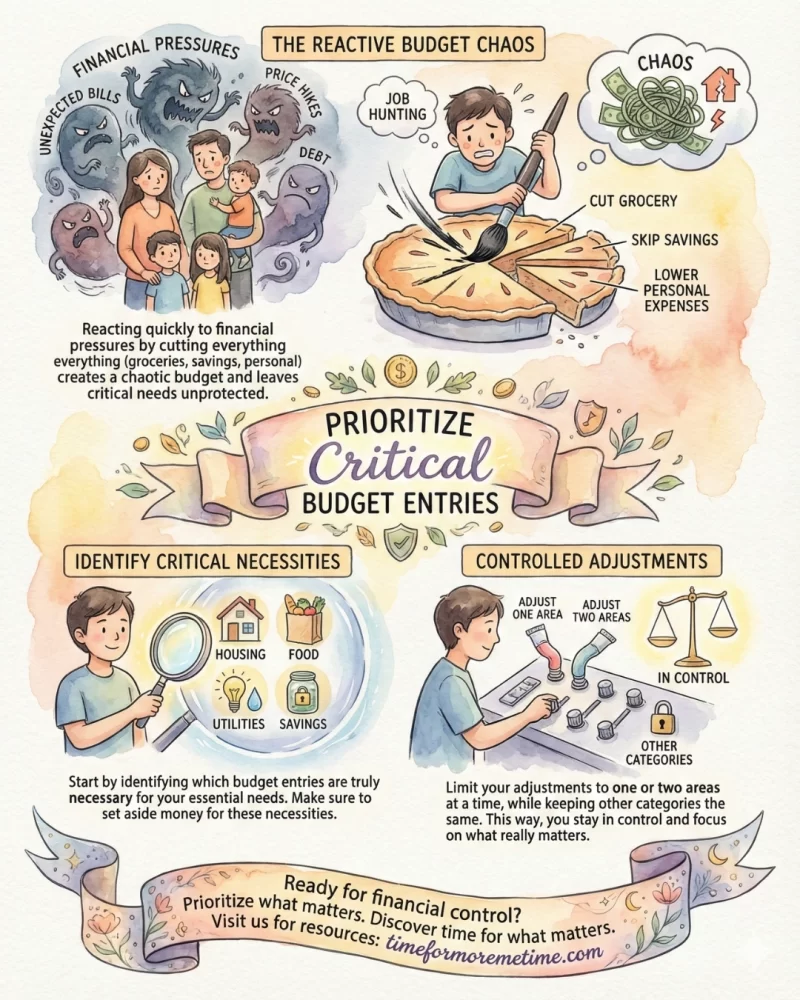

3. Prioritize Critical Budget Entries

It’s important to prioritize budget categories for your essential needs. While dynamic budgeting highlights the areas that change often, you must also make sure you set aside money for necessities.

Many head of families in Reddit struggle when they react quickly to various financial pressures, which often lead them to do job hunting for additional income. For example, they might cut grocery spending, skip savings, and lower personal expenses all in one month if utility bills go up. This can create a chaotic budget because they don’t protect their critical needs.

To avoid this chaos, start by identifying which budget entries are truly necessary. Limit your adjustments to one or two areas at a time, while keeping other categories the same. This way, you can stay in control of your budget and focus on what really matters.

4. Review The Budget Regularly

Review your budget and do finance monitoring whenever your financial situation changes. A budget works best when you respond quickly to real changes, so don’t wait until the end of the month to check it. If you notice any small shifts, take the time to review your budget right away. You don’t always have to make changes immediately; just stay informed. Regular check-ins can help you adjust when necessary.

Many people face bigger problems when they delay their reviews. For example, an unexpected bill might show up, or income could arrive later than planned. If the budget isn’t checked for weeks, multiple categories can feel off at once, making it hard to fix everything.

Instead of sticking to a monthly schedule, connect your reviews to specific events. When you get a higher bill, experience a change in income, or have an unexpected expense, check your budget within the same week. This proactive approach keeps your budget aligned with your actual financial situation.

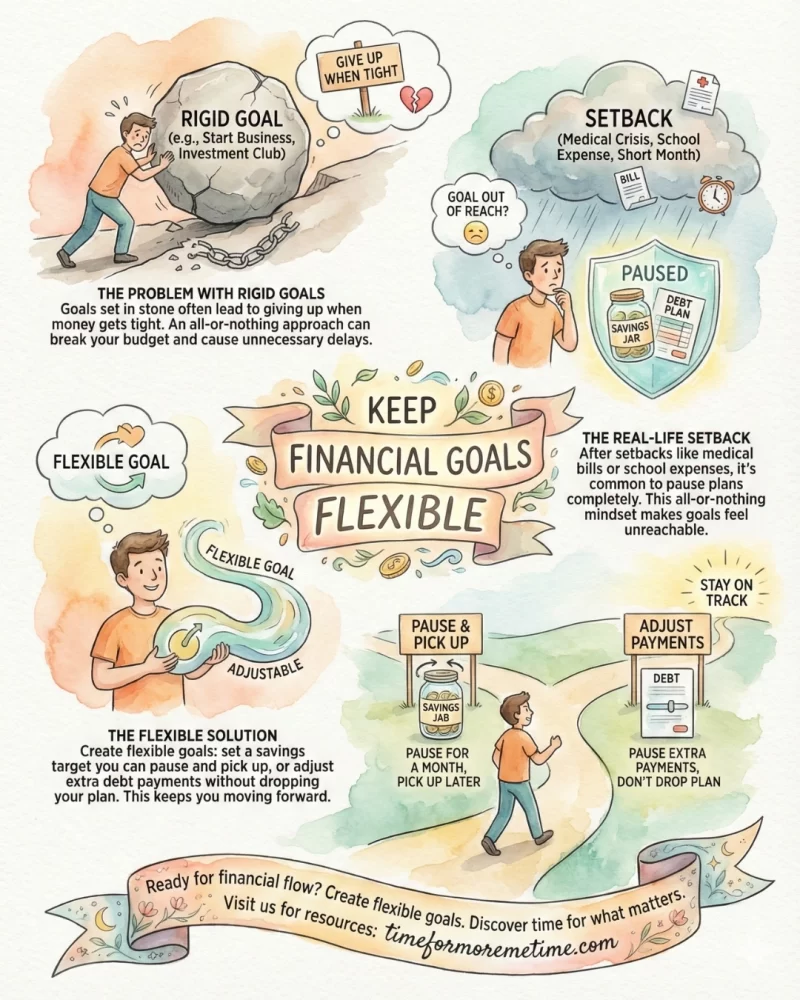

5. Keep Financial Goals Flexible

Make your long-term financial goals like starting a good business or getting into investment clubs flexible and adaptable. After all, you can stay on track when your goals can adjust without breaking your budget. I’ve experienced this myself. I often give up when my goals are set in stone and money gets tight. But now, I keep moving forward even during tough months by having flexible goals.

A lot patients I’ve met pause their savings or debt plans completely after dealing with a medical crisis. But whether it’s a medical bill, a school expense, or a short month, they often feel their goals are out of reach. These setbacks usually aren’t permanent, but an all-or-nothing approach can cause unnecessary delays.

To avoid this, create goals that allow for some flexibility. For example, set a savings target that you can pause for a month and pick up again later when things improve. You can also pause extra debt payments without completely dropping your plan.

Conclusion

Dynamic budgeting works when your plan adapts to real life rather than fighting it. With the right steps, you can turn budgeting into a system that responds rather than reacts.

If this post helped clarify how to apply dynamic budgeting in your household, read our other blogs, follow our socials, and join us for more practical posts like this and watch our YouTube videos.

Source

- Photo: Pexels: Yan Krukau