If you’re raising a big family, money can disappear fast. Groceries, school supplies, bills—everything adds up. It might feel like you’re always spending and never catching up. Already tracking your expenses? This guide takes it a step further—showing you how to turn that information into a simple budget that works for big households. Let’s get started!

1. Start With Your Lowest Consistent Income

If your income changes month to month, always budget based on your lowest reliable average, not your best month. For large families, planning with a safety buffer is essential. A sudden drop in income can affect not just one person, but everyone in the household.

Look at the last three to six months and identify the month with the lowest income. Use that number as your planning base. Anything you earn above that can later be allocated toward savings, debt payments, or a family treat.

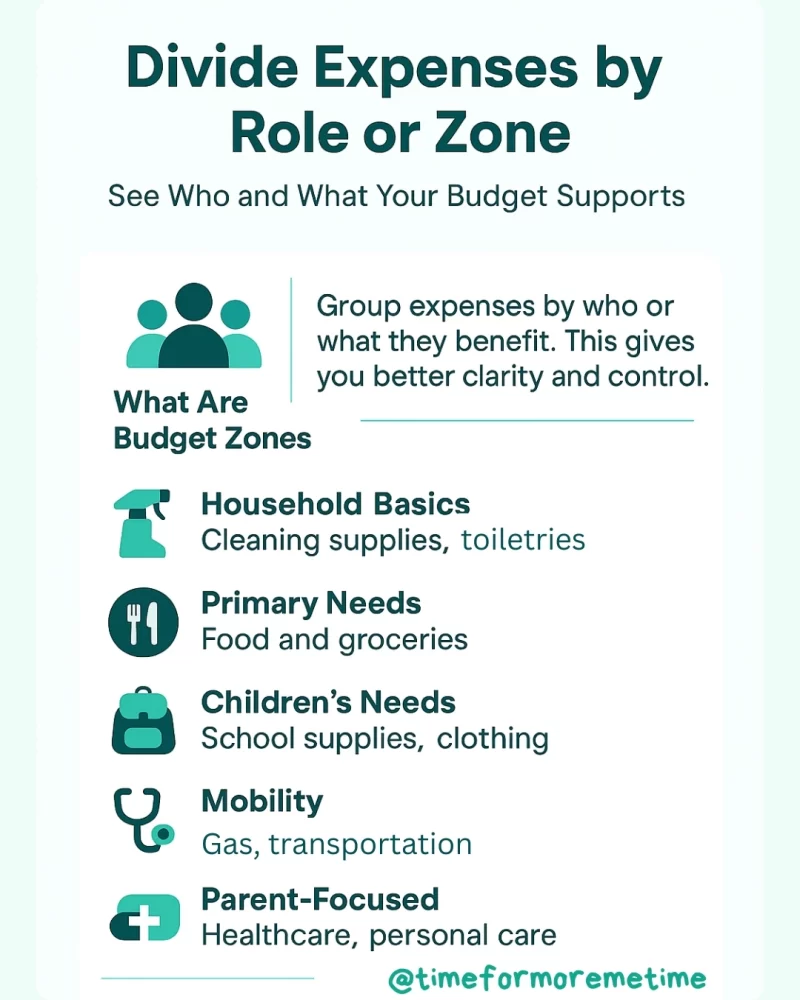

2. Divide Expenses By Household Role Or Zone

When managing for multiple people, it helps to categorize expenses by the individuals or entities they support. Try splitting your budget into “zones” like:

- Household basics like cleaning supplies

- Primary needs like food

- Children’s needs like school supplies

- Mobility like gas

- Parent-focused expenses like healthcare

This way, you don’t just see line items—you understand where the money is going and who it’s supporting. It also makes it easier to spot which areas are growing and need attention.

3. Use A Weekly Budgeting Rhythm

Big families move fast. School projects, birthdays, broken appliances—they can all pop up without notice. A monthly budget can feel too rigid for this kind of pace. So, instead, adopt a weekly rhythm.

Break your budget into four parts and check in every week. Review what’s been spent, what’s coming up, and what needs to shift. Even 15 minutes each Sunday can make a big difference in preventing overspending.

4. Rotate Monthly Focus Areas

Not every category needs to be the priority every month. One way to ease financial pressure is to rotate your focus areas:

- In the first month, focus on stocking up household supplies

- The next, save for an upcoming school event or uniform replacement

- Afterwards, prioritize healthcare or birthday gifts

This rotation system spreads out costs so they don’t hit you all at once. It also gives you a clear direction each month without overwhelming your budget.

5. Bundle Purchases For Efficiency

With large families, making multiple trips for individual items can be time-consuming and costly. Instead, bundle your purchases and errands to reduce costs:

- Plan one big grocery haul every two weeks instead of small daily visits

- Group birthday gifts or seasonal needs into one shopping round

- Coordinate school supply restocking with other home needs

Bundling avoids impulse spending and saves on transportation, especially if you live far from major stores or rely on fuel.

6. Set A Flex Fund

This is different from an emergency fund. A family flex fund is a small amount of cash set aside each month for unexpected but non-emergency situations—like a class party, friend’s birthday gift, or a last-minute outing. Even $300 to $500 can prevent last-minute stress and stop you from dipping into your rent or food categories.

A flex fund gives your budget breathing room without hurting your essentials.

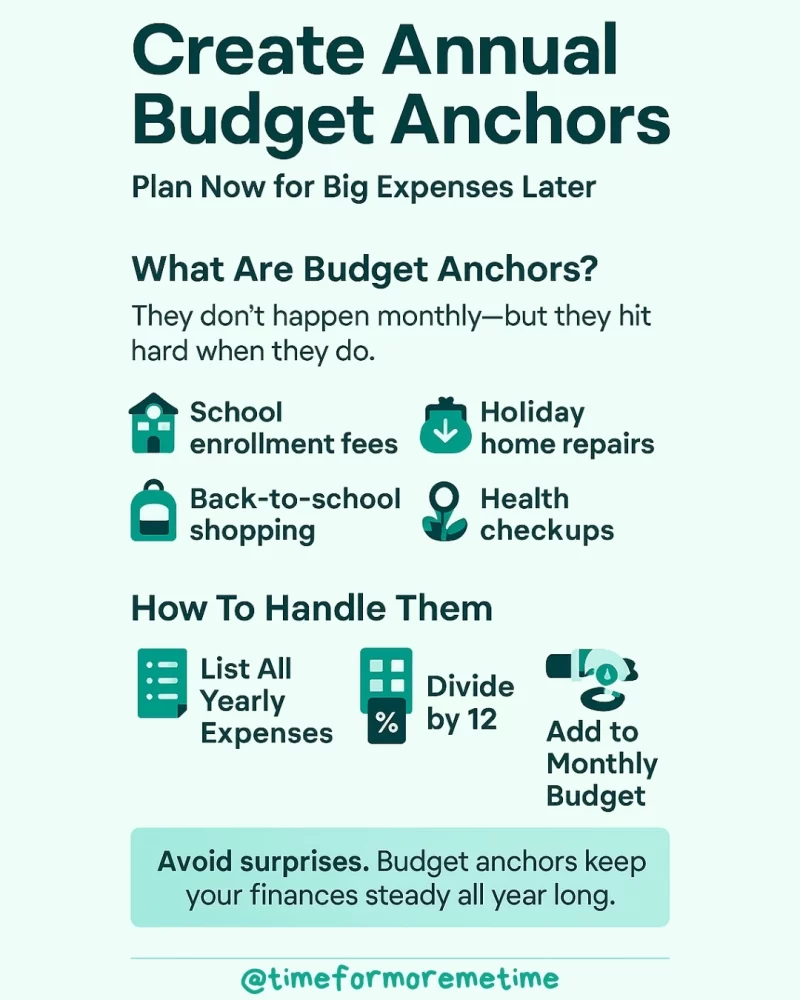

7. Create Annual Budget Anchors

Some expenses don’t happen every month, but when they do, they’re big—and heavy like an anchor. These include:

- School enrollment fees

- Holiday expenses

- Major household repairs

- Back-to-school shopping

- Health checkups

Make a list of all yearly anchor expenses and estimate their cost. Divide each one by 12 and add that amount to your monthly budget. That way, when those months arrive, you’re not caught off guard.

8. Build Household Habits That Support Your Budget

Budgeting doesn’t only happen on paper—it happens through daily choices. Set household routines that make your budget easier to follow:

- Designate one or two “no-spend” days a week

- Limit meals out to once a week or less

- Pack lunches and snacks in advance to avoid daily spending

These habits alleviate pressure on your budget categories and reduce unnecessary expenses without requiring constant monitoring.

9. Use Your Calendar As A Budget Tool

Your family calendar is one of your best budgeting tools. Map out the month and include:

- School activities

- Birthdays

- Church or community events

- Out-of-town trips

- Bills with fixed dates

Seeing events ahead of time helps you anticipate spending before it happens. You can shift money between weeks or plan for extra costs early, before they cause budget stress.

10. Celebrate Budget Wins Together

Sticking to a family budget takes teamwork. When you achieve a goal—such as staying under your grocery budget or saving for a school event—celebrate it. It doesn’t have to cost money. Try:

- A family game night

- A home-cooked favorite meal

- A group shout-out during your budget check-in

Celebrating wins builds positive habits and keeps the whole family engaged in the process.

Conclusion

Budgeting for a large family takes more than a spreadsheet—it takes rhythm, teamwork, and flexibility. With strategies tailored to your household’s pace and needs, you can avoid daily money stress and start building a system that works month after month.

To get more helpful money tips, subscribe to our blog, follow us on social media, and check out our YouTube channel for smart and practical videos.

Sources

- Photos: Unsplash: Sincerely Media