Budgeting on a low income can feel frustrating, but you’re not alone. The good news is, there are simple ways to take control of your money without needing a big paycheck. In this post, you’ll find practical and easy-to-follow tips designed to help budget for low-income families to cover the basics and even start saving. Let’s get started!

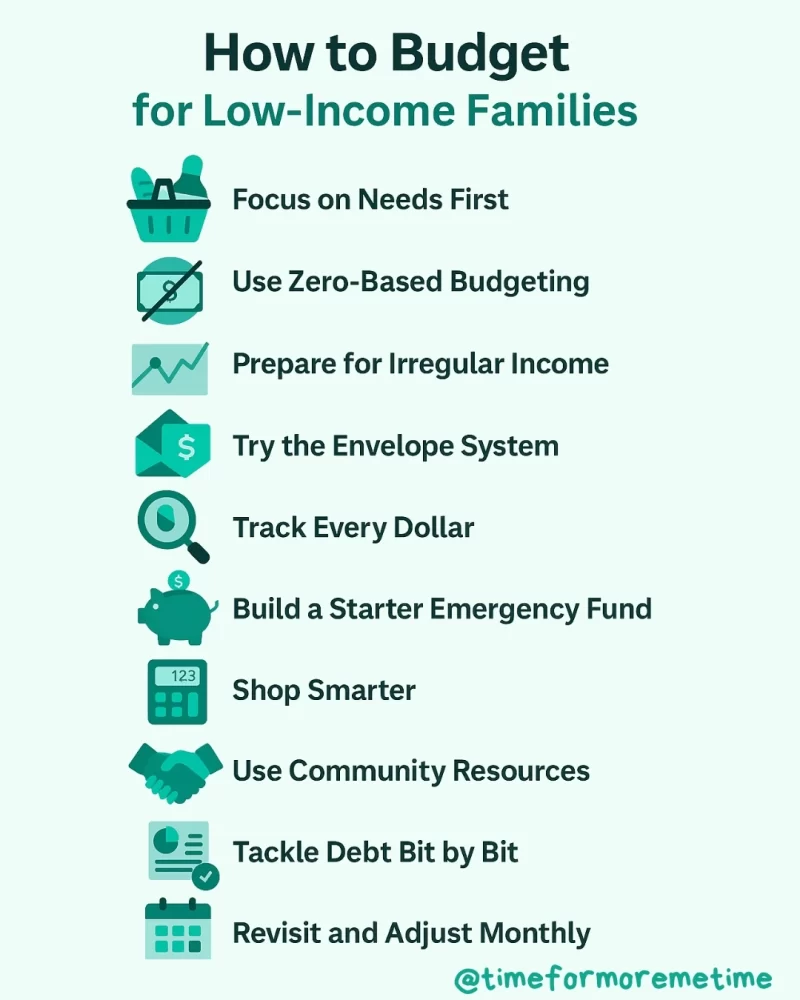

1. Focus On Needs First

The first rule of budgeting on a tight income is to secure your essentials. That means putting your money toward the basics: rent, groceries, utilities, transportation, and necessary healthcare. Once you’ve covered these, evaluate where to reduce or reallocate.

Make a list of must-haves. Use a notebook or app to track the cost of each expense. This helps avoid overspending on non-essentials when funds are limited.

2. Use Zero-Based Budgeting

Zero-based budgeting forces you to assign every dollar to a specific task—bills, savings, or debt—until nothing is left unaccounted for. To get started, compute your total income and subtract each expense until your balance is zero. Adjust your categories monthly based on what works and what doesn’t.

3. Prepare For Irregular Income

Many low-income families rely on freelance, seasonal, or hourly work. If your income varies, it’s crucial to base your budget on your lowest-earning month to avoid shortfalls. Create a bare-bones budget that covers only the essentials. Any extra income can then be saved, used to pay off debt, or used to stock up on necessities.

4. Try The Envelope System

The envelope system is a hands-on way to stay in control. You assign cash to categories like food or transportation and only spend what’s in the envelope. Once it’s gone, you stop spending. This makes budgeting feel more real. It’s beneficial if you tend to overspend with cards or online shopping.

5. Track Every Dollar

When your family is truly struggling, every cent matters. Tracking your spending helps you identify where your money goes and what can be reduced or cut out. Use a budgeting app or a simple notebook to write down every transaction. Reviewing your spending on a weekly basis keeps you aware and accountable.

6. Build A Starter Emergency Fund

Unexpected expenses can derail even the best budget. That’s why it’s important to build a small emergency fund—even if you’re only saving $5 or $10 at a time. Aim for an initial goal of $250 to $500. Keep the fund in a separate account that’s not easy to access. The goal is to create a financial buffer that reduces stress and prevents you from turning to credit.

7. Shop Smarter

A practical way to stretch your budget is to shop with a strategy. Start by planning your grocery list around weekly sales and discount flyers—this helps you prioritize essentials without overspending. When possible, buy in bulk for items you use often, and be sure to stick to your list to avoid impulse purchases.

To save even more, use cashback apps, digital coupons, and store loyalty programs. Choosing generic or store brands can also make a big difference—many offer the same quality as name brands at a fraction of the price.

8. Use Community Resources

You don’t have to figure everything out on your own—there’s help available if you know where to look. Many communities offer programs and services that can ease financial pressure for low-income families.

From local food pantries and housing assistance to free school supplies and healthcare clinics, these resources are available to support families as they work toward stability. Taking advantage of them isn’t a handout—it’s a smart step toward saving money and protecting your well-being.

9. Tackle Debt Bit By Bit

Debt can quietly eat up your budget if left unchecked. While paying it off all at once may not be realistic, small and consistent payments can still make a big difference over time.

Try the snowball method—paying off the smallest balance first—for quick wins and motivation. Alternatively, use the avalanche method to pay off the most expensive debt first and save more on interest. Most importantly, avoid taking on new debt unless absolutely necessary.

10. Revisit And Adjust Monthly

No budget is ever set in stone. As your circumstances change, your spending plan should too. That’s why reviewing your budget at the end of each month is so important.

Take 30 minutes to check in. Are your numbers still realistic? Did anything unexpected throw your plan off track? Use this time to make adjustments, celebrate small wins, and set the tone for the month ahead.

Conclusion

Finding the best way to budget for low-income families doesn’t have to feel overwhelming. With the right tools, small steps, and steady effort, progress is possible—even on a tight income. Start where you are, adjust as needed, and trust that every positive habit makes a difference.

To get more helpful money tips, subscribe to our blog, follow us on social media, and check out our YouTube channel for smart and practical videos.

Sources

- Photos: Unsplash: Yousef Samuil