Preparing for retirement can feel overwhelming, especially with rising prices and no clear roadmap. Many people aren’t sure where to begin or how much they’ll need. In this post, I’ll walk you through the most practical steps to help you prepare, even if you’re starting late or on a tight budget. Let’s get started!

1. Start With A Clear Retirement Goal

Before you think about saving or investing, take time to define what retirement looks like for you. Setting a clear goal gives your plan direction and helps you make smart decisions. Start with simple questions:

- When do you want to retire?

- What does your daily life look like?

- How much will you need each month to support that lifestyle?

Without a clear target, it’s easy to save blindly and fall short later. Most people should aim to save 10 to 12 times their annual income by age 67. But your number might be different depending on your goals, health, and family situation.

Use free tools to calculate how much you’ll need. When your goals are specific, your plan becomes easier to follow—and that makes it more likely you’ll stay on track.

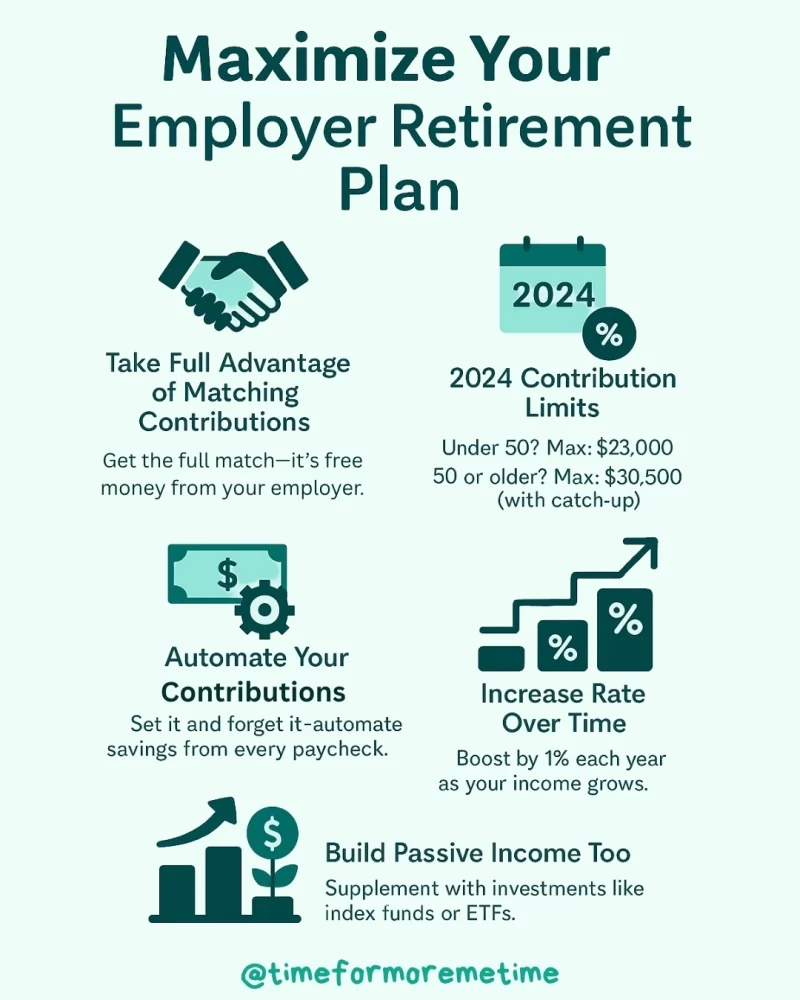

2. Maximize Employer Retirement Plans

If your employer offers a 401(k) or similar plan, take advantage of it, especially for matching contributions. In 2024, the individual contribution limit is $23,000, with an additional $7,500 catch-up contribution for those aged 50 and older, totaling $30,500. Automate your contributions and aim to increase your rate by 1% annually as your income grows.

Start by contributing enough to receive the full match. While these plans are essential, consider supplementing your savings with passive income from having regular investments to enhance your retirement savings.

3. Diversify With IRAs And Roth IRAs

Consider opening an IRA or Roth IRA alongside your workplace plan. In 2024, the combined contribution limit is $7,000, with an additional $1,000 catch-up for those aged 50 and older, totaling $8,000. You can split contributions between both types, but the total must not exceed these limits.

Consistent contributions, even in small amounts, can significantly impact your savings. If you want to fund your IRA without using your main income, consider side hustles like freelance writing or selling digital products to generate extra cash and boost your retirement savings.

4. Avoid Common Planning Mistakes

Many people make avoidable retirement planning errors, such as delaying savings, withdrawing Social Security too early, or neglecting taxes on retirement income. A significant oversight is underestimating healthcare costs, which can exceed $165,000 for retirees and quickly erode savings.

To avoid these pitfalls, plan for medical expenses, premiums, and long-term care needs from the start. Use budgeting apps to project costs and explore tax-efficient withdrawal strategies.

Additionally, be cautious about claiming Social Security benefits before full retirement age, as this can lead to permanently reduced payments. Note that this is separate from Medicare, which typically begins around age 65.

5. Diversify Savings And Assets

Relying on a single income source or investment type can put your retirement at risk—especially during economic downturns. A well-diversified plan gives you more stability and flexibility over time.

Experts recommend keeping one to three years’ worth of living expenses in liquid assets. Consider a high-yield savings account to cover emergencies or market dips without selling investments at a loss.

Beyond that, diversify your portfolio across stocks, bonds, annuities, and even alternative options like real estate investment. Each asset class performs differently depending on the market, helping you spread risk while increasing potential returns.

To keep your plan on track, review and rebalance your portfolio at least once a year. A financial advisor can help you make informed decisions based on your goals, risk tolerance, and market trends. This approach not only protects your nest egg but also supports long-term passive income, making your retirement more financially secure.

Conclusion

Planning for retirement doesn’t have to feel overwhelming. By setting clear goals, maximizing your savings options, avoiding common mistakes, and diversifying your income sources, you’re taking the right steps toward a more secure future. Consider applying these practical, flexible strategies, whether you’re starting early or catching up later in life.

Retirement is your opportunity to live on your own terms. Start small, stay consistent, and keep learning as you go. For more financial planning tips and retirement strategies, subscribe to our newsletter, follow us on social media, and check out our latest videos on YouTube.

Source

- Photo: Unsplash: Beth Macdonald