Saving for retirement sounds important, but it can also feel confusing or out of reach, especially when you’re still dealing with monthly bills. You’re not alone. This guide will walk you through simple, clear tips you can take to start saving now, even if you’re new to the idea. Let’s get started!

1. Start With A Realistic Budget

Before you can save, you need to know exactly where your money goes. A budget gives you control and a clear view of your financial habits.

Utilize budgeting tools like YNAB, Mint, or a simple spreadsheet to track your income and expenses. Break down your spending into three categories: essentials, non-essentials, and savings.

This allows you to identify what you can trim and how much you can start setting aside for retirement. Don’t aim for perfection—focus on being honest with the numbers.

2. Pay Off Debt Using A Focused Method

Once your budget is in place, take aim at your debt. The debt snowball method is a great place to begin.

List your debts from smallest to largest, pay off the smallest one first, and roll that payment into the next debt on your list. These quick wins build motivation and momentum. Each balance you eliminate frees up more money to direct toward your retirement savings—and that’s where real progress begins.

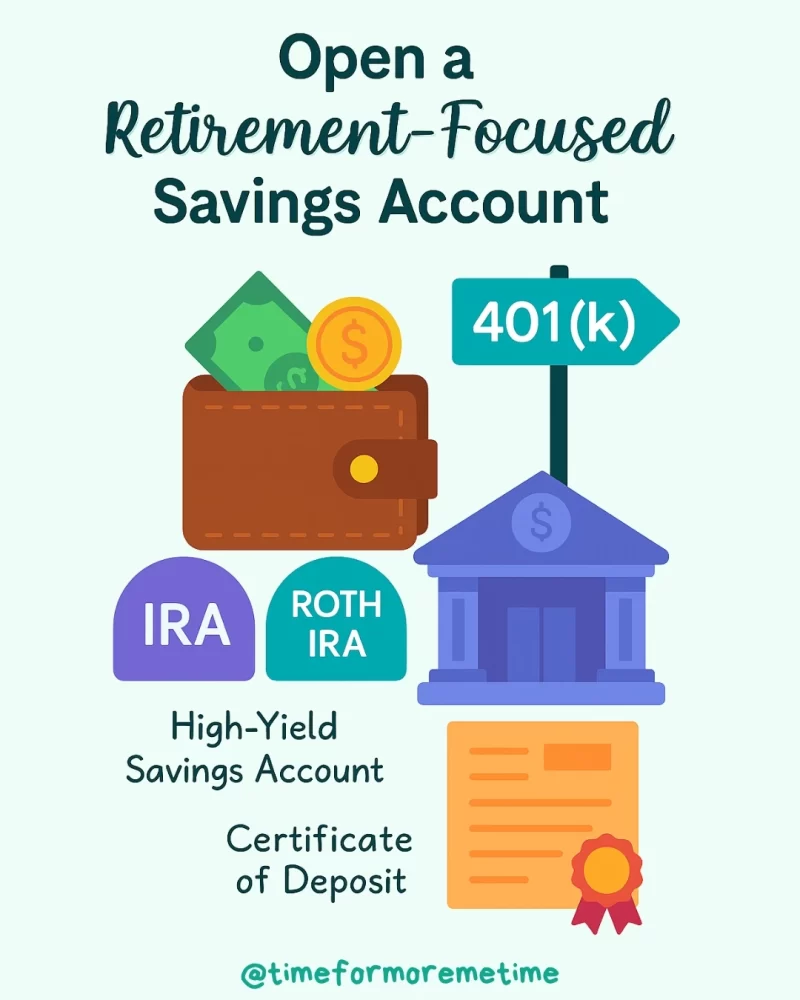

3. Open A Retirement-Focused Savings Account

With some breathing room in your budget, it’s time to choose the right place to grow your savings. If your job offers a 401(k) with matching contributions, take advantage of it—it’s essentially free money.

If not, consider an IRA or Roth IRA, which come with tax advantages that help your savings grow faster. For safer, short-term options, look into high-yield savings accounts or certificates of deposit (CDs). Each account has its purpose, so choose based on your goals and timeline.

4. Cut Expenses That Don’t Add Value

You don’t need to earn more to save more. Often, it’s about spending less on things that don’t matter.

Review your monthly bills and cancel any unused services, such as old subscriptions or automatic charges. Then look at daily habits: limit takeout, shop with a list, or try generic brands.

These small choices add up quickly. Even redirecting $25 or $50 a month into savings builds long-term impact.

5. Automate Your Savings To Build Momentum

Once you’ve identified how much you can save, automate it. Set up recurring transfers from your checking to your savings or retirement account each payday.

Automation removes the temptation to skip a month and helps you stay consistent. Most banks and budgeting apps allow you to adjust the amount anytime, so you can gradually increase your savings as your income grows.

6. Explore Brokerage Firms For Greater Growth

As your savings begin to grow, you may want to consider moving beyond standard savings accounts. Brokerage firms let you invest in index funds, mutual funds, or ETFs—options that typically outperform savings accounts over time. While they involve some risk, they also offer more potential for long-term gains.

New to investing? Begin with low-cost index funds and consider utilizing robo-advisors or platforms that offer built-in educational tools.

7. Build A Weekly System To Stay On Track

Even the best plan won’t work if you don’t follow through. That’s where simple time strategies come in. Set aside 20–30 minutes each week to review your budget, check your progress, and update your savings goals. Treat it like any other important appointment on your calendar.

To make it easier, try using productivity hacks like the Pomodoro method—25 minutes of focused work followed by a short break. You can also batch tasks together, such as paying bills and adjusting contributions, to avoid financial distractions throughout the week.

The goal isn’t to spend hours on your finances. It’s to build a consistent habit that keeps you moving forward without adding stress. A streamlined routine helps you stay focused, efficient, and in control of your retirement plan.

8. Set Specific, Measurable Goals

General goals like saving more aren’t enough. Set clear, time-based targets. For instance, aim to contribute $6,500 to an IRA this year or increase your monthly savings by $100.

Use your budgeting tools to track your progress. When goals are measurable and tied to a deadline, they become more motivating and easier to achieve.

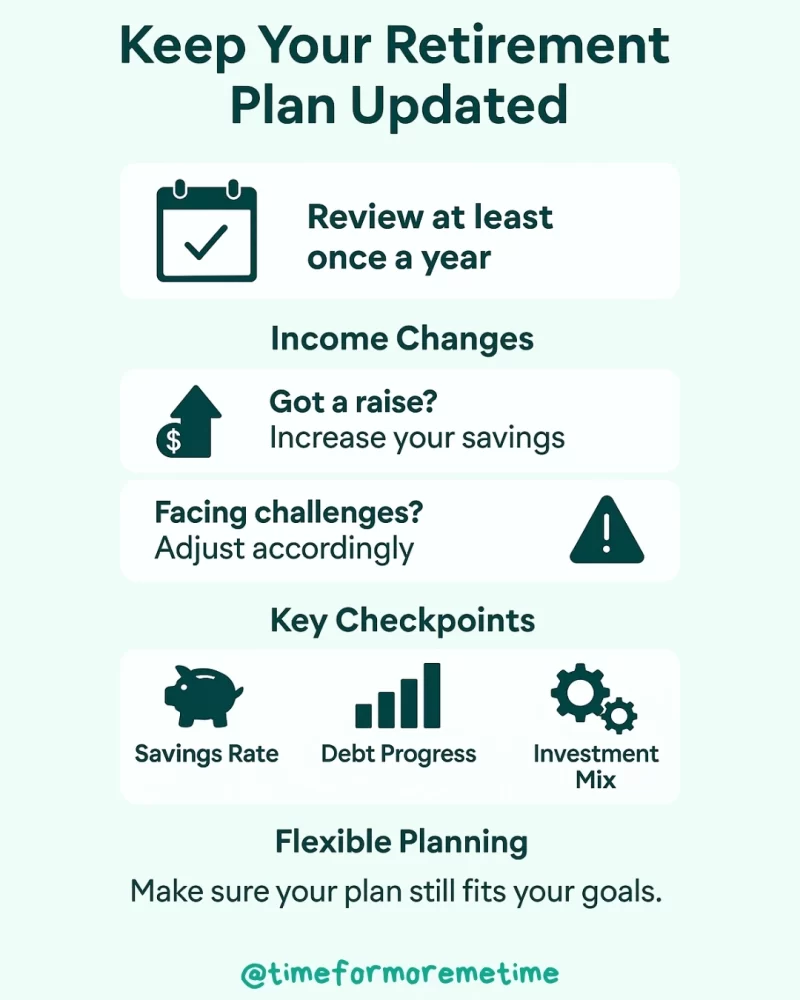

9. Review And Adjust Your Plan As Life Changes

Your financial situation won’t stay the same forever. That’s why it’s essential to review your retirement plan regularly—at least once a year. Revisit your savings rate, check on your debt progress, and see if your investments still align with your goals.

Got a raise? Boost your contributions. Faced with a setback? Reassess and adjust. Flexibility keeps your plan practical and relevant over time.

Conclusion

Saving for retirement is simply about making your money work for your future. Now that you know the basics, you’re better equipped to take that first step with confidence. Start small, stay consistent, and adjust as needed to accommodate life’s changes. You don’t need to have it all figured out—keep moving forward.

Want to learn more about managing your money? Check out our beginner-friendly guides, follow us on social media, and watch our videos on our YouTube channel.

Sources

- Photo: Unsplash: Julius Yls