If budgeting feels complicated or exhausting, the 50/30/20 rule offers a refreshingly simple solution. This method divides your income into three easy-to-follow categories, helping you cover essentials, enjoy life, and build savings without the stress of tracking every penny. In this post, I’ll introduce you to the 50/30/20 rule, so you can manage your money with clarity and balance. Let’s get started!

What Is The 50/30/20 Rule

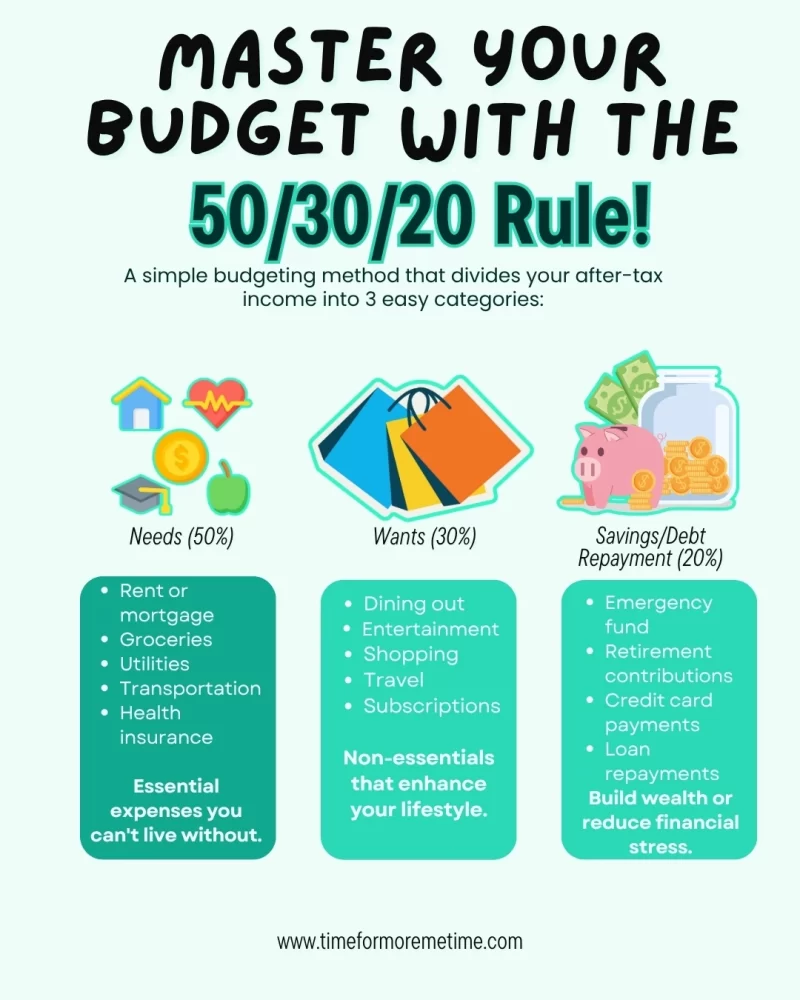

The 50/30/20 rule is a simple budgeting method that helps you divide your after-tax income into three key spending categories: needs, wants, and savings or debt repayment.

According to this rule, 50% of your income is allocated to essential expenses, such as rent, groceries, and utilities. The next 30% is allocated to discretionary spending—things you want but don’t necessarily need, like dining out or entertainment. The remaining 20% is directed toward savings or paying off debt.

This method establishes a clear framework for managing your finances and facilitates maintaining a balanced lifestyle. Instead of tracking every single purchase, you work with broader categories, which makes budgeting feel less like a chore.

How To Do The 50/30/20 Rule

Getting started with the 50/30/20 rule doesn’t require complicated spreadsheets or financial tools. It’s a straightforward approach you can apply with just a calculator and a few minutes of planning. Here’s how to break it down:

- Calculate After-Tax Income: Add up all your monthly income after taxes. This includes your take-home pay, side hustle income, and any consistent cash flow.

- Allocate 50% to Needs: Cover essentials like housing, utilities, transportation, insurance, and minimum debt payments. If these exceed 50%, you may need to adjust other categories.

- Use 30% for Wants: Budget for non-essentials such as dining out, subscriptions, hobbies, or travel. These are flexible expenses that make life enjoyable.

- Save or Pay Off Debt with 20%: Use this portion for emergency savings, retirement contributions, or accelerating debt repayment—Automate transfers where possible.

- Review and Adjust Monthly: Track your spending to see if your categories are balanced. Make small changes as your income or priorities shift.

The goal isn’t perfection—it’s awareness. Once you see how your money flows, it becomes easier to manage it with purpose.

How Can The 50/30/20 Rule Help You

The 50/30/20 rule helps eliminate the guesswork of budgeting by providing a clear structure. If traditional budgeting feels too detailed or time-consuming, this method streamlines the process and offers sufficient flexibility to accommodate most lifestyles.

This rule encourages balance by helping you spend and save with intention, reducing burnout while promoting long-term success. Saving becomes automatic thanks to the fixed 20% guideline, making it a monthly habit rather than an afterthought.

With defined limits on discretionary spending, you become more mindful of your purchases and avoid unnecessary splurges. The simplicity of tracking just three categories makes the system easy to follow and maintain. And because the percentages scale with your income, the 50/30/20 rule grows with you, whether you’re earning a little or a lot.

What Are The Drawbacks Of The 50/30/20 Rule

While the 50/30/20 rule is practical for many, it may not work for everyone. Depending on your income level, location, or financial goals, you may need to adjust it to suit your specific situation. Here’s what to keep in mind:

- Low-Income Limits: In high-cost areas, even covering basic needs might require more than 50% of your income, making the other categories unrealistic.

- Blurry Spending Categories: Not all spending falls neatly into the categories of needs, wants, or savings. Some items blur the lines and require personal judgment.

- No Debt Distinction: The rule doesn’t distinguish between good and bad debt. It may not help you tackle high-interest debt aggressively enough.

- Irregular Income Challenges: If your earnings fluctuate from month to month, adhering to fixed percentages can be challenging without frequent recalibration.

- Risk of Overspending: Allocating 30% to wants might feel like permission to splurge. Without mindfulness, this can derail savings.

The 50/30/20 rule should be viewed as a starting point. It’s flexible enough to adapt, but awareness and customization are key to making it truly effective.

Conclusion

The 50/30/20 rule delivers on its promise by providing a clear and realistic way to manage your finances. It encourages balance, simplifies decision-making, and keeps you focused on both your current needs and your future goals. It’s a solid foundation for anyone starting their budgeting journey and pairs well with other saving strategies for long-term financial health.

To get more helpful money tips, subscribe to our blog, follow us on social media, and check out our YouTube channel.

Sources

- Photos: Unsplash: Jakub Żerdzicki