Tackling debt can feel overwhelming—especially when you’re juggling multiple balances. But what if there was a way to turn small wins into big momentum? In this post, we’ll break down the debt snowball method—a strategy that helps you pay off debt step by step, while building confidence with every payoff. Let’s get started!

What Is The Debt Snowball Method

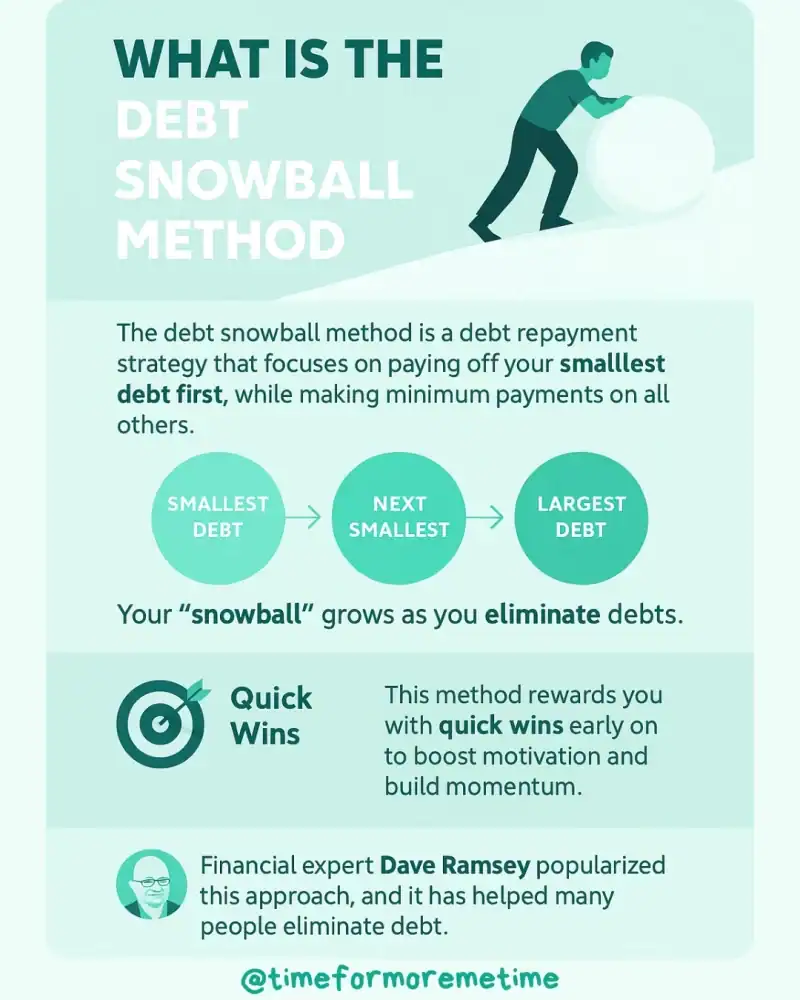

The debt snowball method is a debt repayment strategy that focuses on paying off your smallest debt first, while making minimum payments on all others. Once the smallest balance is gone, you roll that payment into the next smallest debt, and so on. As each debt disappears, your “snowball” grows—helping you tackle bigger balances with greater force.

This method is rooted in psychology, not just math. It gives you quick wins early in the process, which boosts motivation and builds momentum. Unlike approaches that focus on interest rates, the debt snowball prioritizes emotional payoff over financial optimization.

Financial expert Dave Ramsey popularized this approach, and it has helped many people stay consistent and feel encouraged as they eliminate debt. For anyone who needs a clear, step-by-step plan—and likes checking things off a list—it can be a game-changer.

It’s important to note that the debt snowball method may not lead to significant savings on interest payments. This method is primarily focused on helping you eliminate debt with less emotional and financial stress. If your goal is to be more efficient and save money in the long run, consider using the avalanche method instead.

How To Do The Debt Snowball Method

You don’t need any special tools to get started—just a list of your debts and a plan to follow through. The key is to stay focused on progress and trust the process. Here’s how to put the debt snowball method into action:

- List Your Debts by Balance Size: Write down all your debts—from smallest to largest—regardless of the interest rate. Set aside interest rates temporarily to focus on building momentum with small wins.

- Make Minimum Payments on All Debts: Keep up with your required minimums on every debt to avoid fees and protect your credit.

- Focus Extra Money on the Smallest Debt: Put any additional funds you can find toward your smallest balance. This could be money from cutting expenses, side hustles, or windfalls.

- Roll Payments Into the Next Debt: Once your smallest debt is paid off, apply that full amount to the next smallest. The payment grows like a snowball—getting bigger and more powerful with each win.

- Repeat Until All Debts Are Paid: Keep going until you’ve paid off your last debt. Celebrate each milestone, and stay consistent for the full journey.

You can use a spreadsheet, a printable tracker, or a budgeting app to monitor your snowball. As the wins accumulate, so will your confidence that you can become debt-free.

How Can The Debt Snowball Method Help You

Debt doesn’t disappear overnight, but the right strategy can help you stay motivated long enough to eliminate it. The debt snowball method makes progress feel real and rewarding, even when your balances are large. Here’s how this method creates momentum:

- Builds Confidence Early: Starting with your smallest debt gives you a quick win. Paying it off creates a sense of accomplishment that drives you to keep going.

- Simplifies the Process: You don’t need to worry about interest rates or complicated calculations. You follow the list and knock out one balance at a time.

- Reinforces Positive Habits: Each payoff strengthens your ability to stick with a plan. That feeling becomes addictive—in a good way—and leads to more informed financial decisions over time.

- Creates Emotional Motivation: Seeing a debt disappear is a satisfying experience. That emotional payoff is what keeps many people from giving up halfway through.

- Encourages Accountability: Sharing your goals with friends or family can enhance your commitment. The debt snowball method allows you to celebrate milestones with others, creating a support system that keeps you accountable and motivated.

This method transforms debt repayment into a personal challenge, creating a sense of progress that motivates you, even when the amounts seem large. This approach is especially beneficial for individuals who thrive on achieving small wins and feeling a sense of accomplishment. If you’re a person like that, then this method may be a great fit for you.

What Are The Drawbacks Of The Debt Snowball Method

Although the debt snowball method is motivational and easy to follow, it’s not the most cost-effective approach in terms of interest savings. That’s something to consider before diving in. Here are a few potential downsides:

- Ignores Interest Rates: Since you’re paying based on balance size, you might leave high-interest debts untouched longer. That can lead to paying more in interest over time.

- Not Ideal for Everyone: If you’re highly disciplined and motivated by saving money, the avalanche method—which targets high-interest debts first—may be a better fit.

- Takes Time to See Big Savings: Financially, the early wins don’t save much in dollars. You’ll need to be patient as you build momentum toward larger debts.

Despite these drawbacks, many people stick with the debt snowball because it works, especially for those who need visible progress and encouragement to stay committed.

Conclusion

The debt snowball method turns debt repayment into a step-by-step journey that builds confidence, discipline, and momentum. It’s a powerful strategy for anyone who needs motivation and structure to eliminate their debt.

To get more helpful money tips, subscribe to our blog, follow us on social media, and check out our YouTube channel for smart and practical videos.

Sources

- Photos: Unsplash: Pauline Bernfeld