Saving money doesn’t always require a massive lifestyle change. Sometimes, all it takes is a small, intentional action tied to your existing habits. In this post, I’ll walk you through savings triggers—a smart and flexible way to build your savings by linking them to everyday decisions. Let’s get started!

What Is A Savings Trigger

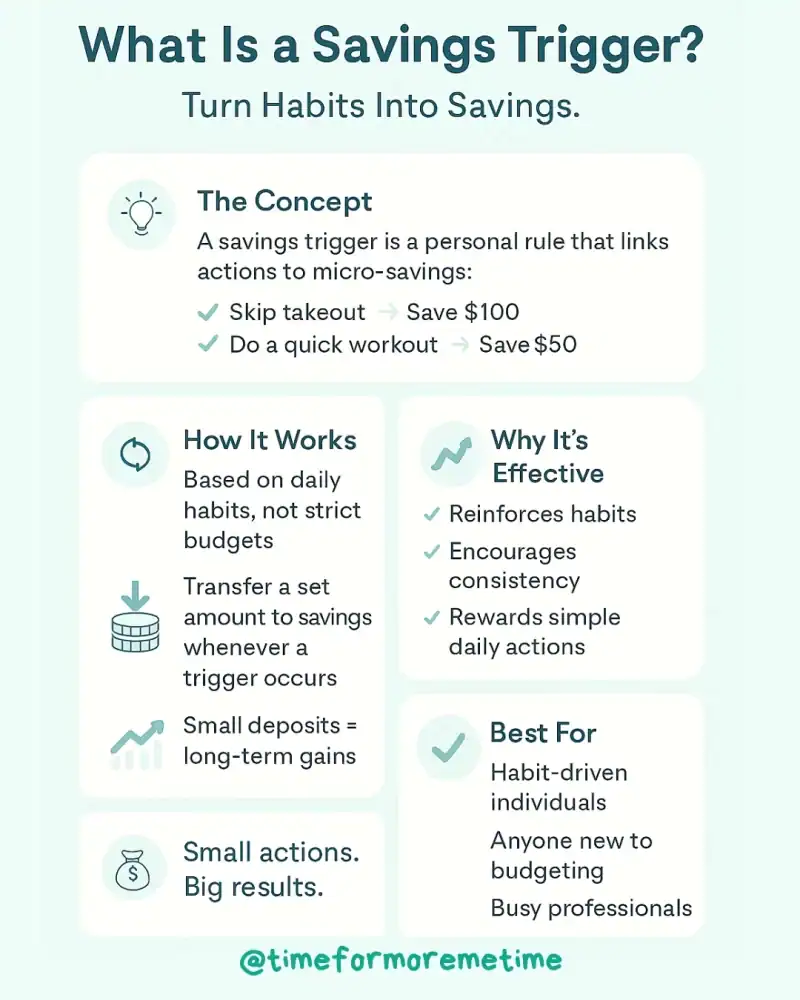

A savings trigger is a personal rule that links a specific action or behavior to a small deposit into savings. It’s a way to turn your everyday choices—like saying no to an online purchase or completing a workout—into meaningful financial wins.

Unlike setting aside a lump sum each month, this method is rooted in behavior-based saving. Each time the “trigger” occurs, you transfer a set amount of money into savings. Over time, these micro-savings add up, without requiring a strict budget or big sacrifice.

The savings trigger method works because it builds on behavior reinforcement. The action you complete—like skipping takeout—becomes a cue for saving money. You reward good choices with a financial boost to your future self.

Small, repeated actions—especially those tied to habits—can help people stay consistent with financial goals. That’s why savings triggers work well for those who struggle with traditional budgeting.

How To Set Up A Savings Trigger

Starting savings triggers doesn’t require any special tools—just awareness and a plan. They’re flexible enough to fit any lifestyle, whether you’re a spender, a saver, or somewhere in between. Here’s how to create your own trigger system in a few steps:

- Identify Your Habits: Start by listing regular behaviors, routines, or decisions that happen often—especially the ones tied to money or discipline. Some good examples are skipping takeout, finishing a workout, or choosing not to buy something online.

- Choose Your Triggers: Decide which actions or choices will trigger a savings deposit. Make sure they’re things that happen frequently enough to build momentum, but not so often that they become burdensome.

- Set a Savings Amount:

Pick a small, realistic dollar amount to save each time the trigger happens. This could be $1, $5, $10—whatever fits your budget. - Decide Where to Save: Use a separate savings account, a budgeting app, or even a physical cash jar. Label it clearly so you always know this money has a specific purpose.

- Track and Reward: Keep a simple record of your triggers—either on paper or in an app—and watch your savings grow. Celebrate your consistency to stay motivated.

If you want to automate this, consider using apps like Acorn. For example, you can set a rule like “Round up every purchase and save the difference,” or “Save $2 every time I complete a workout on my fitness app.”

Keep in mind that services like Acorn typically charge a monthly fee, which can range from $3 to $12. Therefore, if you plan to save less than $10 a month through rounding up or savings triggers, it might be better to start saving manually.

How Can A Savings Trigger Help You

Savings triggers can be surprisingly powerful, especially if you struggle with saving consistently or find it hard to cut back using traditional budgets. They create a natural rhythm for saving that fits into your daily routine, making progress feel effortless over time. Here are the reasons why:

- Make Saving Automatic and Effortless: By tying savings to behaviors, you don’t have to think twice or feel overwhelmed. You’re simply acting on a rule you’ve already set.

- Turn Everyday Wins into Progress:

Each time you skip a purchase or meet a goal, you get the satisfaction of seeing your savings grow. It turns self-control into a game with real rewards. - Build Financial Awareness:

Since triggers are based on your behavior, you’ll become more mindful of your spending patterns. You start noticing your habits—and adjusting them naturally.

Over time, savings triggers help reinforce positive habits. Additionally, it can also help reduce guilt associated with spending while showing you that even small amounts can lead to meaningful progress.

While I mentioned that this process can become effortless over time, it’s important to recognize that it will still require some willpower. I will discuss this aspect further in the next section.

What Are The Drawbacks Of A Savings Trigger

While savings triggers are a creative and low-pressure way to build savings, they’re not without limitations. Like any method, they work best when tailored to your habits and backed by consistency. Here are a few to keep in mind:

- Depend on Self-Discipline:

If you’re manually transferring money, it’s easy to forget or skip the action—especially when life gets busy or you lose motivation. - May Not Add up Quickly:

Since the amounts are small, it may take some time to see significant results. If you’re saving for something big, this method works best alongside a larger savings plan. - They Can Be Inconsistent:

If your chosen triggers don’t happen often—like skipping lattes or workouts—you may go weeks without saving. Choosing the right habits is key to building consistency.

That said, many people find savings triggers effective because they’re low-pressure, flexible, and rooted in daily life. It’s not about saving a fortune at once—it’s about building a habit that sticks.

Conclusion

Savings triggers are a simple, flexible way to grow your savings one small decision at a time. By linking savings to your daily actions, you can make steady progress without feeling deprived or overwhelmed.

To get more helpful money tips, subscribe to our blog, follow us on social media, and check out our YouTube channel for smart and practical videos.

Sources

- Photos: Unsplash: Mockuuups