Money often feels tight right after the holidays. Extra spending, delayed bills, and uneven paychecks can make January feel heavier than expected. That pressure builds quickly when expenses arrive before finances have time to recover.

I started paying closer attention to this pattern after seeing how post-holiday spending affected short-term cash flow more than the rest of the year. The small decisions I made in December often created bigger constraints in January. Working through that cycle showed me how important early adjustments can be.

In this post, I’ll explain practical ways to scrounge up money after the holidays without creating new problems. You’ll see where cash can be freed up quickly, which moves help most in the short term, and how to regain control before financial stress sets the tone for the year. Let’s get started!

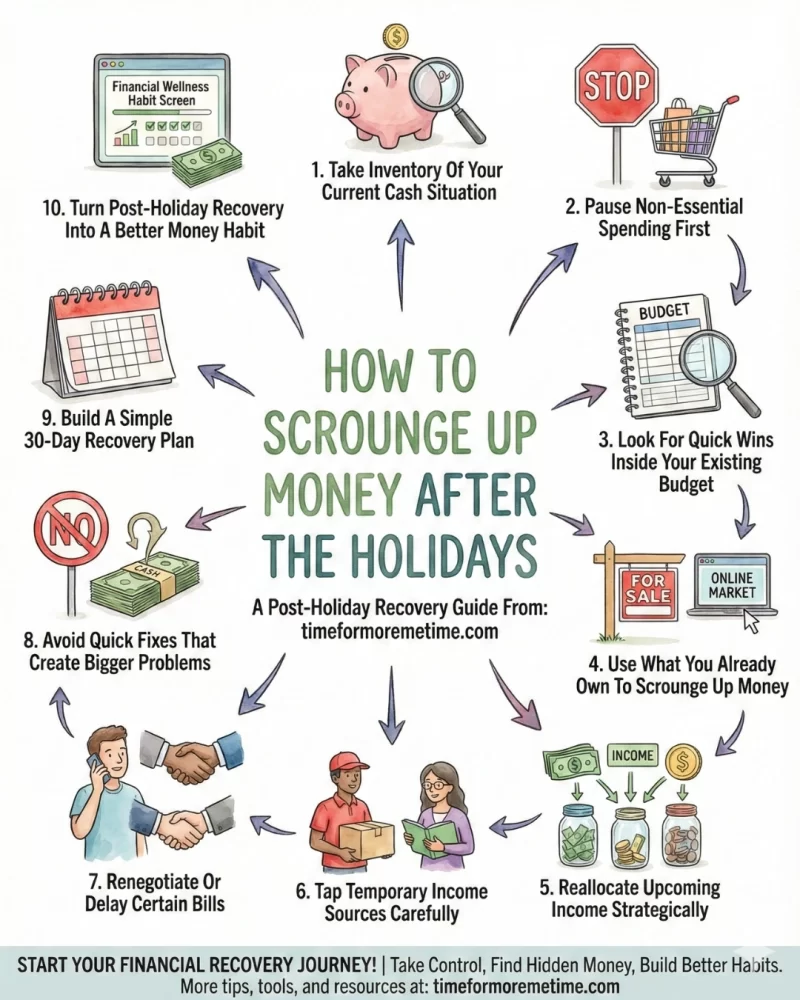

1. Take Inventory Of Your Current Cash Situation

The first step is understanding where your money stands right now. Post-holiday stress often comes from uncertainty rather than the numbers themselves. But when you look at balances, it brings clarity.

Start by reviewing checking, savings, and upcoming bills. Separate what is due immediately from what can wait. This helps you see whether the issue is a short-term gap or a deeper problem.

Once everything is visible, decisions become easier. You stop guessing and start responding with intention.

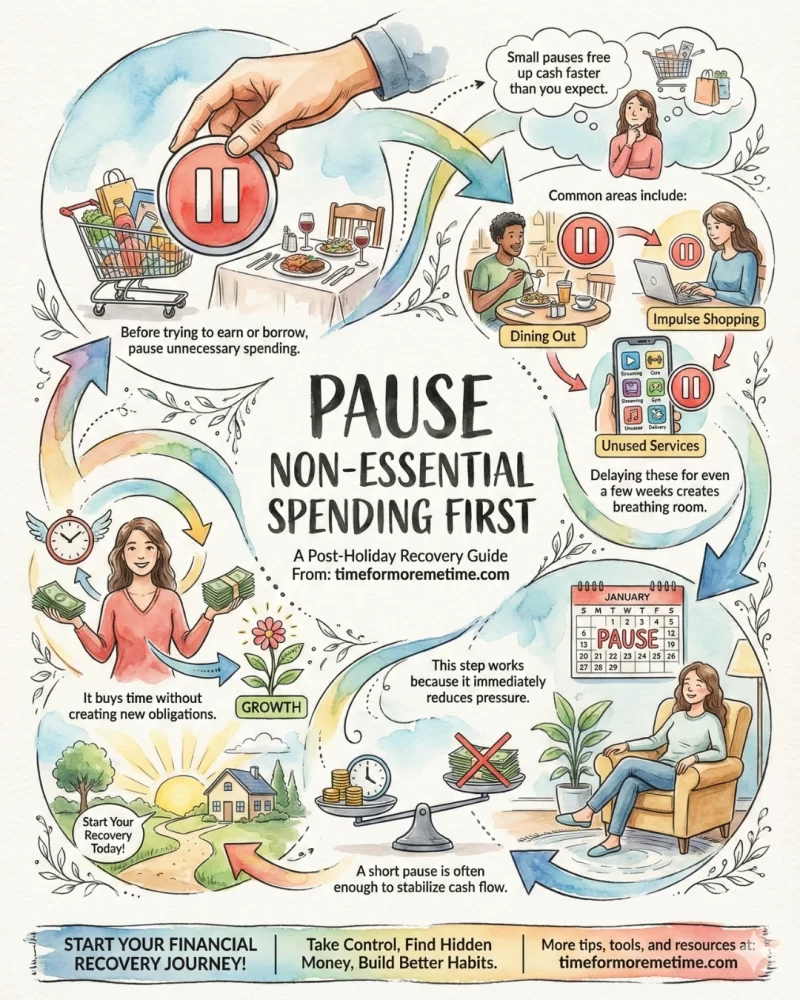

2. Pause Non-Essential Spending First

Before trying to earn or borrow more money, pause unnecessary spending. Small pauses can free up cash faster than most people expect.

Common areas include dining out, impulse shopping, and unused services. Delaying these for even a few weeks creates breathing room. This step works because it immediately reduces pressure.

A short pause is often enough to stabilize cash flow. It buys time without creating new obligations.

3. Look For Quick Wins Inside Your Existing Budget

Quick wins often hide in categories that change each month. Spending on food, entertainment, and convenience typically goes up during the holidays.

Many find extra cash by bringing these expenses back to normal. One smart way to save is to start shopping early. In fact, 68% of holiday shoppers begin before Thanksgiving, which helps them save money.

Even cutting back on one or two categories can quickly free up cash. These small changes can add up fast and work best when temporary.

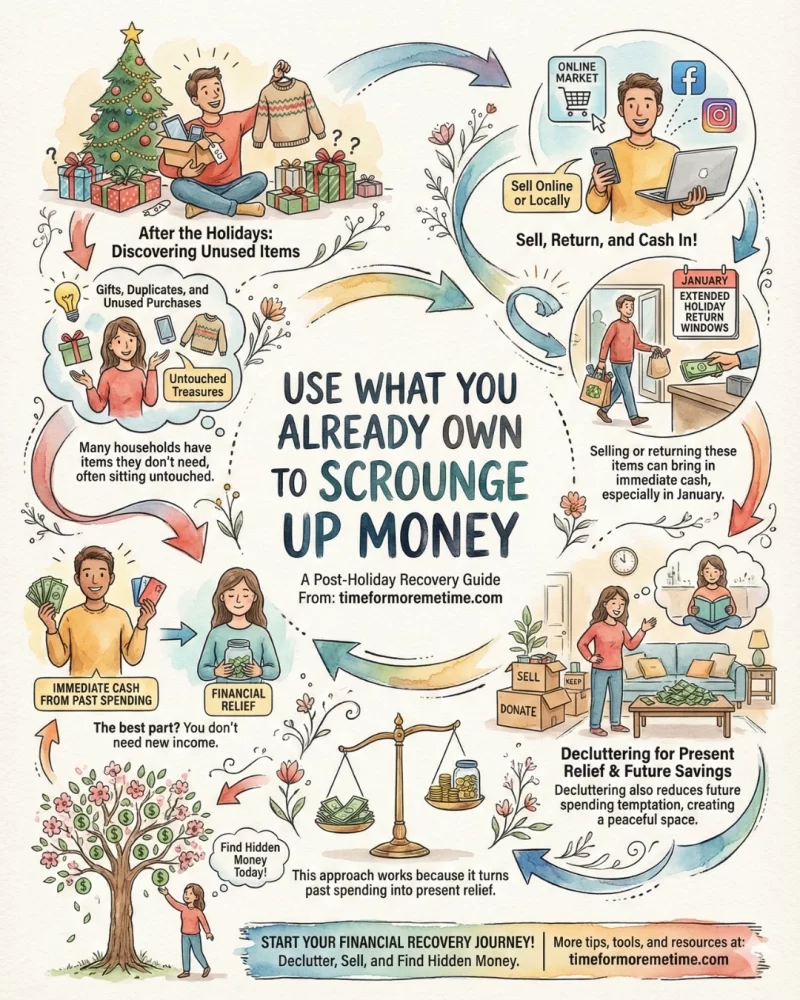

4. Use What You Already Own To Scrounge Up Money

After the holidays, many households have items they don’t need. Gifts, duplicates, and unused purchases often sit untouched.

After the holidays, many people return or resell items they don’t end up using. Selling or returning these items can bring in immediate cash. Extended holiday return windows make this easier in January. Decluttering also reduces future spending temptation.

This approach works because it turns past spending into present relief. The best? You don’t need new income.

5. Reallocate Upcoming Income Strategically

Once spending is paused and quick wins are identified, attention naturally shifts to incoming income. January paychecks often disappear faster than expected when they’re not planned for. Bills, catch-up spending, and routine expenses tend to collide all at once.

Reallocating income before it arrives changes that pattern. Essentials come first, followed by the most urgent recovery needs. This approach reduces the feeling that money is gone the moment it hits your account.

Planning also lowers decision fatigue. When income already has an assignment, fewer choices are needed in the moment. That structure keeps progress steady instead of reactive.

6. Tap Temporary Income Sources Carefully

Even with better planning, small gaps can remain. That’s usually when people start thinking about extra income. Short-term income can help, but only when it serves a clear purpose.

Temporary income works best when it fills a specific need, such as covering a bill or rebuilding a small buffer. Problems start when extra work becomes a long-term fix or drains energy. Relief should not create a new strain.

Choosing options that fit your time and energy keeps this step helpful. Used carefully, short-term income can stabilize cash flow without taking over your schedule.

7. Renegotiate Or Delay Certain Bills

If income adjustments still feel tight, timing becomes the next lever. Not every bill requires immediate payment, even if it appears fixed. Many providers offer flexibility when contacted early.

Payment extensions or short-term arrangements can ease pressure without long-term damage. These conversations are often simpler than expected because companies prefer communication over missed payments. Avoiding the issue usually increases stress.

Even minor timing adjustments can change the month. Extra breathing room allows other recovery steps to take effect instead of piling pressure into one week.

8. Avoid Quick Fixes That Create Bigger Problems

As pressure builds, fast solutions start to look appealing. High-interest options promise speed when patience feels unavailable. That urgency is precisely what makes them risky.

These fixes often trade short-term relief for long-term strain. Fees and interest quietly extend recovery well beyond January. Evaluating the actual cost matters more than how fast the money arrives.

Restraint at this stage protects future stability. Avoiding harmful shortcuts keeps recovery simple instead of complicated.

9. Build A Simple 30-Day Recovery Plan

After addressing spending, income, and timing, direction becomes the focus. Recovery works best when it stays contained. A 30-day window keeps expectations realistic and manageable.

Choose one or two priorities only. Rebuilding cash or catching up on a bill is enough. Trying to fix everything at once often leads to frustration and stalled progress.

Short plans rebuild confidence. Each completed step replaces panic with momentum and reinforces control.

10. Turn Post-Holiday Recovery Into A Better Money Habit

Once stability returns, the experience itself becomes useful. Post-holiday pressure highlights patterns that tend to repeat each year. Ignoring those signals often leads back to the same cycle.

Using this moment to adjust habits improves future outcomes. Planning earlier for holiday spending or building a buffer reduces the impact next time. Small changes shorten recovery every year.

What begins as damage control can become a stronger system. When lessons carry forward, January stops feeling like a setback and starts feeling manageable.

Conclusion

Scrounging up money after the holidays is about regaining control, not fixing everything at once. Small, practical steps can ease pressure and restore balance quickly.

For more practical money strategies like this, read our latest posts, follow us on social media, and visit our YouTube channel for clear guidance you can use right away.

Source

- Photo: Pexels: Leeloo The First