Many people worry about whether free financial apps are truly safe, especially when they handle personal data. That applies to Credit Karma, too, mainly since the platform has grown in popularity. Before you use its free tools and other features, let’s look at its safety and accuracy. Let’s get started!

What Credit Karma Offers In 2025

Credit Karma has grown into much more than a credit score app. In 2025, it positions itself as a financial hub designed to give users a clearer picture of their credit health and basic money management. Members can view their credit scores from TransUnion and Equifax, track progress over time, and receive alerts about changes in their reports.

The platform also provides access to personalized recommendations, such as credit cards, loans, or savings products that might fit your profile. These suggestions enable users to explore financial options while maintaining a free service. In short, Credit Karma offers a gateway into understanding and improving personal credit.

Key Features

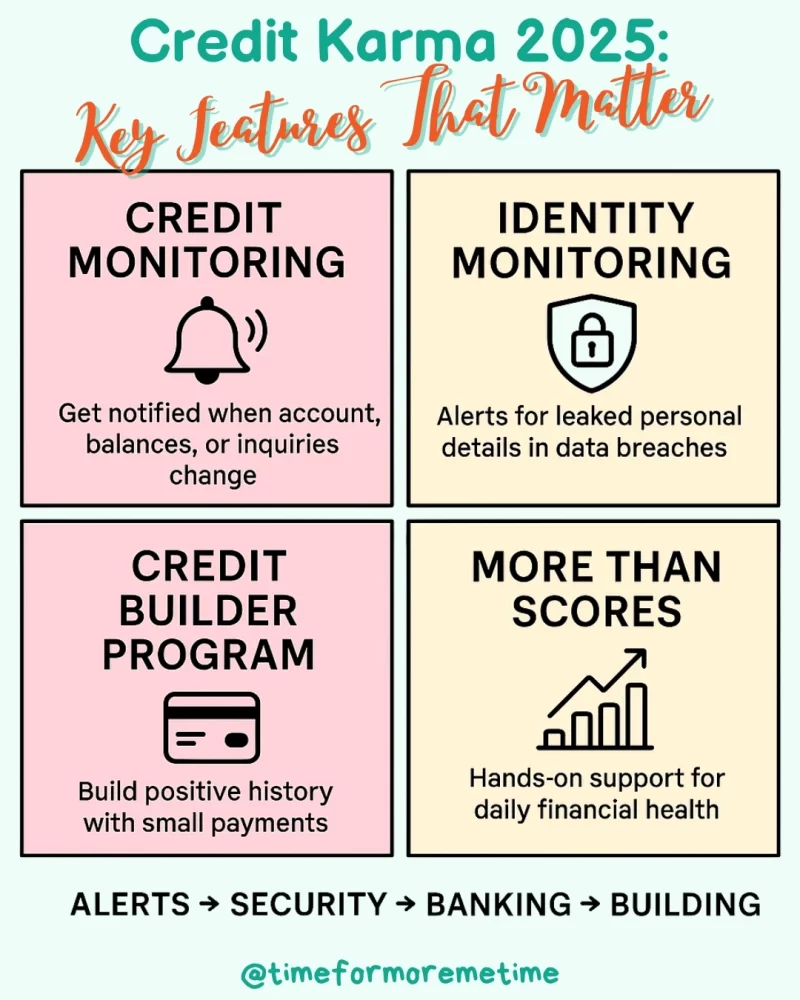

Credit Karma isn’t just about showing credit scores—it provides practical tools that support everyday financial management. Credit monitoring alerts users whenever accounts, balances, or inquiries change, which helps identify potential fraud early. Identity monitoring adds another safeguard by checking for leaked personal details in data breaches.

For daily money use, Credit Karma Money offers FDIC-backed checking and savings accounts through partner banks. Those working to improve their credit can also use the Credit Builder program, which builds positive payment history with small, manageable payments. These features make Credit Karma a hands-on companion, not just an information source.

Privacy And Data Use

Along with security, privacy is one of the top concerns for users in 2025. Credit Karma’s business model is free for consumers, which means revenue comes from recommending financial products based on user credit profiles. These offers are tailored, but they also mean that some personal data is shared with partner institutions.

The company has stated it doesn’t sell sensitive personal details outright, but it does use credit information to match users with offers. Understanding this trade-off is essential—free access to scores and reports is balanced by marketing and data-sharing practices behind the scenes.

Security Practices

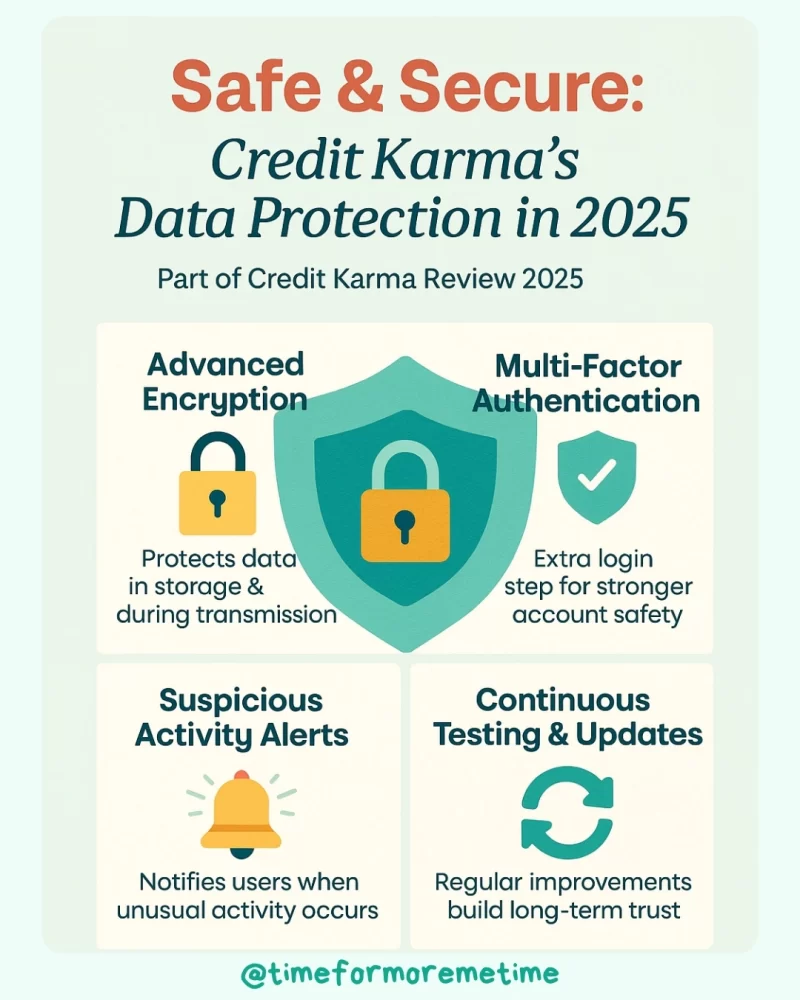

Credit Karma knows that trust begins with keeping user data secure. To protect sensitive information, the platform relies on advanced encryption for data both in storage and during transmission. This ensures personal details are shielded from unauthorized access.

Multi-factor authentication adds an extra step, making it harder for intruders to log in even if passwords are compromised. Users also receive alerts if suspicious activity is detected, allowing them to act quickly. With continuous system testing and updates, Credit Karma shows a steady commitment to safety. While no system is perfect, these measures build a strong foundation of confidence.

Accuracy And Limits

Credit Karma’s scores give users a reliable snapshot of credit health, but they are not the same as the FICO scores most lenders use. FICO, created by the Fair Isaac Corporation, is the industry standard for mortgage, auto loan, and credit card decisions. In contrast, Credit Karma provides VantageScore 3.0 from TransUnion and Equifax.

Both models consider similar factors, such as payment history and credit utilization, but they weigh them differently. As a result, your Credit Karma score may be higher or lower than a lender’s FICO score. This makes it best for tracking trends, not exact approval outcomes.

Incidents And Legal Issues

Like many large platforms, Credit Karma has faced challenges with regulation and public trust. In 2022, the Federal Trade Commission penalized the company for presenting some credit offers as “pre-approved,” even though many users were later denied. This led to a settlement and changes in how offers are advertised.

The company has also been named in lawsuits related to data use and consumer transparency. While no major data breaches have been reported, these incidents highlight the importance of reading policies carefully. The good news is that Credit Karma has improved communication and tightened compliance since then.

Pros And Cons

Before deciding whether to use Credit Karma, it’s important to look at both the positives and the drawbacks. Understanding these points will give you a clearer view of what the platform can and cannot do for you.

Pros:

Credit Karma has several strengths that explain its continued popularity among users. Some of which are as follows:

- Free weekly credit scores and reports from two major bureaus

- Credit and identity monitoring included at no cost

- Extra services like Credit Karma Money and Credit Builder

- Easy-to-use interface that works well for beginners

Together, these advantages make Credit Karma a powerful free resource for anyone who wants to stay informed about their credit and catch potential issues early.

Cons:

There are also some limitations that users should keep in mind before relying solely on Credit Karma. Here are some of them:

- Uses VantageScore instead of FICO, leading to differences with lender results

- Lacks Experian data, leaving out one-third of your credit profile

- History of regulatory issues with marketing practices

- Provides limited identity protection compared to paid services

These downsides don’t erase its value but show that Credit Karma works best as a starting point. It should be paired with other tools or official reports when making major financial decisions.

Comparisons In 2025

In 2025, Credit Karma competes with both free apps and premium credit services. Compared to paid options like myFICO, it falls short because it doesn’t include Experian data or official FICO scores. However, it wins on cost since everything is free.

When compared to full identity-theft protection services, Credit Karma provides monitoring but not recovery assistance or insurance coverage. For budgeting and money management, apps like YNAB or PocketGuard may offer better tools.

Still, Credit Karma remains the go-to choice for anyone who wants accessible, no-cost credit monitoring without the complexity of premium platforms.

Who Credit Karma Is Best For

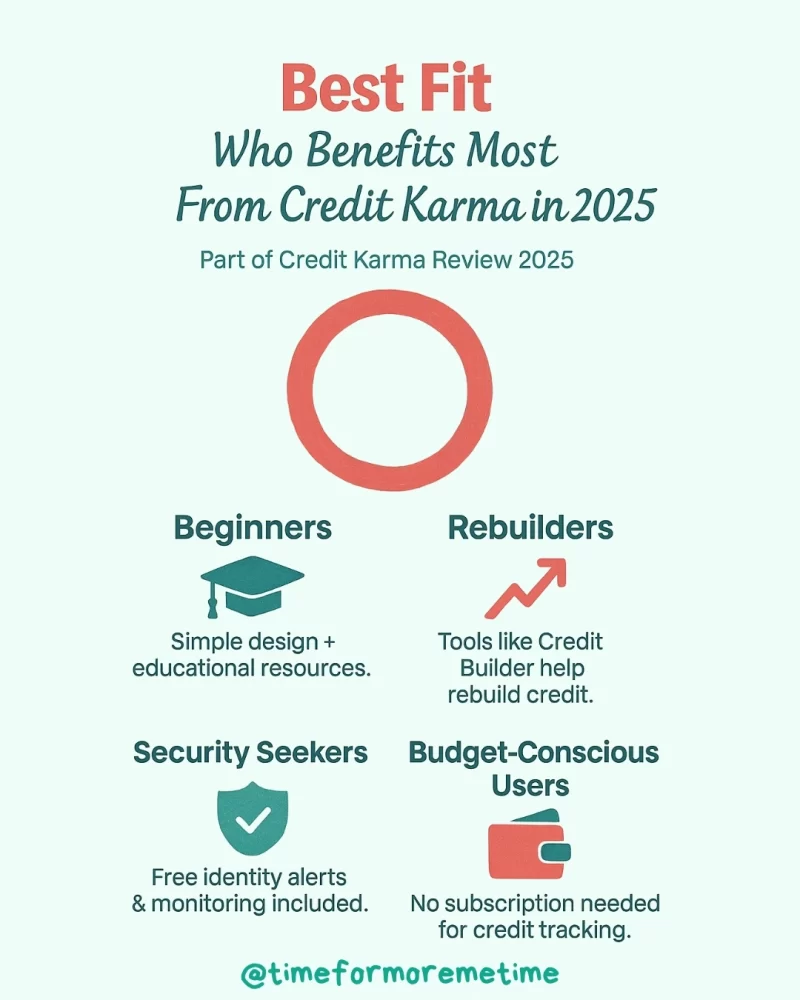

Credit Karma is ideal for people who want to track their credit without paying for a subscription. Beginners benefit from its simple design and educational resources, while those rebuilding credit can take advantage of tools like Credit Builder.

It’s also a good fit for anyone who values free identity alerts and likes having financial product recommendations tailored to their profile. However, those who need Experian data, FICO scores, or robust identity protection should consider alternative services.

Ultimately, Credit Karma works best as a starting point for staying informed about your credit health.

Verdict: Is Credit Karma Safe In 2025

Using Credit Karma isn’t about finding a perfect financial tool—it’s about having a free, reliable system to stay informed and protect your credit health. With realistic expectations, it can help you track progress, catch issues early, and feel more confident about your finances.

Interested in more reviews of financial tools like Credit Karma? Subscribe to our blog, follow us on social media, and visit our YouTube channel for honest insights into the apps and services that can help you manage money smarter in 2025.

Source

- Photo: Pexels: Mikhail Nilov