Budgeting feels very different once your money decisions start affecting more than just you. When you budget alone, choices are personal and flexible. When you budget as a family, every decision connects to shared needs, shared goals, and shared consequences.

That’s because family budgets introduce responsibility in a new way. It’s no longer about optimizing your own spending. It becomes about stability, predictability, and making sure everyone’s needs are covered, even when life changes unexpectedly.

In this post, let’s break down how family budgets differ from single budgets while making it feel more realistic and less frustrating. Let’s get started!

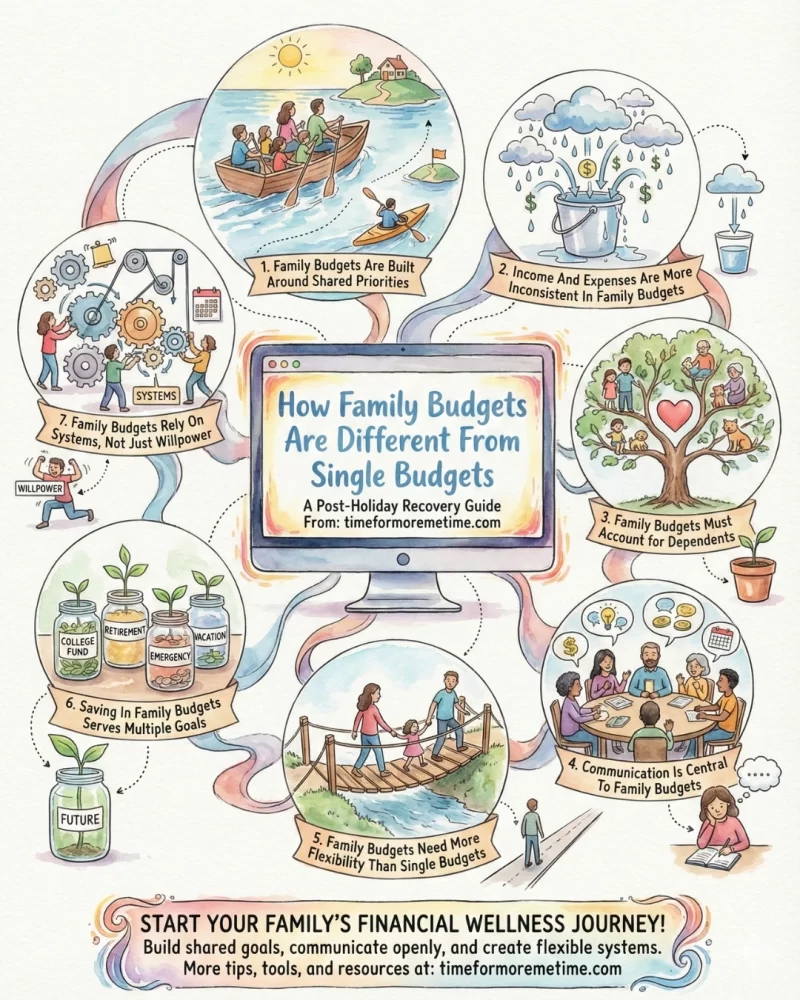

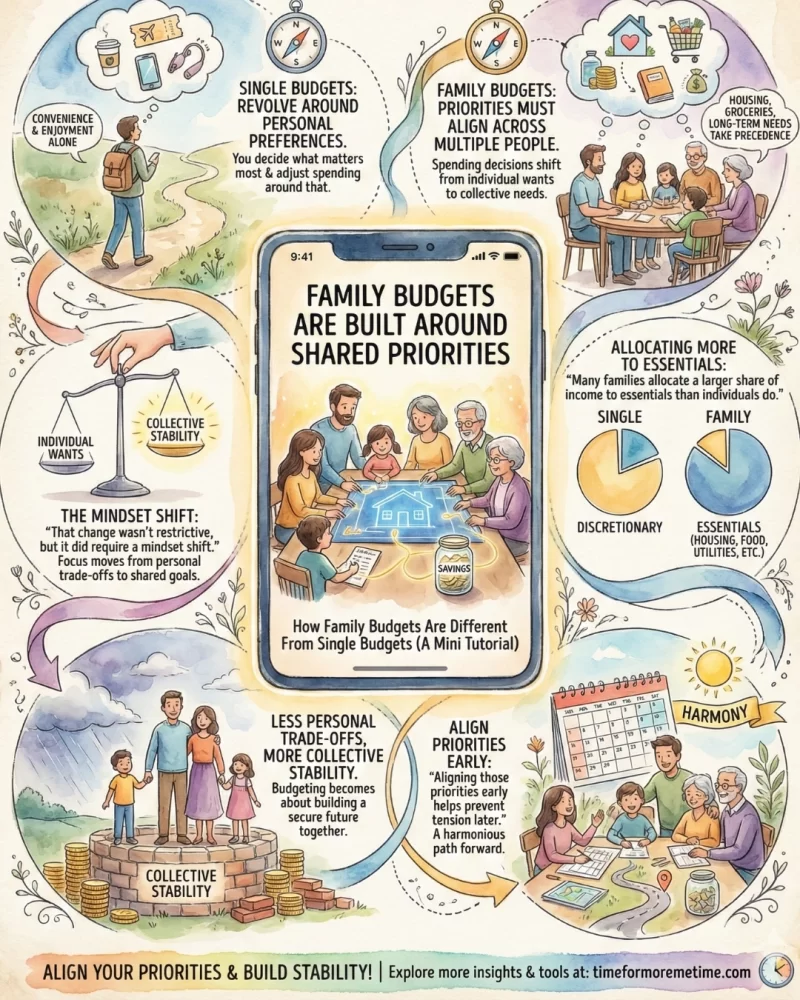

1. Family Budgets Are Built Around Shared Priorities

Single budgets usually revolve around personal preferences. You decide what matters most and adjust spending around that. Budget making for families work differently because priorities must align across multiple people.

I felt this shift clearly when spending decisions stopped being about convenience or enjoyment alone. Housing, groceries, and long-term needs began to take precedence over my individual wants. That change wasn’t restrictive, but it did require a mindset shift.

And I’m not alone in this: many families allocate a larger share of their income to essentials than individuals do. When priorities are shared, budgeting becomes less about personal trade-offs and more about collective stability. Aligning those priorities early helps prevent tension later.

2. Income And Expenses Are More Inconsistent In Family Budgets

Budgeting alone often means dealing with one paycheck and fairly predictable expenses. Family budgets rarely work that way, since income arrives at different times and expenses shift from month to month. That difference changes how steady money feels, even when the total income stays the same.

I remember months that felt fine and others that felt uncomfortable, even though nothing major had changed on paper and cash on the side is left untouched. Bills landed unevenly, and paydays didn’t line up the way I expected. That timing created pressure that didn’t show up in the numbers but was easy to feel day to day.

When income and expenses move out of sync, the strain shows up quickly. Planning starts to feel reactive, and confidence in the budget slips. Family budgets work better when flexibility is built into the structure rather than added after problems arise.

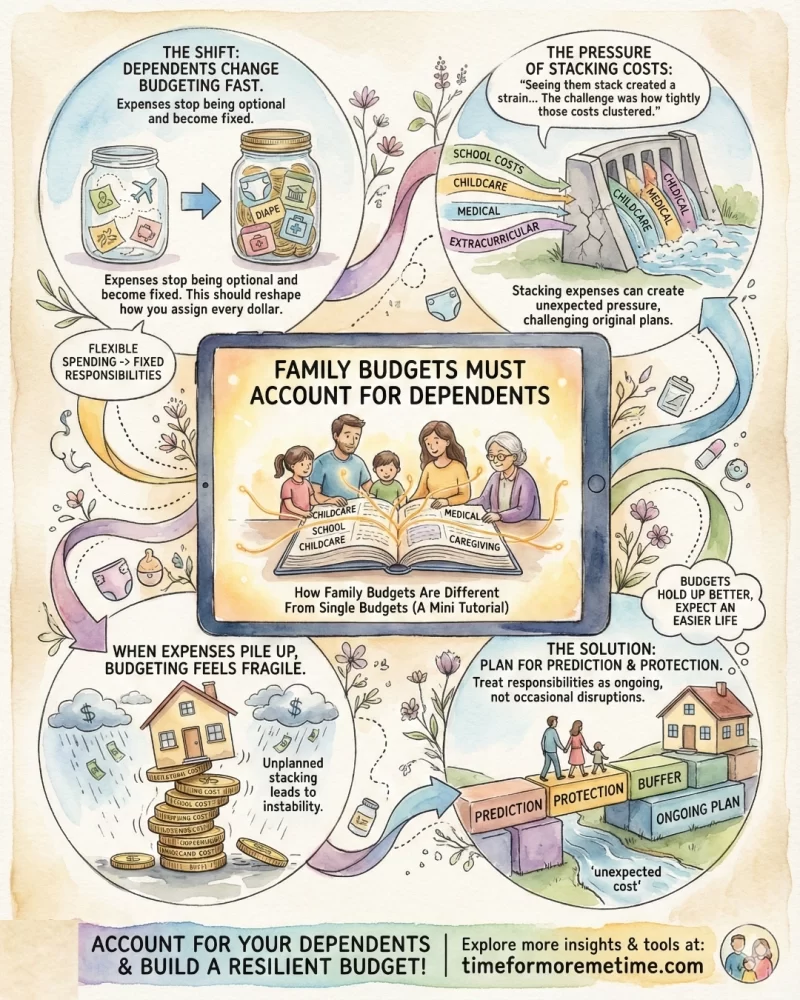

3. Family Budgets Must Account For Dependents

Dependents change budgeting faster than most people expect. Once children or caregiving responsibilities enter the picture, expenses stop being optional and start becoming fixed. That shift should reshape how you assign every dollar.

Where I work, colleagues there who started budgeting comfortably and then felt pressure once school costs and childcare expenses landed close together. Each expense made sense on its own, yet seeing them stack created a strain that their original plans were not built to absorb. The challenge was not the amount but how tightly those costs clustered.

When dependent expenses pile up, budgeting starts to feel fragile. In order to prevent this, you should start planning for prediction and protection. Once you treat these responsibilities as ongoing rather than occasional disruptions, your family budgets hold up better and you can expect an easy life.

4. Communication Is Central To Family Budgets

Money conversations usually show up during everyday decisions. It comes up while shopping for groceries, booking appointments, or agreeing to a purchase that affects something else later. In family budgets, these moments pile up quickly when spending decisions happen without shared context.

This commonly plays out in most families in America. Once families started talking more openly about money and effectively delegating expenses, their expectations aligned more naturally and decisions stopped feeling personal. As a result, they were able to resolve disagreements easily, if not lessen them. They no longer guess expenses once they started discussing their budgets.

As communication improves, budgeting feels lighter. Fewer surprises show up, and fewer decisions need repair after the fact.

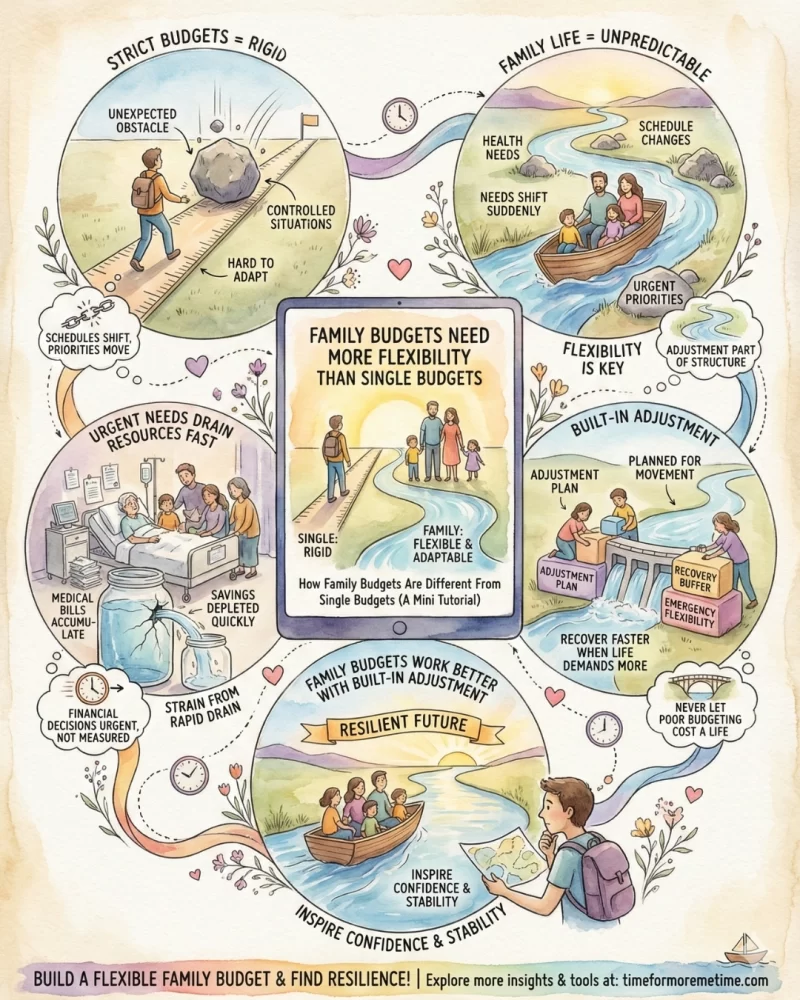

5. Family Budgets Need More Flexibility Than Single Budgets

Strict budgets can work in controlled situations. However, family life rarely stays controlled for long. Schedules shift, health needs appear, and priorities move without warning.

When my grandmother’s health declined, I experienced this. At that time, our family tried everything we could to support her care. Medical bills accumulated, savings were depleted faster than planned, and financial decisions became urgent rather than measured. The strain came from how quickly our resources drained.

That’s what I promise myself: never let poor budgeting cost us anyone’s life. Family budgets work better when adjustment is already part of the structure. Now, I made sure plans can move and recover faster when life demands more.

6. Saving In Family Budgets Serves Multiple Goals

Saving feels different once more people rely on it. In single budgets, money often moves toward one goal at a time—like if you want to get rich. In family budgets, several needs sit side by side, all competing for attention.

People always try to keep all their savings in one place. Emergency needs, school costs, and future plans were pulled from the same pool. This makes progress feel scattered. Things changed once they separated their savings by purpose because each goal finally had its own space.

This approach matters once you look at the numbers. Only 46% of US households can cover three months of expenses with savings, which shows how easily uncertainty creeps in when money has no clear role. Family budgets benefit from clear saving categories because that structure removes hesitation and gives each dollar a purpose. Saving then starts to feel steadier and more intentional.

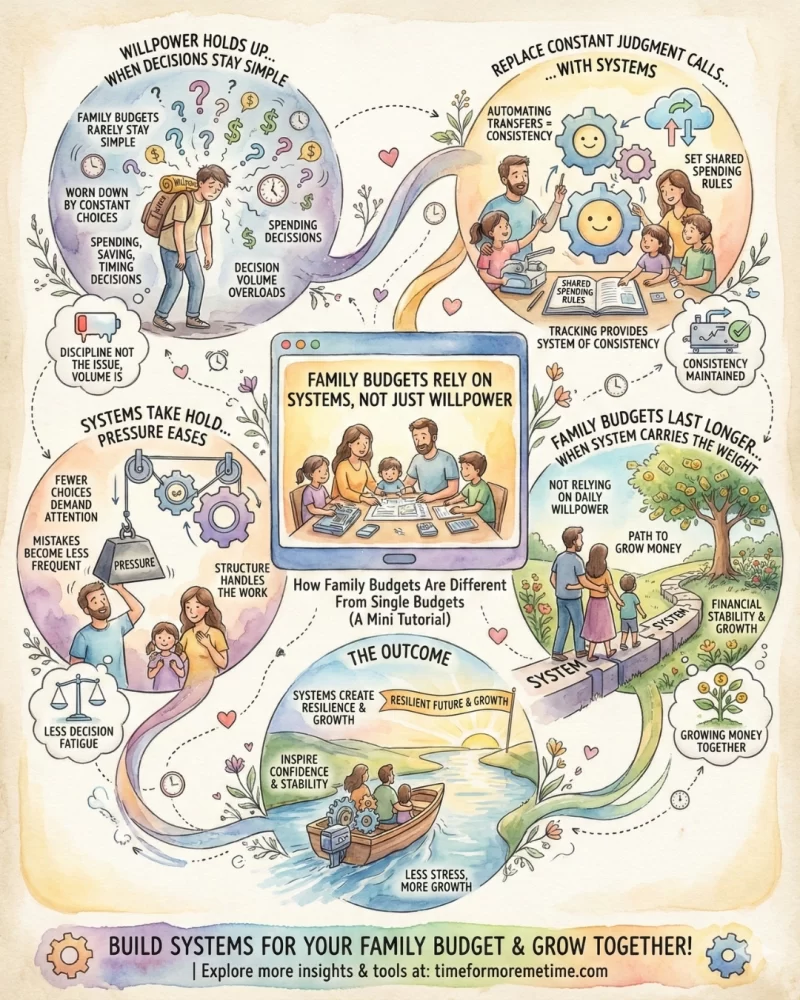

7. Family Budgets Rely On Systems, Not Just Willpower

Willpower holds up when decisions stay simple, but family budgets rarely stay that way. I’ve seen this with people close to me who started strong, only to feel worn down by constant choices about spending, saving, and timing. It wasn’t that they lacked discipline. The volume of decisions made makes maintaining consistency difficult.

Things started to settle once they replaced constant judgment calls with systems. For instance, a friend of mine shared how automating transfers and setting a few shared spending rules changed everything at home. They no longer have to debate or discuss money decisions, since tracking has given them a system of consistency.

As those systems took hold, the pressure eased. Fewer choices demanded attention, and mistakes became less frequent because the structure handled most of the work. Family budgets tend to last longer when the system carries the weight instead of relying on daily willpower. And if lucky, this may lead to a path where the family can grow money.

Conclusion

Family budgets differ from single budgets because responsibility is shared. Every decision affects more than one person, which changes how we must manage money.

If you want to learn more effective budgeting habits and a system for managing your finances, read our latest posts, follow us on social media, and visit our YouTube channel for clear guidance you can apply confidently.

Source

- Sources: Pexels: Kampus Production