There are moments when I look back and realize how much time I spent learning things the hard way. Not because I ignored advice, but because I never had access to the right guidance early on. Money wasn’t something my family discussed strategically growing up. It was something we survived around.

I grew up watching utilities get shut off, meals stretch further than they should, and stress sit quietly in the background of everyday life. Later, I earned degrees, built a career in radiation oncology, and eventually paid off over $90,000 in student loans and credit card debt. The progress came, but it took longer than it needed to.

I learned many important lessons that I wish I had known when I was a kid. If I could sit down with my younger self, I would share these lessons. Now, I want to share them with you. So, let’s get started!

1. Master Money’s Dynamics

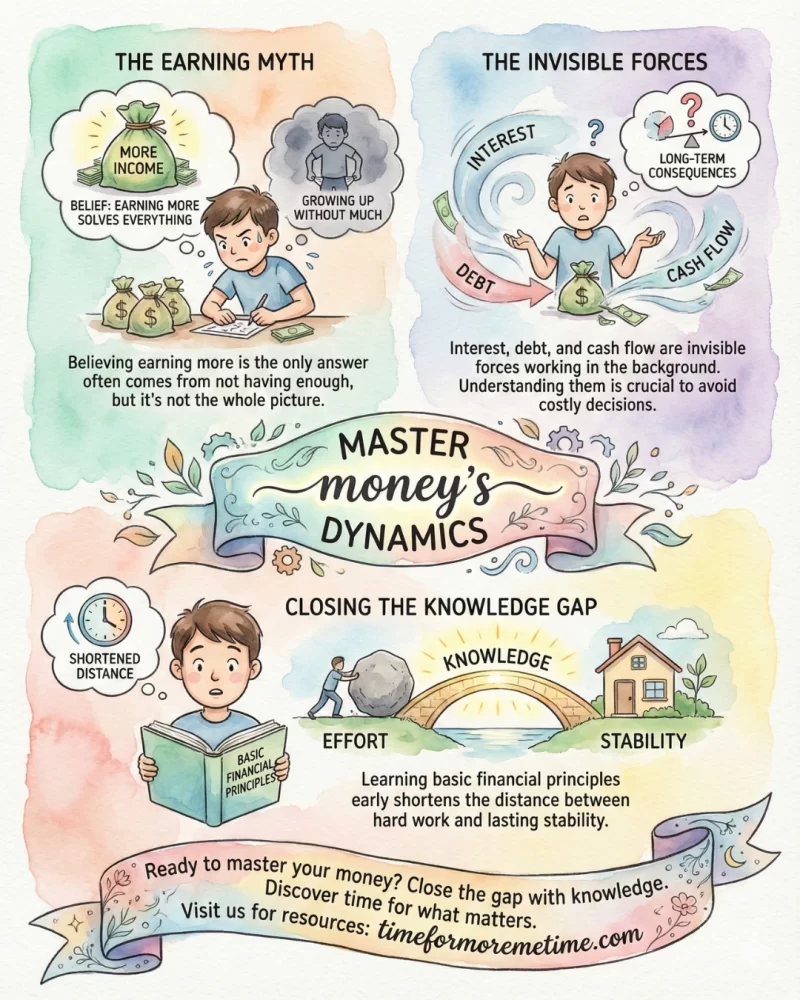

Learn how money works before you start earning it. For a long time, I believed that earning more would solve everything. That belief came from growing up without much money. When you don’t have enough income, it feels like the only answer.

What I didn’t understand early on was how money actually behaves. Interest, debt, and cash flow were invisible forces working quietly in the background. Without understanding them, I made decisions that seemed reasonable at the time but had long-term consequences.

I entered adulthood knowing how to work hard, but I didn’t really understand how to make money work for me. That gap cost me years. Learning basic financial principles earlier would have shortened the distance between effort and stability.

2. Confront Debt’s Control

Debt is a normal part of life, but it can control you if you let it. At first, debt doesn’t seem too bad. Monthly payments feel small, and the total amount looks temporary. But things change when debt starts affecting your choices.

I carried student loan debt while building my career and didn’t fully appreciate how much freedom it was costing me. Decisions about where to live, how much to save, and how much rest I could afford were all filtered through debt obligations.

The hardest part was how debt extended timelines. That’s why my goals took longer while flexibility shrank, making my time more expensive. If I had treated debt reduction as a priority earlier, I would have reclaimed years that I can’t get back.

3. Mitigate Lifestyle Inflation

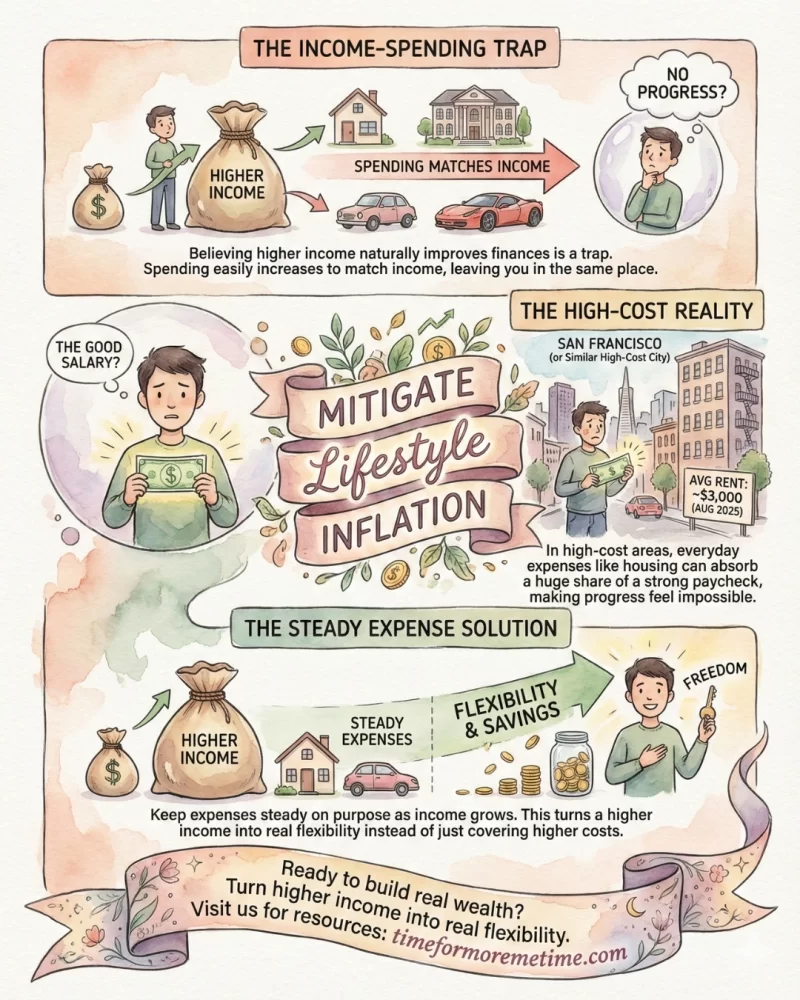

Lifestyle inflation can delay your financial freedom more than just having a low income. I used to think that as my income grew, my financial situation would improve naturally. That idea stuck with me even when my job got better. What surprised me was how easily my spending increased to match my income.

Living and working in San Francisco made that reality hard to miss. I saw people earning solid salaries who still felt financially boxed in because their everyday costs kept climbing alongside their income. By August 2025, around $3,000 is the average rent for a one-bedroom apartment in SF. This meant housing alone could absorb a huge share of an otherwise strong paycheck.

This pressure changes how you view progress. Instead of relief from pay raises, many people just stay in the same place financially. I found that keeping some expenses steady on purpose helped me turn a higher income into real flexibility instead of just covering higher costs.

4. Elevate Time’s Value

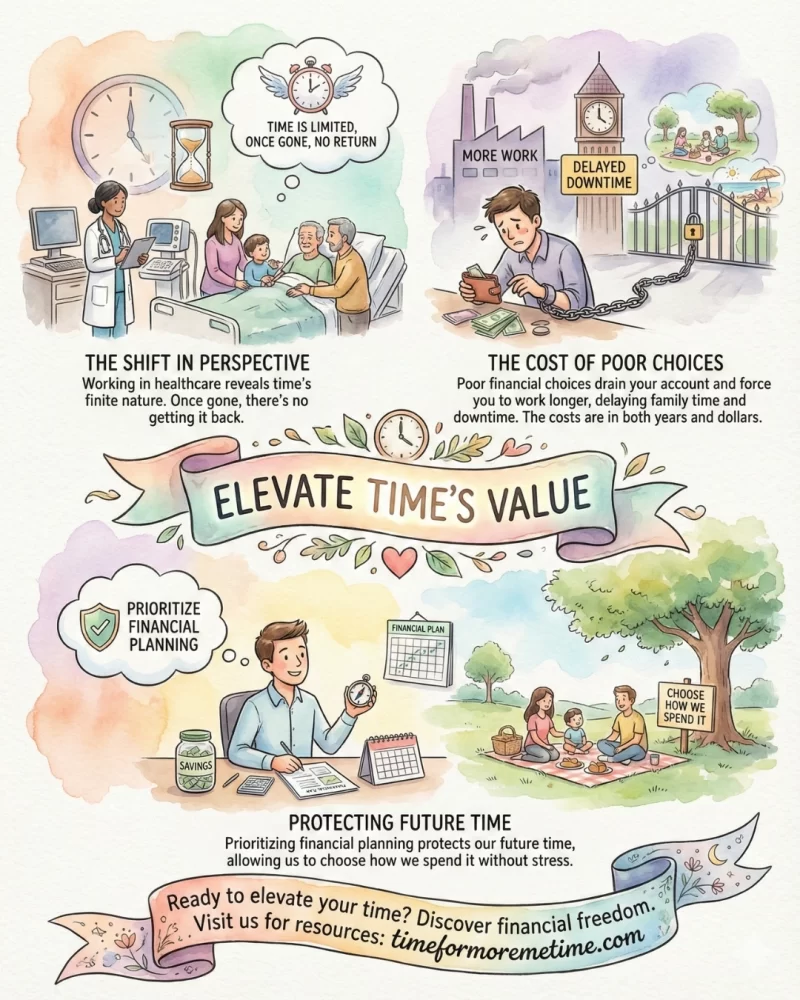

Working as a medical dosimetrist changed how I think about time in a way nothing else ever did. Watching patients and families navigate serious illness makes one thing very clear. Time is limited, and once it’s gone, there’s no getting it back.

This perspective shifted how I view money. Poor financial choices will drain your bank account. It will also force you to work longer, delay your downtime, and put family time further away. The costs show up in both years and dollars.

Before I found stability, I took on many different jobs. I washed dishes, worked in retail, and did warehouse labor. Each job taught me about resilience and showed me how valuable time is when money is tight. Now, I prioritize financial planning because it helps protect our future time, allowing us to choose how we spend it without stressing about making the right decisions.

5. Establish A Financial Plan

Make a financial plan early so that managing money doesn’t take too much discipline later. For a long time, I tried to handle my money just by putting in effort. I wrote down my expenses, checked my bank balance often, and made daily decisions about where to focus. This worked when life was simple and my energy was high.

As my responsibilities grew, this method became hard to maintain. Everything changed when I got tired of daily tracking. Now, I follow my financial plan, which accounts for everything. Instead of noting every single expense, I set a fixed amount I can spend. Any money I don’t use goes into savings at the end of the month. I also follow clear rules based on my plan, which makes it easier than trying to remember everything.

Once I started following my financial plan, my progress became steady instead of exhausting. This consistency helped me pay off debt, rebuild stability, and even support my parents in remodeling their home. My plan kept my momentum going, even when my motivation dipped, and helped me move forward.

Conclusion

The financial advice you wish you had heard earlier often becomes clear only after years of trial and error. Looking back, the biggest lessons aren’t about earning more, but about my understanding of how money decisions shape time, freedom, and long-term stability.

If you want to apply these financial lessons now instead of wishing you had learned them sooner, read our latest posts, follow us on social media, and visit our YouTube channel for practical guidance you can apply right away.

Source

- Photo: Pexels: Andrea Piacquadio