Lending money to family or friends is common, but it can get complicated fast. Many people want to help, yet loans without clear boundaries often lead to stress or broken trust. The good news is that you can support loved ones while also protecting yourself. With a clear plan in place, lending money becomes less risky and more respectful for both sides. Let’s get started!

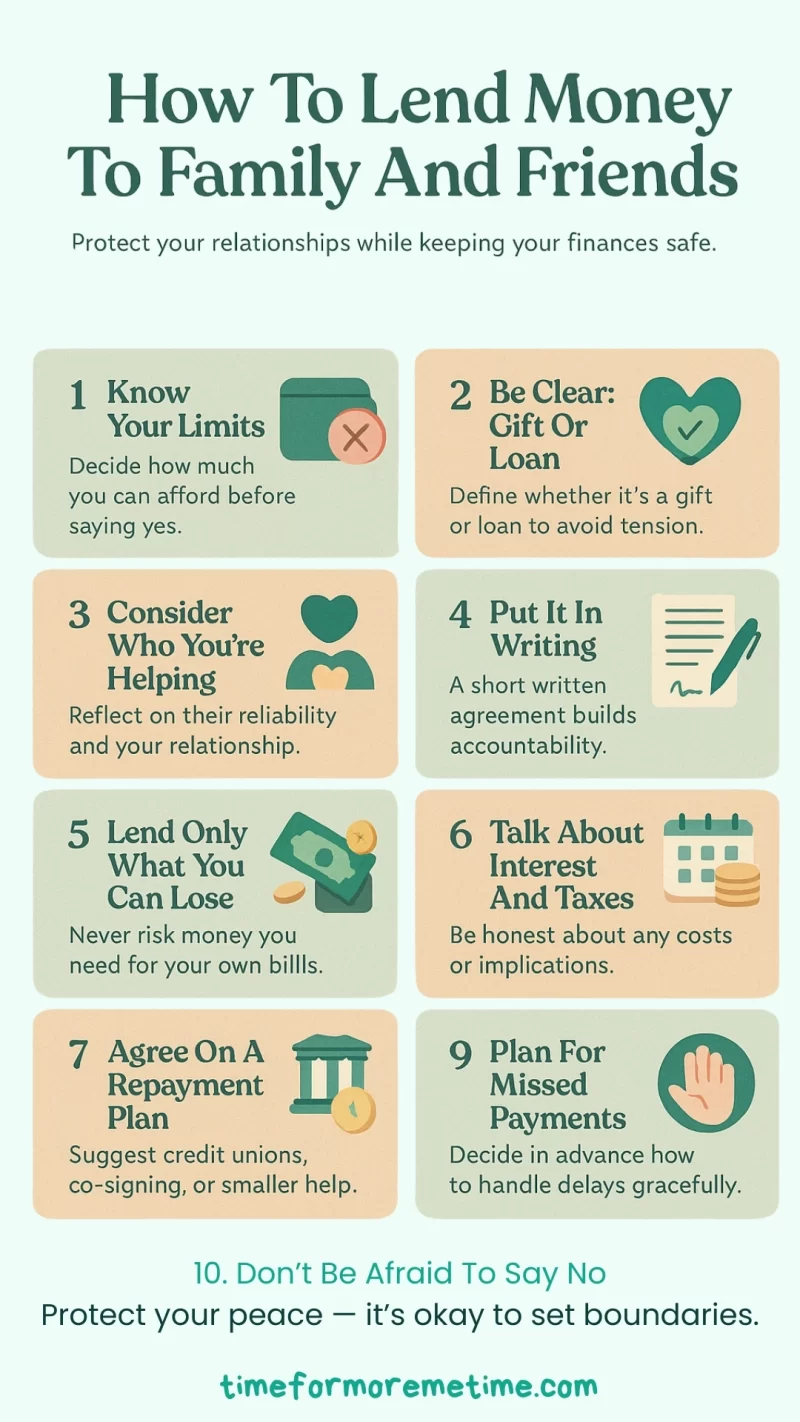

1. Know Your Limits

Before offering help, pause to review your own finances. Lending money should never put your savings, bills, or emergency fund at risk. Ask yourself if you could manage comfortably if the loan is never repaid. Thinking this through helps you avoid resentment later.

When you clearly know what you can afford, you’re more confident in your decision and less likely to feel stressed if repayment doesn’t go as planned.

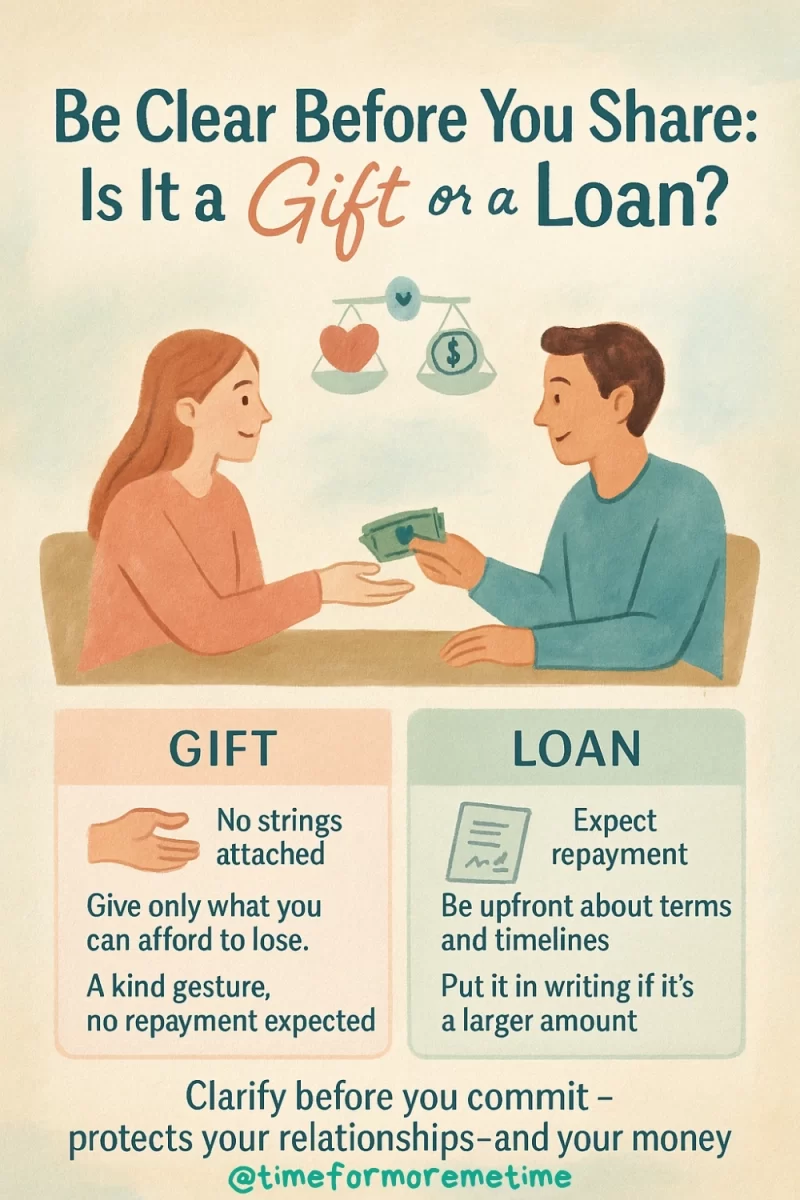

2. Be Clear: Gift Or Loan

Once you know your limits, decide whether the money is a gift or a loan. If you’re comfortable never seeing it again, a gift might make sense and save future conflict. If it’s a loan, be upfront so expectations are clear.

Too often, people assume repayment will happen when it doesn’t. By clarifying your motive early, you protect your relationship from misunderstandings and ensure both sides know exactly what to expect.

3. Consider Who You’re Helping

Next, consider who is requesting the money and why. Is this a one-time emergency or part of a pattern of financial struggles? Consider the borrower’s reliability—have they handled debts responsibly before? This isn’t about judging them harshly but being realistic about the likelihood of repayment.

Considering both the relationship and their track record helps you strike a balance between compassion and caution when deciding how formal or flexible your loan terms should be.

4. Lend Only What You Can Lose

Even when you trust someone, it’s wise to lend only what you can comfortably lose. Setting a limit keeps you financially safe and prevents the loan from harming your own stability. It also reduces tension if repayment is delayed or doesn’t happen at all.

Lending within your means allows you to stay generous without creating resentment. Keeping amounts realistic helps you support loved ones while still protecting your financial well-being.

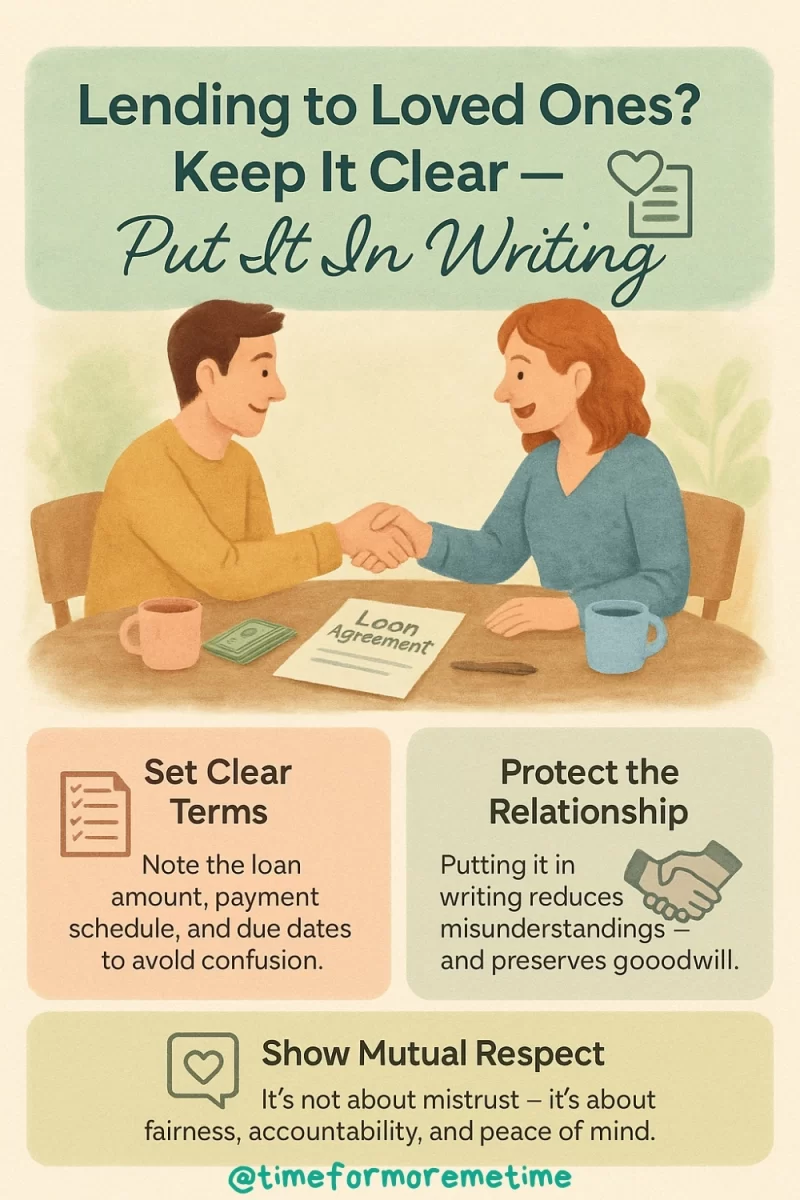

5. Put It In Writing

Handshakes and promises often fade, so it’s best to write down the terms of the loan. Even a simple note that includes the amount, repayment plan, and due dates makes expectations clear and transparent.

A written agreement protects both parties by eliminating uncertainty and preventing future disputes. While it may feel too formal with family or friends, this step demonstrates your commitment to maintaining a strong relationship and ensuring a fair loan.

6. Talk About Interest And Taxes

Money between loved ones can still have financial consequences. Charging interest may feel awkward, but it can sometimes add accountability and fairness. If you do, make sure the rate is reasonable and legal to avoid tax issues. Even interest-free loans can raise IRS questions if they’re large.

Discussing these details upfront helps avoid hidden surprises. Treating the loan with the same care as a bank would keep everyone on the same page.

7. Agree On A Repayment Plan

Once terms are clear, decide on a repayment schedule that works for both of you. Will it be weekly, monthly, or a lump sum? Putting specific dates in place makes it easier to track progress and reduces the chance of awkward reminders.

Checking in regularly creates accountability without nagging. A clear repayment plan also gives the borrower confidence, as they know exactly what’s expected and can budget accordingly.

8. Consider Safer Alternatives

Sometimes saying yes isn’t the best way to help. Instead of a personal loan, you might suggest alternatives such as co-signing, small formal loans through online platforms, or helping them apply for assistance programs. Some apps even let you structure family loans securely, reducing tension.

Exploring alternatives shows you care about their situation while protecting your finances. It can be the middle ground between offering support and maintaining financial and personal independence.

9. Plan For Missed Payments

Even with the best intentions, repayment may not always go smoothly. That’s why it’s important to discuss what happens if a payment is late or missed. Will you extend the timeline, pause the loan, or forgive part of it?

Talking this through before money changes hands helps avoid anger later. Planning for bumps in the road keeps communication open and the relationship intact, even if repayment takes longer than expected.

10. Don’t Be Afraid To Say No

The hardest, yet sometimes wisest, choice is saying no. Lending money you can’t afford—or lending to someone who may not repay—can create bigger problems than it solves. Saying no doesn’t mean you don’t care; it means you’re protecting both your finances and your relationship.

Offering non-financial support, like helping them budget or find resources, can be just as valuable. Knowing when to say no helps you stay generous without risking long-term strain.

Conclusion

Lending money to family and friends doesn’t have to end in stress or broken trust. With clear limits, written terms, and open conversations, you can help loved ones while protecting your own financial security. The goal isn’t just to hand out money but to do it in a way that keeps relationships healthy.

Want more practical guides on handling money wisely? Subscribe to our blog, follow us on social media, and check out our YouTube channel for tips you can use every day.

Sources

- Photo: Pexels: Tima Miroshnichenko