Trying to stick to the family budget is often harder than putting one together. Many households begin with clear intentions, yet daily spending choices gradually undermine the plan. When routines fail to support the budget, maintaining consistency becomes challenging.

That pattern became clear while I was handling household money during a busy time with work and family obligations. The budget was good, but it relied too much on remembering and resisting temptations in the moment. Once I followed some easy steps that worked even on crazy days, the budget finally worked out.

In this post, I’ll show you how to stick to the family budget. Let’s get started!

1. Build A Budget You Can Repeat

A budget only works when it fits into daily life without constant attention. The goal is to have consistency over the weeks. With a working and repeatable budget, you can set clear limits and allow for normal changes.

Most families struggle when a budget needs regular updates to stay accurate. Fixed bills are predictable, while groceries, fuel, and school costs change throughout the month. To avoid losing control, I separate these categories to create flexibility. This approach addresses a concern people often express online: that budgets feel too strict to follow.

To do this, look at how your money moves during a typical week rather than an ideal one. Set ranges instead of exact amounts for flexible categories. Fix amounts for fixed costs. Sticking to it becomes much easier if you make your budget match how you actually live. This naturally leads to tracking spending without burnout.

2. Track Spending Without Burnout

Tracking spending should not be like a second job. The purpose is to stay aware enough to make better choices. Having a simple tracking habit keeps the budget visible without draining energy.

I used to stop tracking because I tried to be too detailed for too long. Writing down every small purchase and checking apps multiple times during my power hour every day becomes tiring quickly. That’s when I found a lighter approach that works better. Now, I do weekly check-ins and daily quick notes. This is usually enough to spot patterns and catch problems early.

Remember, you don’t need both methods and paid finance tips from advisors to track expenses. Choose one method that you can keep up with even during busy weeks. This could be using a notes app, a simple spreadsheet, or a budgeting app you already use.

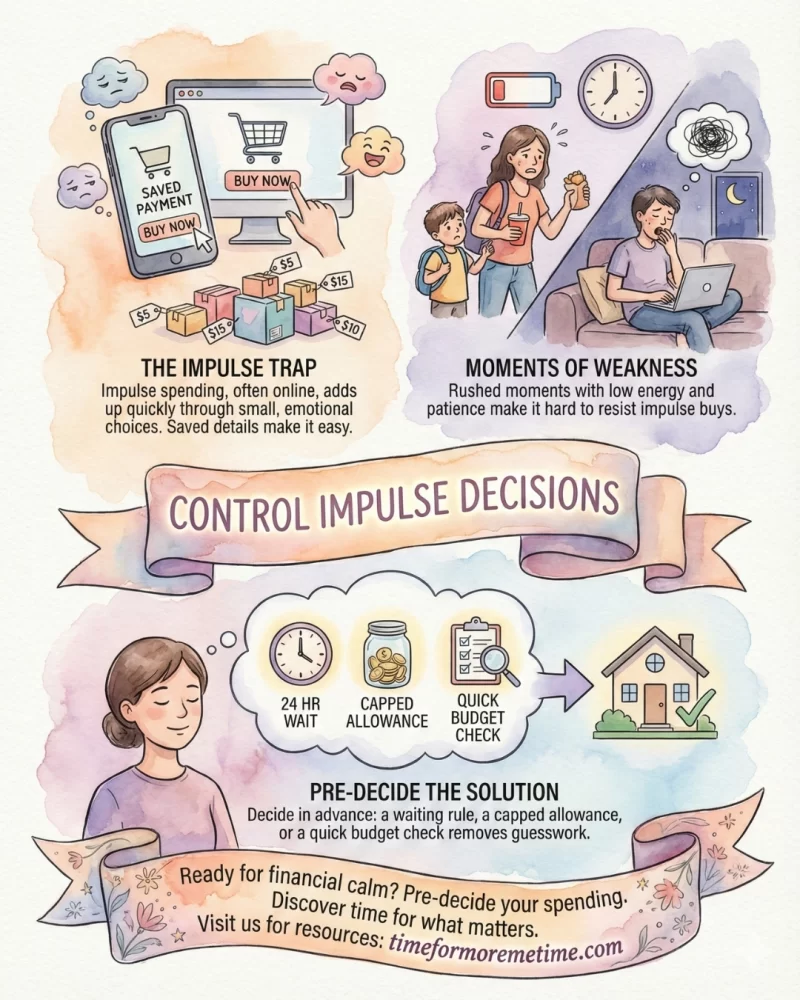

3. Control Impulse Decisions

Impulse spending is one of the fastest ways a family budget gets pushed off course, and it often happens online. In fact, 40% of impulse purchases are made online due to small, emotional decisions that add up quickly. These purchases are rarely large at the moment, but they stack up over a week through quick taps and saved payment details.

Some of my friends, before I became an expert side hustler, spent a lot of money when they were rushed and didn’t take time to think about the sudden expense. This happens after school pickup, while grabbing food between errands, or late at night when the house finally gets quiet. In those moments, energy is low and patience is thin, making it hard to consider expenses and allowing impulse to take control.

The solution lies outside those moments. Decide in advance how to handle unplanned spending, so the decision is already made. A waiting rule, a capped allowance, or a quick budget check removes guesswork.

4. Automate Budget Priorities

Automation keeps a budget working even when attention shifts elsewhere. Automating key decisions allows you to budget without relying on unreliable memory or timing. This is what keeps my progress steady during busy weeks.

I started using automation after experiencing how easily plans slipped once the month began. Bills were handled first, while savings and debt were dealt with at the end. The change created stability without extra effort.

You can easily set up automatic transfers for savings, debt, and fixed bills as soon as income arrives. Leave only what’s needed for daily spending in your checking account. This structure protects the budget quietly and makes it easier to adjust when life changes.

5. Adjust The Budget Without Quitting

A budget works best when it can bend a little. Life changes, expenses shift, and routines don’t always stay neat. Treating the budget as flexible keeps it useful instead of frustrating.

I often see people on social media post about giving up after one off month. Budgeting gets set aside once a repair bill shows up or spending runs higher than expected. What actually helps in those moments is having a simple way to recover instead of starting from scratch.

If you’re like that, you don’t need a full overhaul. You can start with a short review for recovery. Look back at the month, move money where it needs to go, and reset a few limits.

Conclusion

If you want to stick with a family budget, it comes down to how well it fits real life. Clear decisions and regular check-ins do more than motivation ever will, which is what keeps a budget going beyond the first few weeks.

To help you rethink more of how you manage your household budget, read our other posts, follow our socials, and watch our YouTube videos. Moreover, share it with someone who’s trying to stay consistent, and let me know which change you’re starting with.

Source

- Photo: Pexels: Mikhail Nilov