Tax season gets stressful when people think of taxes as a once-a-year issue. Many do not realize how quickly unpaid taxes can add up, especially if their income isn’t from a regular paycheck. This pressure usually hits when deadlines loom, leaving few options.

I dealt with this problem when my income became unpredictable. This was before I became a roofer, graduated from college, and became a dosimetrist. Without steady paychecks, I had to take care of my own taxes. After one tough filing season, I knew I couldn’t wait until April anymore.

In this post, I’ll share how to manage your estimated tax payments in a way that works for you. I’ll explain how I did it. Let’s get started!

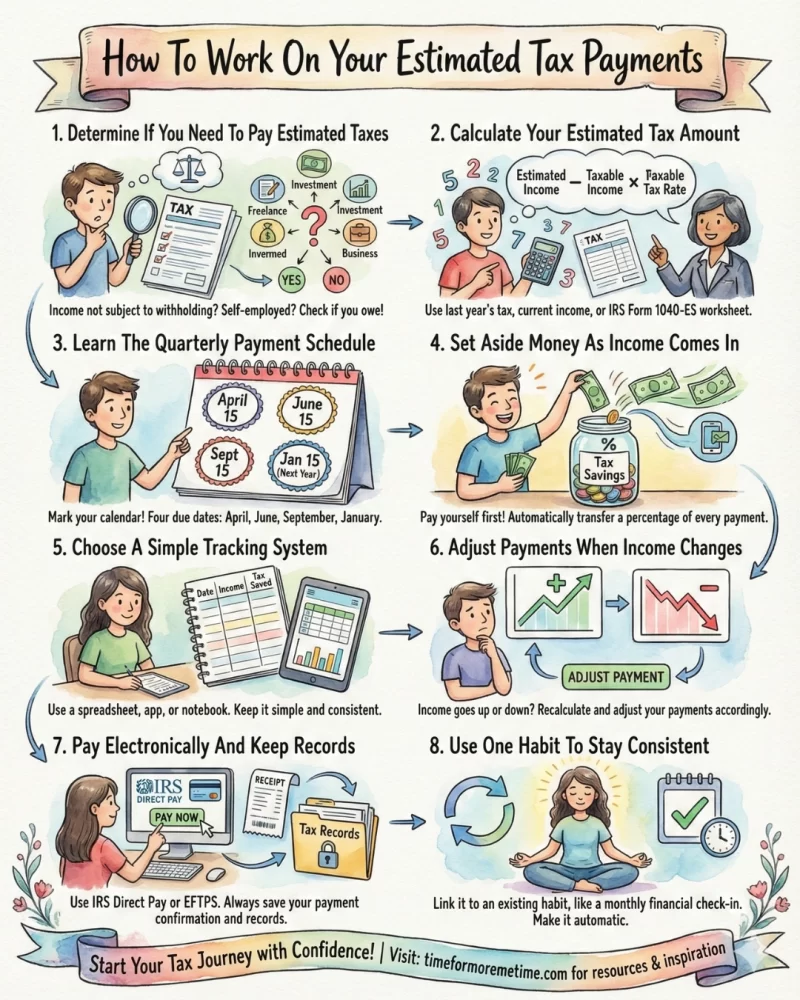

1. Determine If You Need To Pay Estimated Taxes

Estimated tax payments are for people who earn income that isn’t automatically taxed. This includes freelancers, side jobs, investment gains, and certain retirement distributions. I worried about this when I was working as a contractor.

Tax authorities usually say that if you expect to owe a certain amount in taxes, you need to make estimated payments. This rule applies even if your income is uneven or seasonal. Waiting until tax time won’t erase this obligation.

Once you know that you need to make estimated payments, it’s easier to organize the rest of the process.

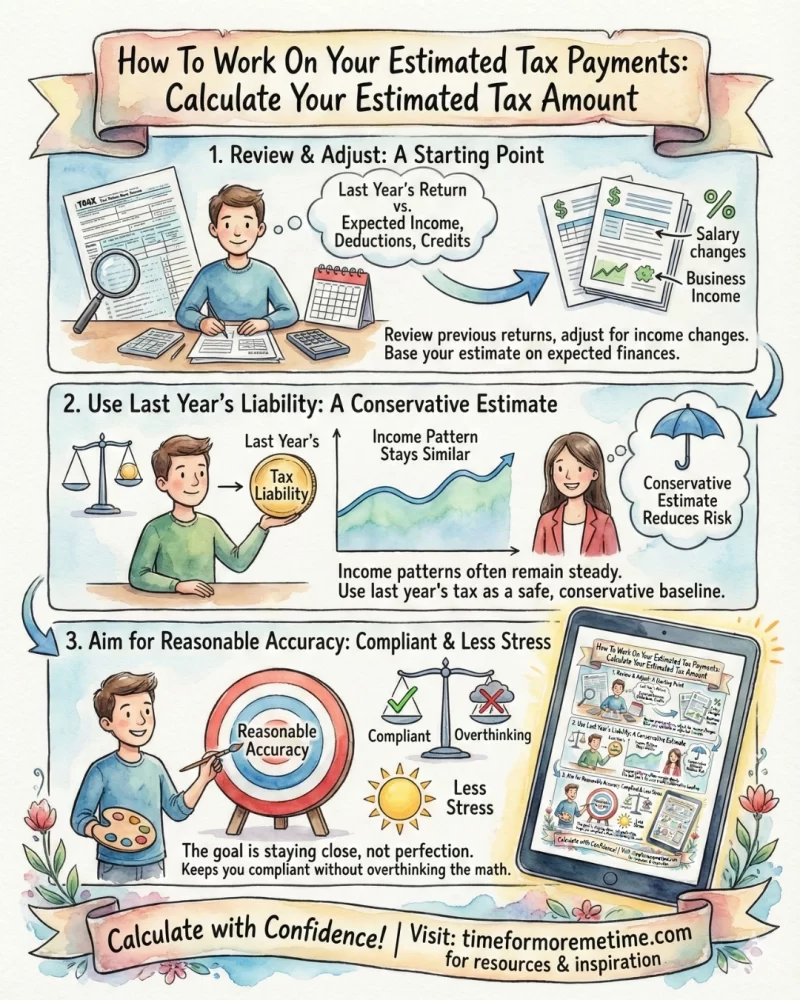

2. Calculate Your Estimated Tax Amount

Your estimated tax amount is based on expected income, deductions, and credits for the year. I began by reviewing my previous tax return and adjusting for income changes.

Many people use last year’s tax liability as a starting point. This works because income patterns often stay within similar ranges. And when you’re estimating conservatively, you’re reducing the risk of underpayment.

The goal is reasonable accuracy. Staying close keeps you compliant without overthinking the math.

3. Learn The Quarterly Payment Schedule

Estimated taxes are typically paid four times a year, meaning payments follow a fixed schedule rather than a monthly rhythm. That schedule includes deadlines in April, June, September, and January. This timing often surprises people—it surprised me before—because it doesn’t match standard calendar quarters.

When one of these dates is overlooked, penalties can apply even if the rest of the year is handled well. That’s why adding these deadlines to your calendar early helps you stay on schedule and avoid unnecessary last-minute stress.

4. Set Aside Money As Income Comes In

Setting aside tax money as income comes in prevents cash flow problems later. This step becomes essential when income fluctuates or arrives irregularly. I noticed this mattered most once income stopped following a predictable paycheck cycle.

Because taxes are owed regardless of timing, separating the money early reduces pressure. Many people find that keeping tax funds in a dedicated account creates a clear boundary between what can be spent and what is already committed. When payment deadlines arrive, the funds are available without scrambling.

This habit works best when it’s tied directly to receiving income. Each deposit triggers a small transfer to your tax set-aside account. Over time, this turns tax saving into a routine rather than a decision you have to revisit each month.

5. Choose A Simple Tracking System

A simple tracking system helps keep your estimated tax payments organized and visible. This way, you’ll be reminded to pay your taxes without confusion later. I found that tracking often fails when the system is too complicated.

Basic tools work best because they are easy to use. A spreadsheet, budgeting app, or simple notes can help you track income, set-aside amounts, and payment dates. Keeping everything in one place makes it easier to see patterns and catch problems early.

You’ll be more consistent if tracking fits naturally into your routine. Update your records during your regular financial check-ins. This keeps the system active and makes estimated taxes feel like a normal part of managing your money, not an extra burden.

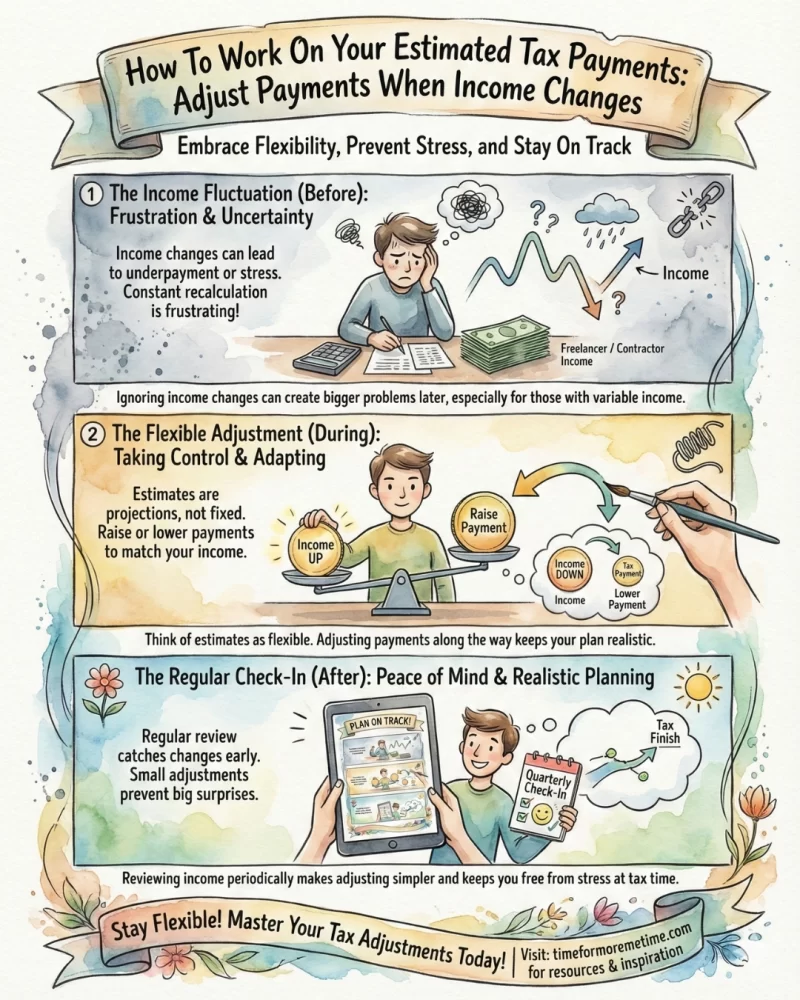

6. Adjust Payments When Income Changes

Your income can change throughout the year, which affects how much tax you owe. Ignoring these changes can lead to underpayment or extra stress later. This is especially true for freelancers and contractors. When I was moving from job to job, it was frustrating to keep calculating what taxes I owed, even with a tracker.

Since estimated taxes are based on projections, it’s okay to make adjustments. If your income goes up or down, you can raise or lower your payment amounts to stay on track. Thinking of estimates as flexible rather than fixed makes the system easier to manage.

Regular check-ins make adjusting payments simpler. Reviewing your income at certain times during the year helps you catch changes early. Making small adjustments along the way prevents bigger problems at tax time and keeps your plan realistic.

7. Pay Electronically And Keep Records

Paying your taxes electronically makes managing estimated payments much easier. It reduces delays and gives you immediate confirmation, removing uncertainty about whether your payment went through. Plus, it’s simply more convenient.

Keeping records is just as important as making payments. Tracking dates, amounts, and confirmations helps when you need to check totals later. Without records, tax season can become slow and frustrating.

A simple system is best for records. Saving confirmations in a dedicated digital folder makes everything easy to find. When your records are organized throughout the year, filing your taxes becomes a straightforward task instead of a major challenge.

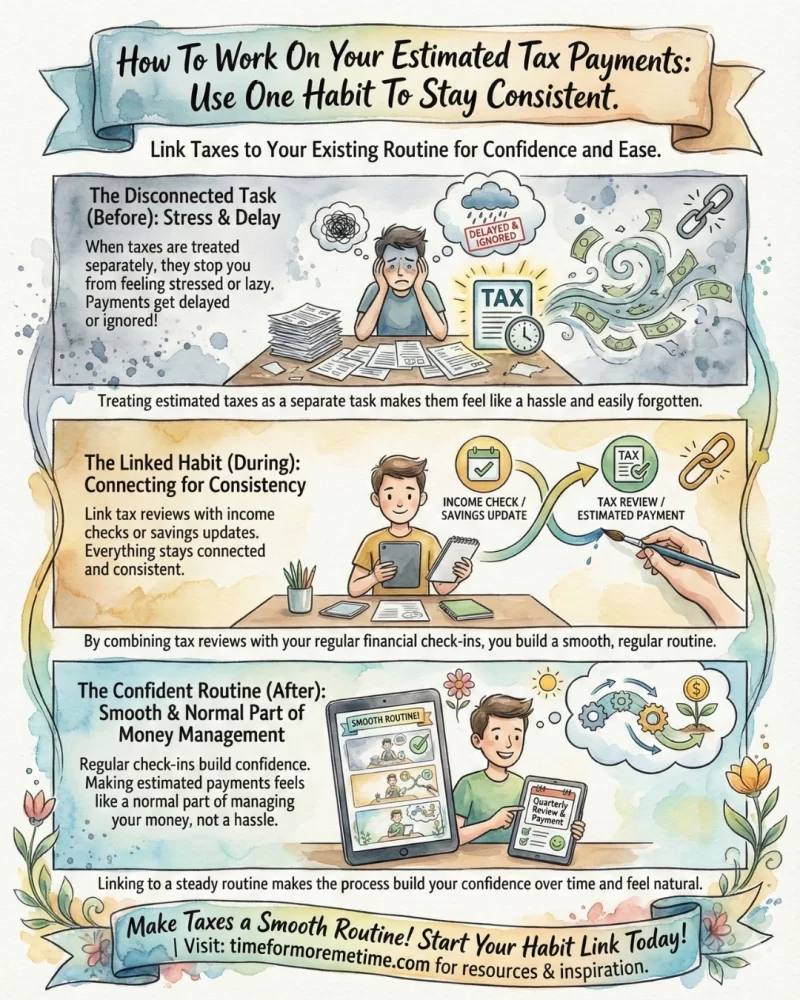

8. Use One Habit To Stay Consistent

Estimated tax payments are easier when you link them to a habit you already have. When taxes aren’t seen as a separate task consistently, it stops you from feeling stressed or lazy about making payments.

Many people check their finances regularly. By combining tax reviews with income checks or savings updates, everything stays connected. When taxes are treated separately, they often get delayed or ignored.

Linking estimated taxes to a steady routine helps things run smoothly. Whether it’s monthly budgeting or quarterly reviews, being regular builds your confidence. Over time, making estimated payments feels like a normal part of managing your money instead of a hassle.

Conclusion

Working on your estimated tax payments becomes easier when you treat them as an ongoing habit rather than a seasonal task. Simple planning, regular reviews, and realistic systems keep payments manageable throughout the year.

For more practical money strategies like this, read our latest posts, follow us on social media, and visit our YouTube channel for clear guidance you can apply right away.

Source

- Photo: Pexels: Nataliya Vaitkevich