Most people underestimate how much income they actually need to cover basic needs in today’s economy. Knowing the true minimum—your cost of survival—is essential to planning for financial security. In this post, I’ll explain the difference between minimum, living, and comfortable wages—and show you how to calculate a baseline for your situation. Let’s get started!

Survival Income Benchmarks In The US

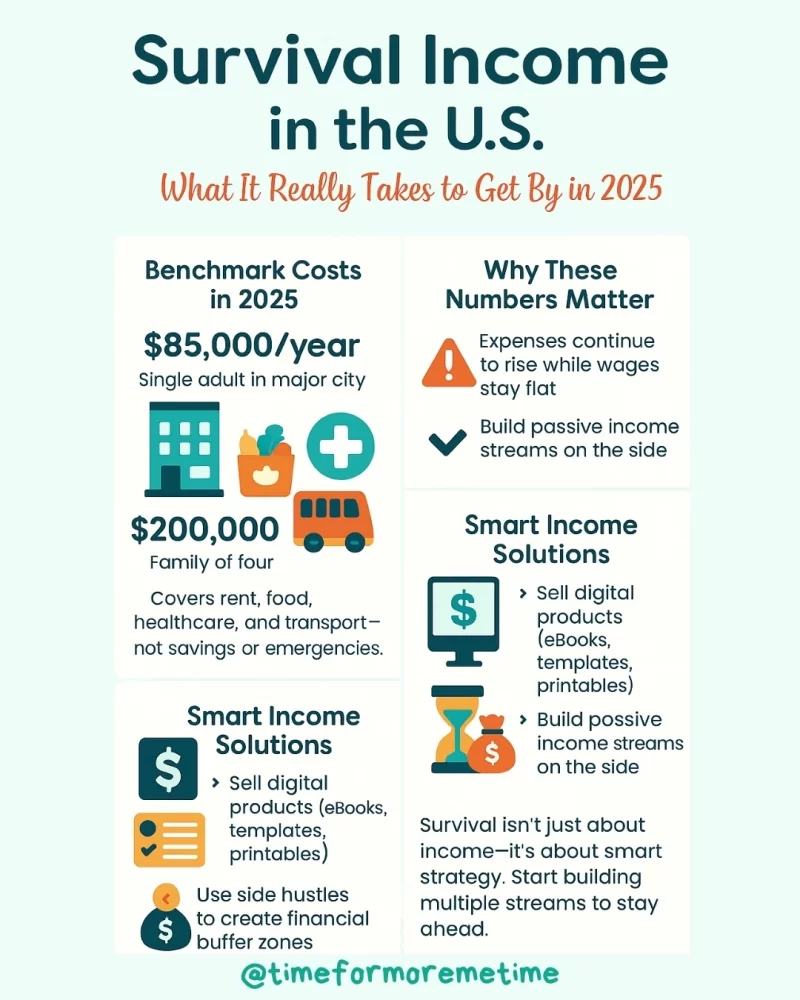

In 2025, the survival income for a single adult in a major U.S. city will have reached approximately $85,000 per year, while a family of four will need nearly $200,000 annually to cover necessities like rent, food, healthcare, and transportation. These numbers reflect the minimum required to survive—without accounting for savings, debt, or emergencies.

As basic living costs rise, many Americans are exploring supplemental income sources. Selling digital products—like templates, printables, or eBooks—has become a popular option due to low overhead and flexible hours. Creating small streams of passive income alongside a primary job can ease the pressure of meeting survival-level expenses and provide a buffer for future needs.

Global Survival Income Estimates

Survival income needs vary widely across the globe, but the pattern is clear—basic costs are rising everywhere. According to the Anker Methodology, survival-level wages must cover essentials like food, housing, healthcare, and transportation.

In the UK, an adult needs at least £28,000 per year, while families in London require over £47,000 to meet minimal living standards. In Australia, nearly half of young Australians have less than $1,000 saved despite rising living costs.

In response, some are turning to passive income sources like rentals or online sales to close the survival gap. These efforts provide much-needed flexibility and financial breathing room.

Reality Of Minimum Wage Vs. Survival Needs

The federal minimum wage in the U.S. remains at $7.25 per hour, a rate unchanged since 2009. Yet in most cities, this is far from enough to cover even the most basic survival needs. For example, a single adult in California needs at least $19.41 per hour, while a family of four requires $27.42 per hour to get by.

This gap forces many low-income earners to rely on multiple jobs, public assistance, or high-interest credit—leaving little room for planning or security. Without access to savings, affordable housing, or basic financial instruments like low-risk investments or employer-sponsored benefits, surviving on minimum wage becomes a constant financial balancing act.

Emergency Fund As Survival Buffer

An emergency fund is a critical buffer that helps you survive financial shocks—like medical bills, car repairs, or sudden job loss—without falling into debt. The average U.S. household should aim for an emergency fund of at least $35,000, which covers roughly six months of essential expenses.

Building this fund is a priority before investing money elsewhere. While stocks and other investments offer long-term growth, your emergency savings must be easily accessible and low-risk.

Think of it as your financial safety net—the foundation that keeps you stable when life throws you a curveball. Without it, even minor disruptions can push you below the survival line and make it difficult to recover.

How To Calculate Your Personal Survival Number

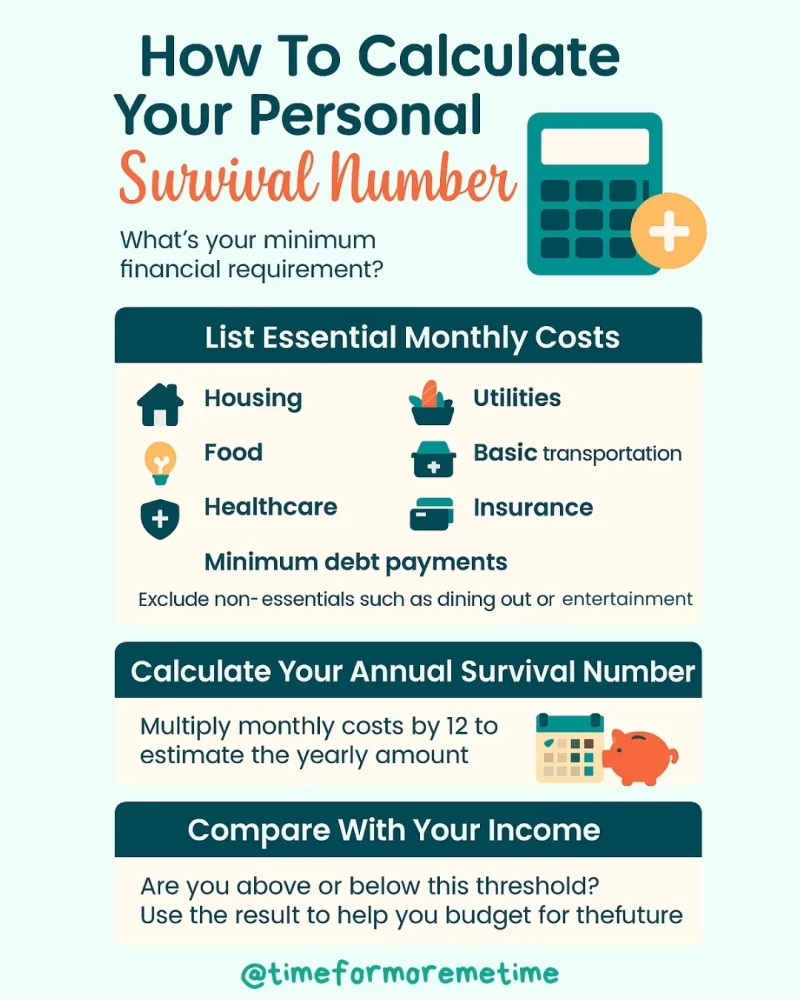

Everyone’s survival number is different, depending on where you live, how many people are in your household, and your essential monthly costs. To calculate yours, start by listing your absolute necessities:

- Housing

- Utilities

- Food

- Basic transportation

- Healthcare

- Insurance

- Minimum debt payments

Leave out non-essentials like dining out, subscriptions, entertainment, or savings goals—this is about what it takes to survive, not thrive.

Add up the monthly cost of these essentials, then multiply by 12 to get your annual survival number. If you’re unsure of local benchmarks, use free tools like an online living wage calculator for a regional baseline.

Next, compare this number to your actual income. Are you above or below your survival threshold? If you’re below, it may be time to reassess your spending or explore ways to increase revenue—whether through side jobs, benefit programs, or cutting fixed costs.

This survival number also gives you a target for emergency savings and helps inform future goals like budgeting, career planning, or even investing money after your basics are covered. Knowing your minimum financial requirement gives you more control, clarity, and motivation to build a more secure future.

Conclusion

Knowing your survival number gives you clarity and control. It helps you focus on what really matters—covering your essentials and building a stable foundation.

If you found this post helpful, subscribe to our blog, follow us on social media, and check out our YouTube channel.

Source

- Photo: Pexels: Kaboompics.com