Cutting back on daily expenses might seem overwhelming, especially with rising prices on everything from food to utilities. However, with a few simple adjustments, you can take control of your spending without compromising your lifestyle. In this post, I’ll walk you through practical strategies to help you minimize daily expenses and build smarter financial habits—starting today. Let’s get started!

1. Track And Analyze Spending

The first step to minimizing daily expenses is knowing exactly where your money goes. Track every purchase—no matter how small—for at least a week. Use a simple notebook, spreadsheet, or budgeting app to record your spending habits. Look for patterns, such as frequent takeout or unused subscriptions, that quietly drain your funds.

Many banks now offer built-in expense tracking tools through their mobile apps, making it easier to categorize spending and set alerts. Reviewing your transactions regularly helps you make more informed choices and identify areas where you can reduce expenses without major lifestyle changes.

By staying aware of your spending, you’ll take the first step toward establishing a more sustainable and budget-friendly routine.

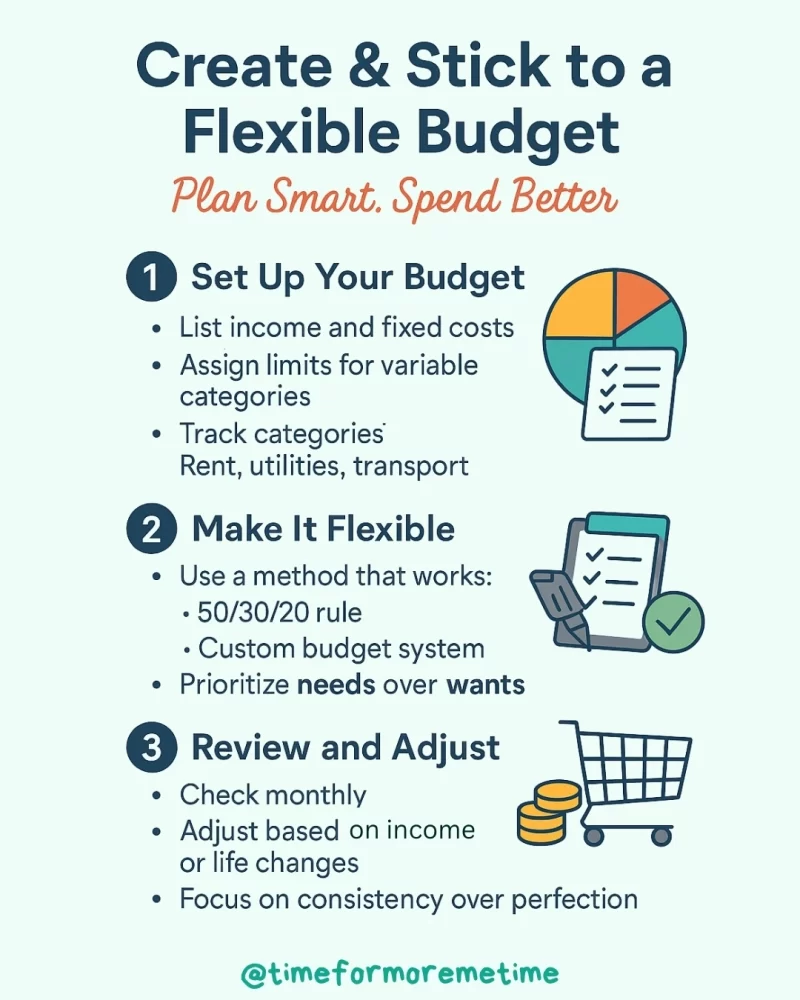

2. Create And Stick To A Flexible Budget

Once you understand your spending habits, it’s time to set a realistic budget that fits your lifestyle. Start by listing your monthly income and fixed expenses like rent, utilities, and transportation. Then assign limits to variable categories such as food, entertainment, and shopping.

The key is to stay flexible. A budget isn’t meant to restrict you—it’s meant to guide you. Choose a method that works for you, whether it’s the 50/30/20 rule or a custom plan. For those focused on frugal living, budgeting helps prioritize needs over wants and avoid impulse spending.

Adjust your budget monthly based on changes in income or expenses. Consistency is more important than perfection, and even small improvements can lead to big savings over time.

3. Automate Essentials And Savings

Automation makes it easier to stay on track with your financial goals. Start by setting up automatic payments for fixed expenses, such as rent, utilities, and subscriptions, to avoid late fees and missed due dates. Most banks allow you to schedule payments directly from your account.

Next, automate your savings. Set up recurring transfers from your checking to your savings account—even small amounts add up over time. This “pay yourself first” approach helps you build a safety net without thinking about it. You can also automate contributions to retirement funds or investment accounts.

By automating essentials and savings, you remove the guesswork, reduce stress, and make progress toward your goals with minimal effort. It’s a straightforward way to establish consistency in your finances.

4. Cut Unnecessary Recurring Costs

Recurring costs can quietly drain your budget if left unchecked. These include monthly subscriptions, app memberships, streaming services, and automatic renewals that often go unnoticed. Review your bank and credit card statements to identify services you rarely use or forgot you signed up for.

Canceling even just two or three subscriptions can lead to significant savings over time. This step is one of the most practical saving money tips because it reduces spending without changing your daily habits. You can also consider switching to free or shared alternatives where possible.

Regularly auditing your recurring charges ensures you’re only paying for what you truly use, helping you keep more of your money where it belongs.

5. Manage Fixed Expenses

Fixed expenses like rent, utilities, insurance, and loan payments take up a large part of your budget—but that doesn’t mean they can’t be adjusted. Begin by reviewing each major bill to identify areas where you can reduce costs. Can you negotiate your internet or phone plan? Are there cheaper providers for insurance or energy?

If you’re renting, consider downsizing, getting a roommate, or moving to a more affordable location. Refinancing loans or consolidating debt may also help lower your monthly payments. For those with investments, rebalancing away from high-risk assets to fixed-income mutual funds can provide greater stability during periods of market volatility.

Managing fixed expenses is a smart move if you’re aiming for long-term financial control and daily savings.

Conclusion

Minimizing daily expenses doesn’t require extreme sacrifice—it just takes intention, consistency, and a few smart changes. Start with one habit, build on it, and stay flexible as your needs change. The goal isn’t perfection—it’s progress. Over time, these simple choices can lead to stronger financial habits and a greater sense of control over your money.

Ready to take the next step? Subscribe to our blog, follow us on social media, and check out our YouTube channel for more helpful guides.

Source

- Photo: Unsplash: Mike Cho