Living on one income means every dollar already has a job before it even arrives, especially in a single-income family facing rising prices. According to data, many US households struggle to cover a few hundred dollars in an unexpected expense. That pressure is real, and it pushes families to make harder choices faster.

I have managed a household where one paycheck covered rent, groceries, and insurance. Years ago, in a small Buffalo apartment, I wrote every expense in a notebook to keep the month from slipping out of control. That habit led me to study budgeting systems, spending patterns, and income planning that hold up under real pressure. Those lessons shaped how I approach financial stability today.

In this post, I’ll walk you through clear ways to make one income stream work better based on my experience, where each section focuses on actions you can use right away. Let’s get started!

1. Build A Stable Budget

A stable budget gives a single-income household a clear operating plan. It assigns income to fixed bills, flexible spending, and future goals before money starts moving. I adopted this approach after realizing that reacting to expenses created more stress than the expenses themselves.

That reaction-based pattern is common across US households. Federal Reserve data shows that US families often struggle to cover a $400 unexpected expense without borrowing. When income has no assigned direction, even small surprises can knock an entire month off balance.

Think about how your paycheck enters your household. If decisions happen only when bills arrive, pressure builds quickly. A stable budget removes that friction by setting priorities in advance to manage household finances. This structure serves as the basis for controlling costs and planning ahead.

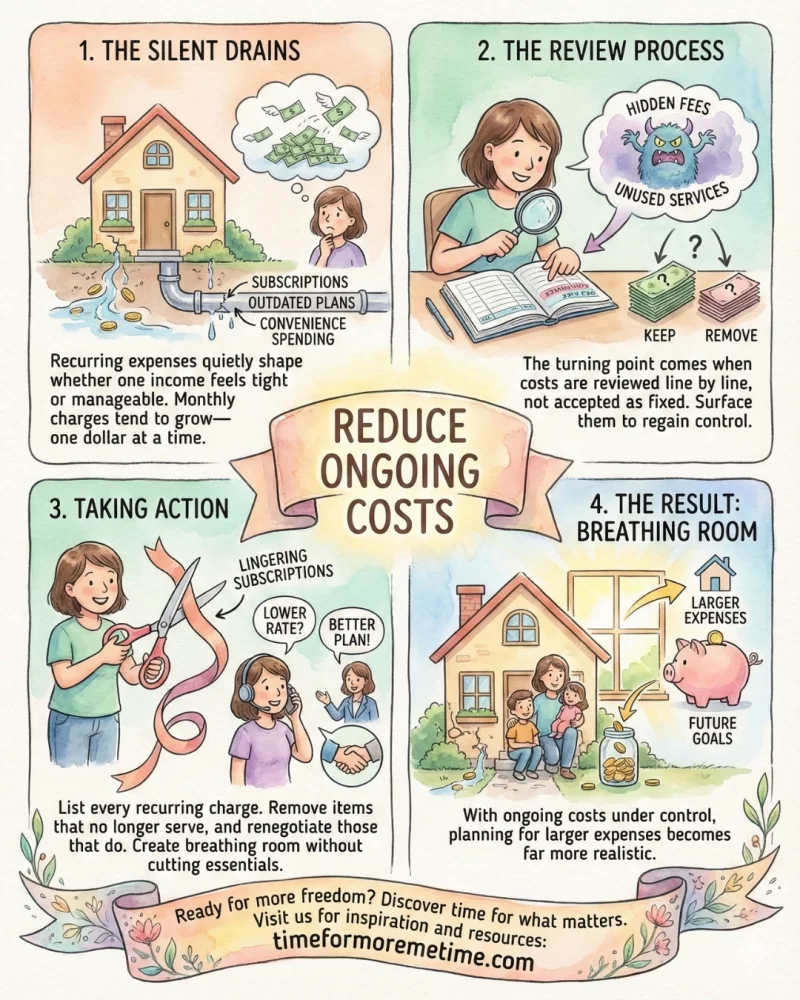

2. Reduce Ongoing Costs

Recurring expenses quietly shape whether one income feels tight or manageable. Monthly charges tend to grow in the background—one US dollar at a time—often without a clear decision attached to them. The turning point usually comes when those costs are reviewed line by line instead of accepted as fixed.

I have seen this pattern repeatedly in messages from readers who track their spending for the first time. Subscriptions linger, insurance plans stay outdated, and convenience spending fills the gaps between paychecks. Once these costs are surfaced, control returns faster than expected.

So, start listing every recurring charge tied to your household. Remove items that no longer serve your priorities, and renegotiate those that do. This process creates breathing room without cutting essentials. With ongoing costs under control, planning for larger expenses becomes far more realistic.

3. Plan Major Expenses

Large expenses can hurt a budget when they come out of nowhere. With only one income, costs like school fees, medical bills, or home repairs can wreck months of planning in an instant. By planning ahead, we can change these surprises into planned choices.

I learned this lesson when a medical bill arrived during a tight month. The bill wasn’t huge, but the timing was bad. Since then, I include big, expected expenses in my budget so they don’t catch me off guard.

Look ahead at the next six to nine months in your home. Identify any expenses you know will come, even if you’re unsure of the exact amounts. Set aside money little by little so the impact is easier to handle. Budgeting day-to-day is much easier when you expect major costs.

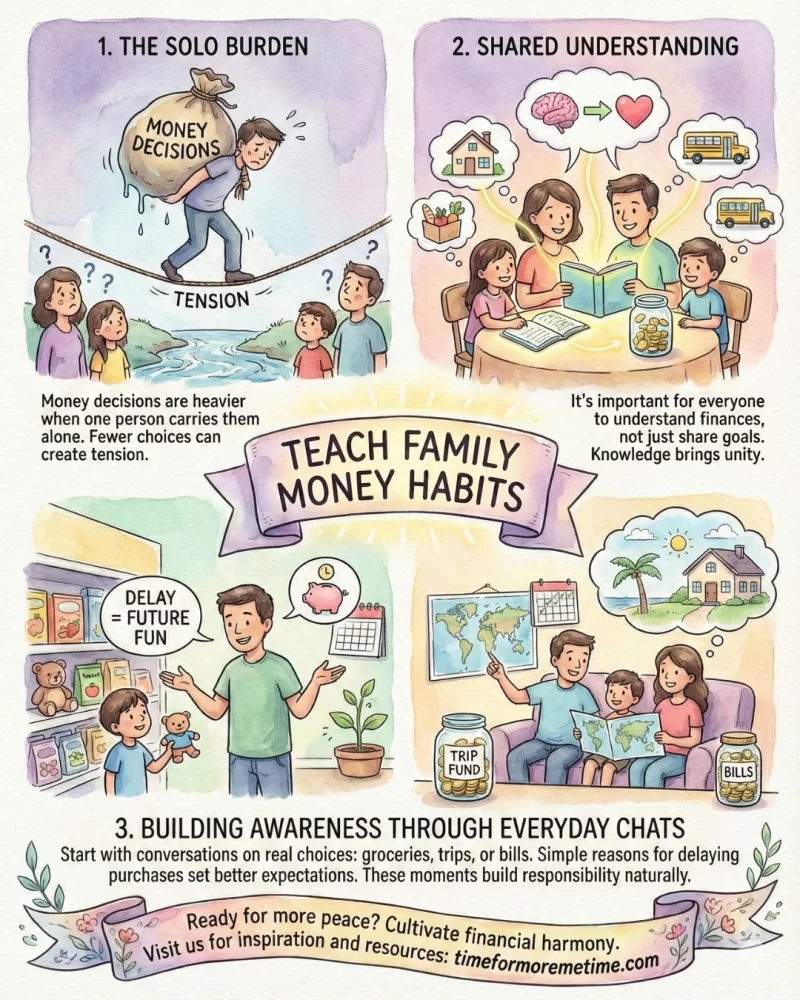

4. Teach Family Money Habits

Money decisions are heavier when one person has to make them alone. In a single-income household, it’s important for everyone to understand finances, not just share goals. Fewer choices can create tension if everyone doesn’t know how money works at home.

Include your family in small talks about spending and saving. Simple reasons for delaying certain purchases can help set better expectations. Over time, these chats will lower stress.

Start with conversations that relate to real choices. Discuss grocery shopping, saving for trips, or planning for bills. These moments help build awareness and responsibility naturally.

5. Add Income Strategically

Extra income is most helpful when it fits into a stable plan for spending and saving. Chasing money without a clear strategy can bring stress. To avoid overwhelming my household, I focus on making what works even better.

I often see people start side jobs to increase income because they’re short on cash. Some options are helpful, but others take up time and energy without improving income. The key is whether they match your existing routines and skills.

It’s smarter to find income ideas that fill a specific need instead of chasing every opportunity. For example, selling things you don’t use, doing flexible freelance work, or making money from a skill you already have keeps your efforts focused.

Conclusion

Living well on one income comes down to structure, timing, and shared understanding. If you have a clear budget, controlled recurring costs, planned expenses, family involvement, and thoughtful income choices, you can reduce pressure and create stability.

Want more tips to manage your finances? Subscribe to the blog and follow along on social media for more practical posts like this, or watch our YouTube videos. Thanks!

Source

- Photo: Pexels:

Yan Krukau