Retirement marks a new chapter in life—one that offers more freedom, but also introduces new challenges. While some dream of travel and relaxation, others are concerned about money, health, and how to spend their time meaningfully. If you’re wondering what life will really look like after leaving the workforce, this post breaks it all down. Let’s get started!

Mandatory Daily Rhythm Changes

One of the biggest shifts in retirement is the loss of daily structure. Without a job anchoring your schedule, you may struggle to find purpose or routine. So, change your daily rhythm.

Create a new rhythm by planning morning walks, weekly errands, or time blocks for hobbies. Use productivity tips like batching errands or setting a simple morning routine to bring structure to your day. This helps prevent boredom and keeps you mentally and physically active.

Sudden Adjustments

Retirement often brings more free time and less daily stress, but it can also lead to unexpected feelings of isolation or a loss of purpose, especially during the first year. Without the structure and interaction that work provides, some retirees find it difficult to stay emotionally balanced.

One way to ease this transition is by staying socially connected. Join local clubs, attend community events, or participate in online groups that match your interests. Creating regular social appointments on your calendar not only helps you stay engaged but also serves as a simple time management tool that supports your well-being.

In addition to staying connected, consider light side work such as tutoring, selling crafts, or teaching a skill online. These flexible options can bring in extra income while adding structure and purpose to your routine.

Just like part-time work gives your week more rhythm, setting personal goals can help fill unstructured time with meaning. Try walking 20 minutes three times a week or reading one book a month—simple goals that give your days direction and create a sense of accomplishment.

Pair these with journaling to reflect on your progress, stay motivated, and maintain emotional balance over time.

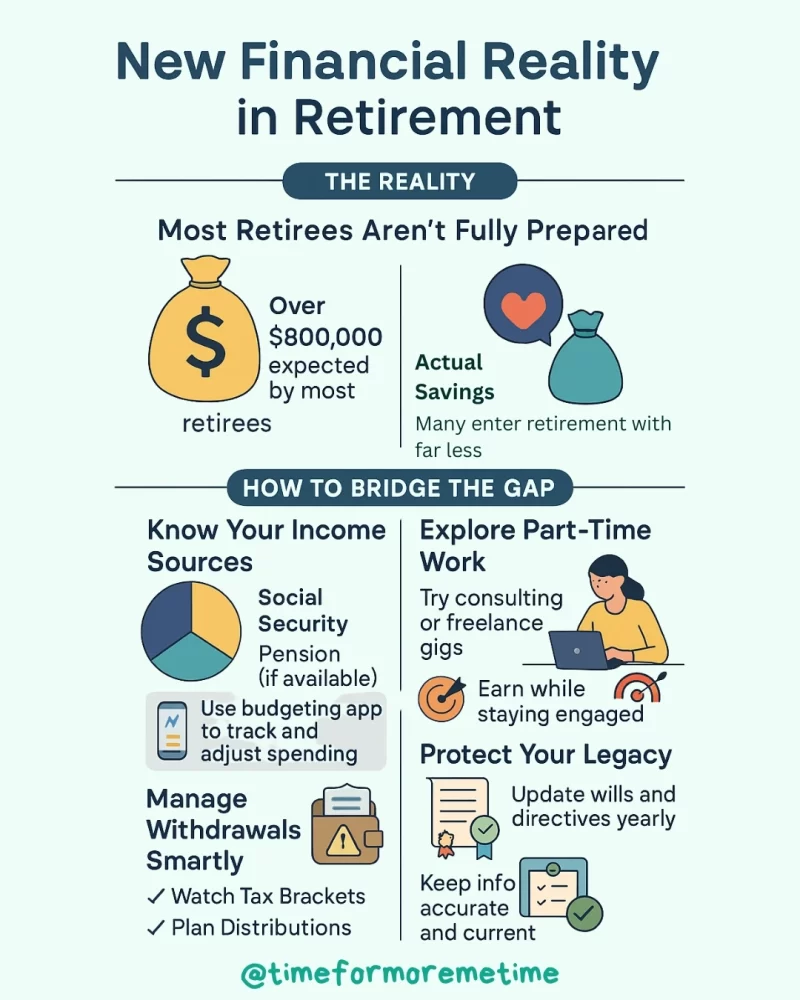

New Financial Reality

Achieving a comfortable retirement requires careful planning, yet many Americans are underprepared. While most anticipate needing over $800,000 for retirement, many enter this phase with significantly less saved.

To bridge this gap, start by identifying your income sources, which typically include Social Security, pension plans, and personal savings or investments. Once you have a clear picture of your income, consider using budgeting apps to monitor spending and make real-time adjustments.

If your projected income falls short, explore part-time work or consulting in your field. These options can provide financial support while offering a sense of purpose.

Retirement planning continues even after paychecks stop; it simply shifts focus. Your withdrawal strategy is crucial—taking out too much at once can push you into a higher tax bracket or incur penalties, especially from tax-deferred accounts like IRAs.

Regularly review your withdrawal strategy and consider working with financial advisors to coordinate income streams and minimize taxes. Additionally, revisit your estate plan annually to ensure your assets are protected and your wishes are clear. Keep beneficiary information, wills, and healthcare directives up to date to maintain your legacy.

Evolved Market Conditions

Markets are unpredictable, and retirement doesn’t protect you from economic shifts. While rising interest rates may benefit your savings account, inflation can quickly reduce your purchasing power.

That’s why it’s important to diversify your assets and strike a balance between growth and financial security. Combining different investment types—like mutual funds, annuities, or dividend-paying stocks—can help you create a more stable income stream over time.

To make informed choices, consider working with financial advisors. They can help you manage market risk, adjust your portfolio when needed, and keep your long-term goals on track.

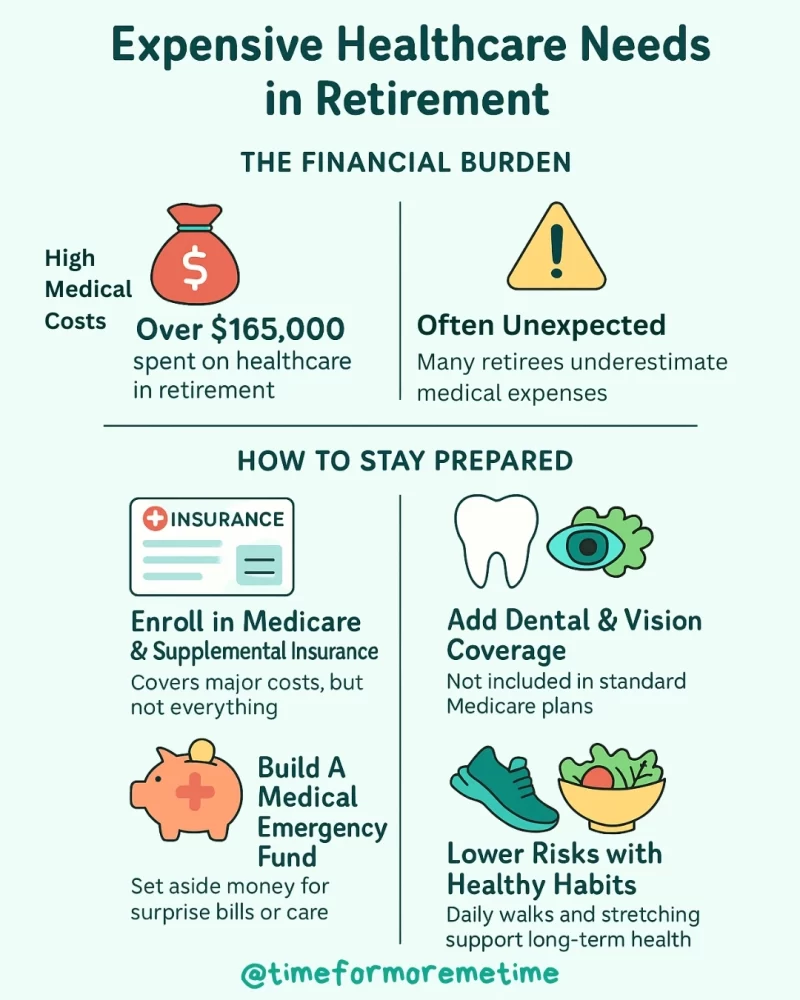

Expensive Healthcare Needs

Healthcare expenses can take up a large portion of your retirement budget. On average, retirees spend over $165,000 on medical care throughout retirement—a cost that often catches people off guard.

Start by enrolling in Medicare and exploring supplemental insurance to help cover out-of-pocket expenses. Don’t forget to include dental and vision care, which aren’t always part of standard plans.

To stay financially prepared, maintain a dedicated savings account for unexpected medical bills or long-term care needs. At the same time, adopting simple healthy habits—like daily walks or regular stretching—can lower your risk of illness and reduce overall costs in the long run.

Conclusion

Retirement is more than a finish line—it’s a lifestyle shift that affects your time, money, relationships, and sense of purpose. By understanding the realities of this transition, you can prepare better and enjoy the life you’ve worked hard to build.

For more tips on living well after work, subscribe to our newsletter, follow us on social media, and watch our videos on YouTube.

Source

- Photo: Unsplash: Kahar Erbol