Managing daily expenses can be tough, especially with prices constantly rising. If you often wonder where your money goes by the end of the day, you’re not alone. The good news is, a few simple strategies can help you take control. In this post, I’ll share practical tips to help you manage your income, set daily spending limits, and build a budget you can actually stick to. Let’s get started!

1. Understand Your Income And Daily Spending

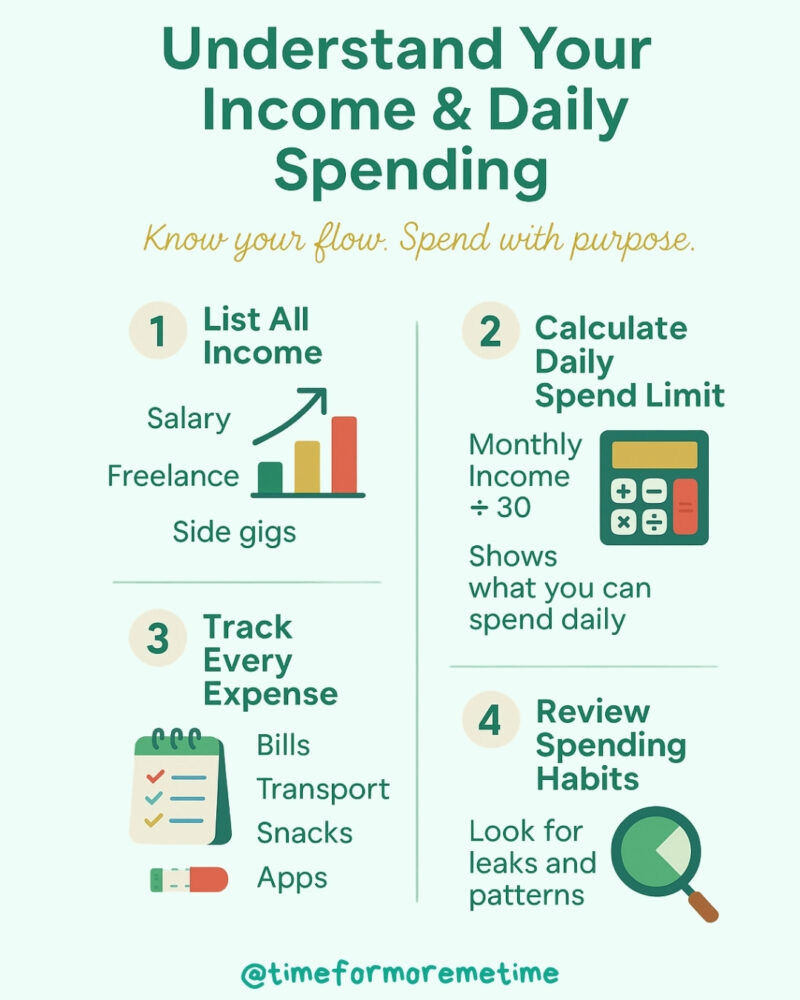

One of the first steps in learning how to manage daily budget is knowing exactly how much money you earn and where it goes. Start by listing all your income sources—this includes your main paycheck, freelance work, or any side gigs.

Then calculate your daily spending capacity by dividing your total monthly income by 30. This gives you a rough idea of how much you can afford to spend each day without going over budget.

Next, track your personal expenses for at least a week. Log every transaction, from bills and transportation to snacks and subscriptions. This step helps reveal spending patterns and small leaks you may be overlooking.

Whether you use a notebook, spreadsheet, or budgeting tools, the goal is the same: understand your daily cash flow so you can make smarter, more intentional choices with your money.

2. Choose A Budgeting Method That Fits You

Not all budgeting methods work equally well for everyone, so it’s essential to choose one that aligns with your habits and goals. Here are some of them:

- 50/30/20 Rule: Ideal for those seeking straightforward guidelines—50% of your income goes to needs, 30% to wants, and 20% to savings or debt repayment.

- Zero-based Budgeting: For those who want more structure, assign every dollar a purpose, helping you stay fully in control of your spending.

- Envelope or Cash-Stuffing Method: This technique involves dividing your money into categories using physical envelopes or digital budgeting tools. This is especially helpful if you’re focused on frugal living, as it limits overspending and builds discipline.

Try different methods and adjust until you find one that fits your lifestyle and income.

3. Set And Allocate Daily Spending Limits

Once you know your monthly income and chosen budget method, the next step is to break it down into manageable daily amounts. Start by dividing your monthly income by 30 to get a rough daily budget.

Then, assign spending limits to categories such as food, transportation, and personal needs. For example, you might set aside $10 per day for meals or $5 for transport.

A helpful rule of thumb is to allocate about 50–60% of your budget to needs, 20–30% to wants, and 10–20% to savings or debt payments. Rounding your limits to simple amounts makes them easier to follow.

Or also consider one of the best saving money tips, where you spend below your daily limit and put the extra into a savings jar or account. Small adjustments like these help you build better habits without feeling restricted.

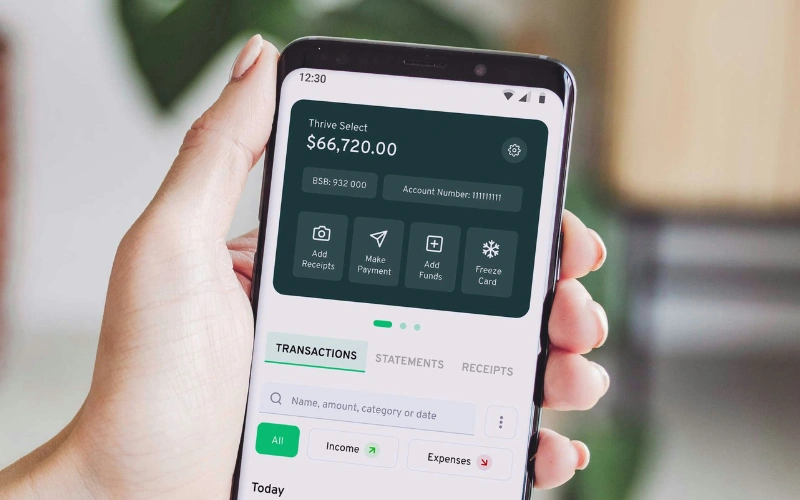

4. Use Tools And Apps To Automate and Track

Staying on top of your daily budget is easier when you utilize digital tools to automate the process for you. Budgeting apps help you track spending in real-time, set limits for each category, and receive alerts before you overspend. Many budgeting tools also sync with your bank accounts, so your expenses update automatically.

Automation takes the stress out of managing money. You can schedule bill payments, set recurring transfers to savings, and receive notifications when you’re close to reaching your limit.

Some banking apps also offer built-in expense trackers and spending summaries. Using the right tools helps you stay organized, reduce effort, and stick to your budget without constantly checking every transaction.

5. Adjust Budget During Price Fluctuations

Prices change, and your budget should adjust with them. When the cost of essentials like groceries, gas, or utilities increases, review your daily spending plan and adjust your limits as needed. If grocery prices rise, for example, consider saving on groceries by doing the following:

- Planning meals

- Buying in bulk

- Switching to store brands

Learning how to manage daily budget becomes especially important during periods of inflation or unexpected expenses. Revisit your non-essential spending and reduce what isn’t urgent. Cancel or pause subscriptions, delay major purchases, or find more affordable alternatives to high-cost items.

Adjusting your budget doesn’t mean giving things up—it means prioritizing what matters most. A flexible mindset helps you stay in control, even when prices shift unexpectedly.

Conclusion

Managing your daily budget is one of the simplest ways to stay in control of your finances, even when prices are unpredictable. With a few daily habits and the right tools, you can reduce unnecessary spending and stay aligned with your goals without feeling restricted.

Was this post helpful? If yes, subscribe to our blog, follow us on social media, and check out our YouTube channel for more easy-to-follow budgeting tips.

Sources

- Photo: Unsplash: Thriday