Budgeting on one income can be tough for families because there’s no second paycheck to help fix mistakes. Even when families plan well, it’s easy for things to get out of sync. This pressure makes managing money feel heavier than it should.

When I helped manage my family’s finances during a time when I had the highest paycheck, we faced a big problem: our budget. You can only call it a budget on paper. It wasn’t really an effective budget that worked.

Our so-called budget ignored important timing, needed constant choices, and had no room for mistakes. Even though I was making enough money, we often ran out a few days before my next paycheck because of many budgeting mistakes. It was stressful—no thanks to that so-called budget I made during that time.

I don’t want that to happen to you. So in this post, I’ll share how to budget for a single-income family based on my experiences. Let’s dive in!

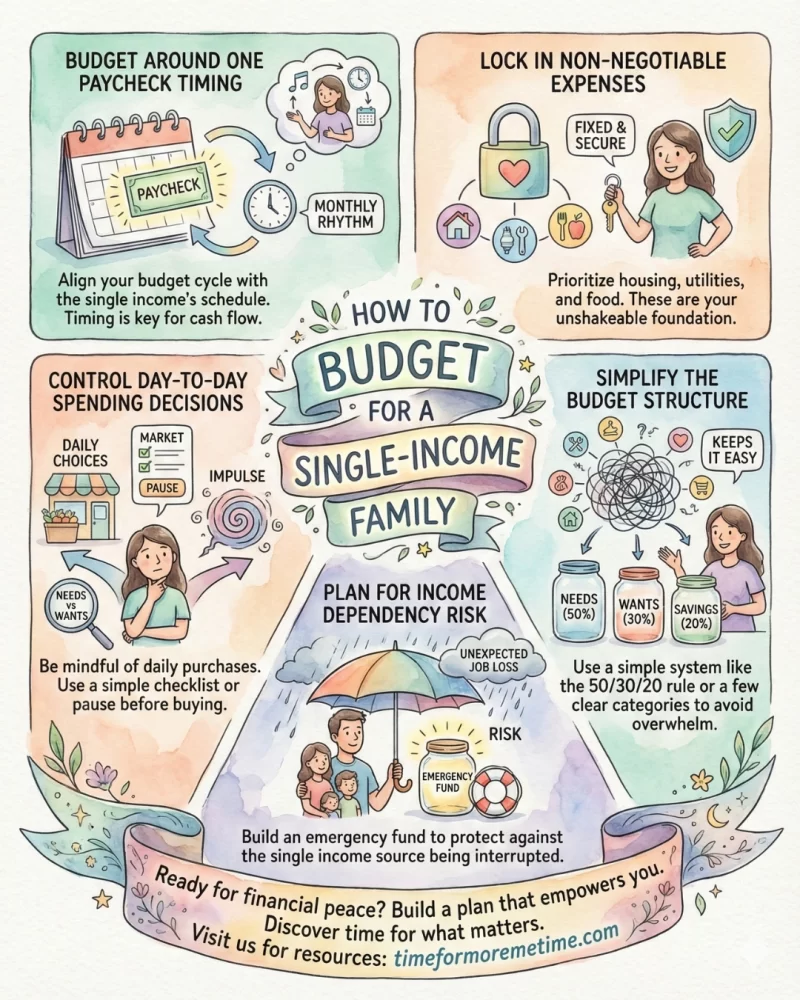

1. Budget Around One Paycheck Timing

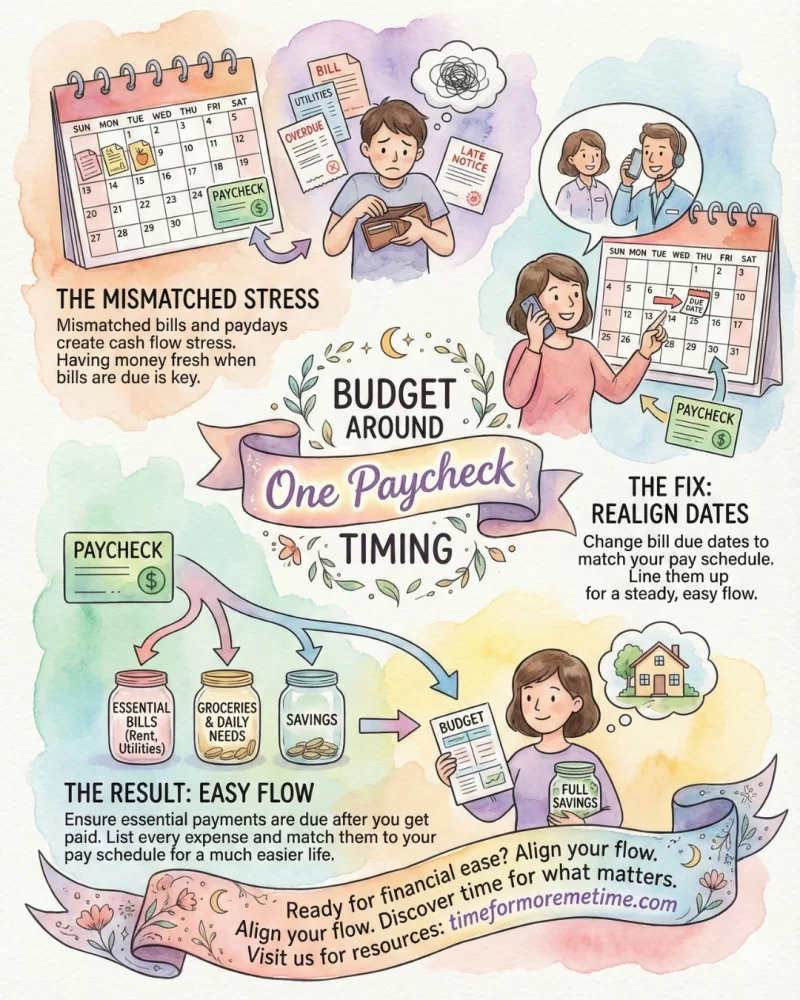

A budget works best when it matches your paycheck schedule. If your paycheck comes 15 days before your bills, it can create a lot of stress. It’s easier to pay bills when you have the money fresh from the ATM or bank. So, it’s important to line up your bills with your paydays to keep your cash flow steady.

In my experience, our bills were spread out over the month, but my income came at the end. Sometimes, it was late or not the full amount because I was freelancing and mostly contracting and some same day pay jobs on the side. This meant that rent, utilities, and groceries all needed money at the same time, which made things tough.

To fix this, I changed the due dates for bills and planned my spending around my paydays. This made life a lot easier. You can do the same. List every bill and expense and match them with your pay schedule. It’s best to have essential payments due after you get paid.

2. Lock In Non-Negotiable Expenses

A single-income budget works best when you take care of essential costs first. Housing, utilities, and childcare are key to daily life, so they shouldn’t compete with optional spending. By securing these expenses first, your budget will feel more stable.

This is important because many families already have little room to maneuver. About 42% of U.S. households live below what’s called the ALICE (Asset Limited, Income Constrained, Employed) threshold. People living below this threshold means they earn above the Federal Poverty Level but still cannot make ends meet.

To avoid getting yourself included in that statistic, list the expenses you can’t skip and use your income to pay them as soon as you get it. First, take care of these essential costs before spending on non-essentials. By locking in your needs early, your budget will hold together better and allow for smarter choices later.

3. Control Day-To-Day Spending Decisions

Daily spending choices are more important in a single-income household than many families realize. A few unplanned purchases during the week can affect what’s left for essentials. Without clear rules, these decisions can quietly add up.

Many families share on social media how they spend during times of mental fatigue or to feel better. This often means buying small things as a reward after a tough day, adding extras out of habit, or making purchases to avoid making another decision. These purchases might seem okay at the time, even if they weren’t planned.

The fix starts before these moments happen. Decide in advance how you’ll manage everyday spending so you’re not struggling with emotions versus the budget each time. Set limits, use a small allowance, or take a moment to pause before buying.

4. Simplify The Budget Structure

A single-income budget works better when it’s easy to understand and quick to use. Having too many categories, rules, or tools can create problems. A complicated budget is frustrating and hard to maintain, making it easy to stop checking it, even if the plan is good.

This isn’t just a problem for my family. I’ve seen it happen with close relatives too. They had budgets filled with dozens of details that looked organized but were exhausting to keep up with. Spending still happened, but they often delayed or skipped updates.

You don’t want that. So, simplify your budget to what you really need. Perform financial monitoring. Combine similar categories, limit special rules, and use one main tool. Keep your budget’s structure simple to make yourself and your family more likely to stick with it.

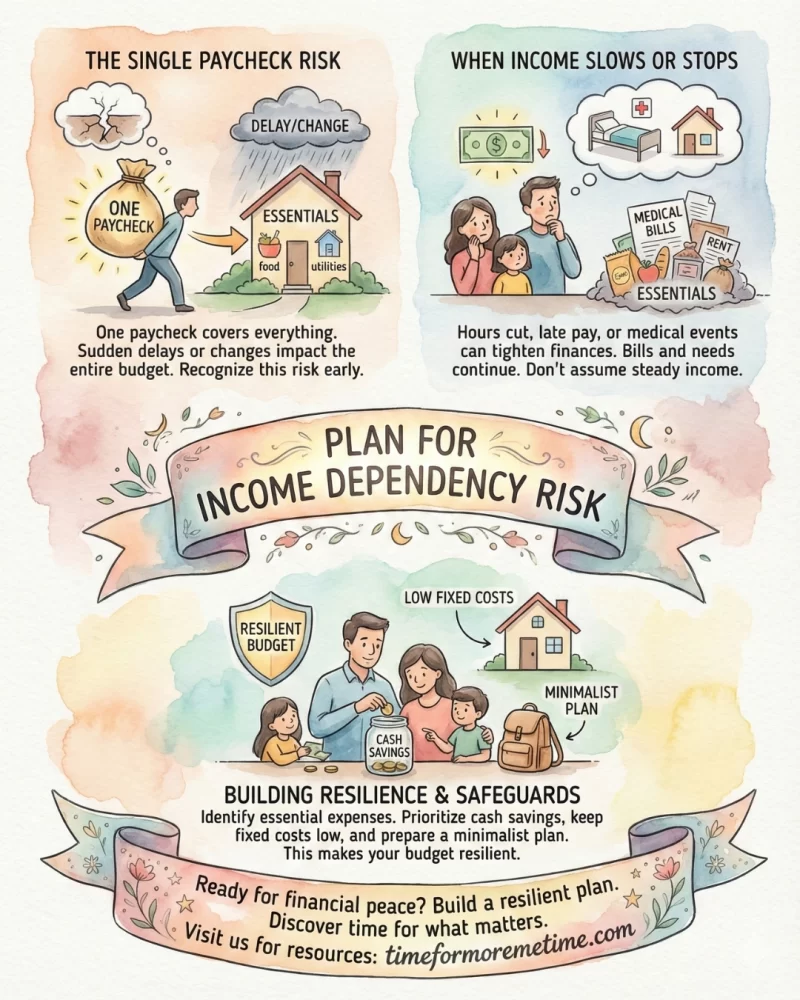

5. Plan For Income Dependency Risk

Having a single-income household often carries more risk. One paycheck has to cover everything, so a sudden delay or change in that income can impact your entire budget. Even if you work faster or do your job right compared to your coworkers, this may happen. So planning for this reality helps prevent stress from turning into panic.

Some people I’ve met shared how quickly their finances tightened when their hours were cut or paychecks were late. It doesn’t help that medical bills can pile up too. Even if you’re hospitalized, bills keep coming, and you still need to eat. This is true even if your paycheck is cut in half or arrives late. The key is to recognize this risk early and shape your budget around it. Don’t ever assume your income will stay steady.

So start by identifying what expenses need coverage if your income slows or stops. Add small safeguards to your budget, like prioritizing cash savings or keeping fixed costs low. Prepare to undergo minimalist lifestyle if money gets tight suddenly. This makes your budget more resilient and easier to trust each month.

Conclusion

Budgeting for a single-income family works best when the plan reflects how money actually moves and how decisions get made day to day. With these steps, you can create a budget that holds under pressure.

If this post helped clarify your approach, follow along and watch our YouTube videos for more practical posts like this one. Share it with someone budgeting on one income, and let me know which section made the biggest difference for you.

Source

Photo: Pexels: Tima Miroshnichenko