College debt continues to burden millions—but escaping it is possible with the right strategy. In this post, I’ll explain key options and innovative decision-making tools to help you eliminate student loans faster and more effectively. Let’s get started!

1. Use Income-Driven Repayment Plans

Income-driven repayment (IDR) plans can ease the burden of federal student loans by adjusting your monthly payments to match your income and family size. Options like Income-Based Repayment (IBR), Pay As You Earn (PAYE), and Saving on a Valuable Education (SAVE) are designed to keep payments affordable—sometimes as low as $0—and may lead to forgiveness after 20 or 25 years.

If you’re feeling broke or financially stretched, these plans offer breathing room without defaulting. Pair them with budgeting tools to monitor your cash flow, stay current on bills, and make better decisions while working toward long-term debt relief.

2. Apply For Forgiveness Programs

Federal loan forgiveness programs can help you eliminate student debt without paying the full balance—if you qualify. Options include Public Service Loan Forgiveness (PSLF) for government and nonprofit workers, Teacher Loan Forgiveness for educators, and Borrower Defense to Repayment for students misled by their schools.

These programs require consistent, on-time payments under a qualifying plan, so staying organized is key. If you’re juggling other bills or a credit card balance, forgiveness can be a lifeline that redirects money toward essentials. Always read the fine print, meet all eligibility requirements, and recertify annually to stay on track for debt cancellation.

3. Prepare For Policy Shifts And Plan Transitions

Student loan policy is changing fast, and staying ahead of those shifts can save you time, stress, and money. For example, the SAVE (Saving on a Valuable Education) plan is being phased out for new borrowers by mid-2026, and plans like RAP (Repayment Assistance Plan) may take its place. Interest resumed on federal student loans as of August 1, 2025, which could affect your monthly balance if you’re not prepared.

To avoid getting caught off guard, build flexibility into your budget using reliable budget-making strategies. Review updates from your loan servicer regularly, and be ready to switch plans if needed to keep your payments manageable and your progress on track.

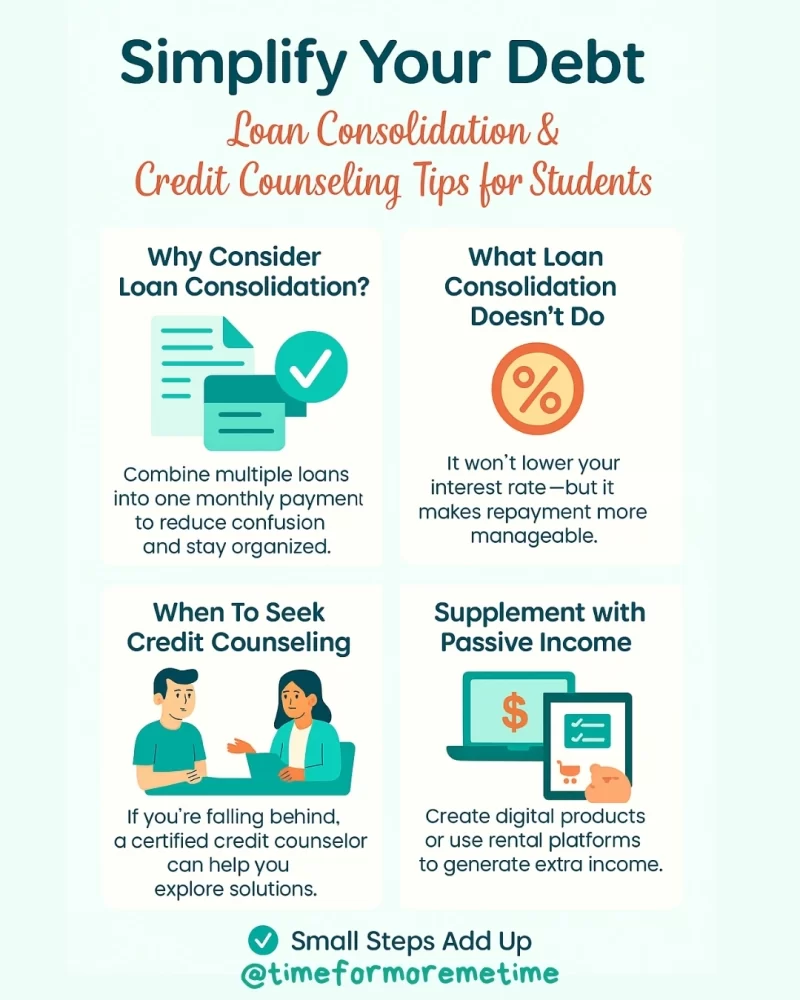

4. Consider Loan Consolidation Or Credit Counseling

If managing multiple student loans feels overwhelming, loan consolidation can help by combining them into one simplified monthly payment. While it won’t lower your interest rate, it can reduce confusion and improve your ability to stay on top of due dates. If you’re behind or facing more serious financial stress, working with a certified credit counselor can help you explore repayment strategies or negotiate with lenders.

To stay afloat while repaying loans, consider building passive income through simple, low-effort sources like digital products or rental platforms. Every extra dollar you earn or save helps speed up your journey out of college debt.

5. Choose A Payoff Method: Snowball Vs. Avalanche

Choosing a student loan payoff method can make a big difference in how fast—and how confidently—you escape debt. The snowball method focuses on paying off your smallest loan first, which builds momentum and motivation as you eliminate balances one by one. The avalanche method, on the other hand, targets the loan with the highest interest rate first to save the most money over time.

If you’re feeling broke or discouraged, the snowball approach may give you quick wins. But if you’re focused on long-term savings, the avalanche may be more efficient. Combine either method with side hustle ideas or bonus income to speed up your progress and stay motivated.

6. Set Up Autopay And Make Extra Payments When Possible

Setting up autopay is one of the easiest ways to stay consistent with your student loan payments—and many servicers offer a small interest rate discount when you do. It also helps prevent missed or late payments that can damage your credit score.

When you have extra money from tax refunds, bonuses, or even money-making apps, consider putting it toward your loan principal. Making extra payments—even small ones—can significantly reduce your total interest over time and help you get out of debt faster. Just be sure to instruct your servicer to apply extra payments to the principal, not future due dates.

7. Explore Side Hustles Or Passive Income To Supplement Payments

Supplementing your student loan payments with extra income can speed up your payoff timeline and reduce stress. Taking on a side hustle—like freelance work, tutoring, or delivery driving—gives you flexible ways to earn more without sacrificing your primary job.

If time is limited, consider building passive income through digital products, online courses, or affiliate marketing to generate money in the background. The key is to choose income streams that fit your schedule and skills. Every extra dollar you earn can go directly toward your loans, helping you escape college debt faster and with fewer interest charges over the long term.

Conclusion

Escaping college debt takes time, but the right strategies can make it feel possible—and even empowering. From income-driven repayment to forgiveness, budgeting, and side income, every step you take brings you closer to financial freedom.

If you found this post helpful, subscribe to our blog, follow us on social media, and check out our YouTube channel for more debt-busting tips.

Source

- Photo: Pexels: Mikhail Nilov