Before starting a family, money usually feels manageable. You pay your bills, you make plans, and most months things work out just fine. Because of that, it’s easy to assume your finances will simply adjust when life changes.

I’ve had conversations with friends who felt confident about their money right up until responsibilities started stacking up. Childcare costs showed up, income got tighter, and their old budgeting system stopped working much faster than they expected. The surprise wasn’t the expense itself but how quickly their setup failed.

They didn’t understand money basics, so their system fell apart. Without that understanding, your setup won’t hold either. To help you avoid the same problem, here are the essential money basics to build a steadier foundation before starting a family. Let’s get started!

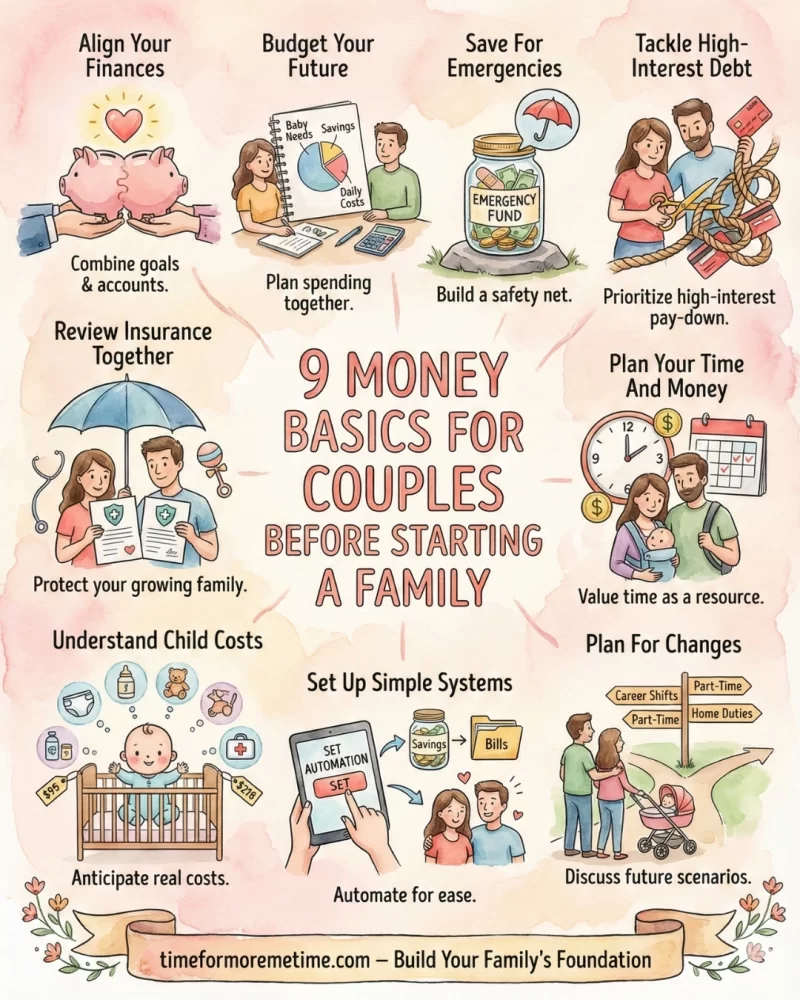

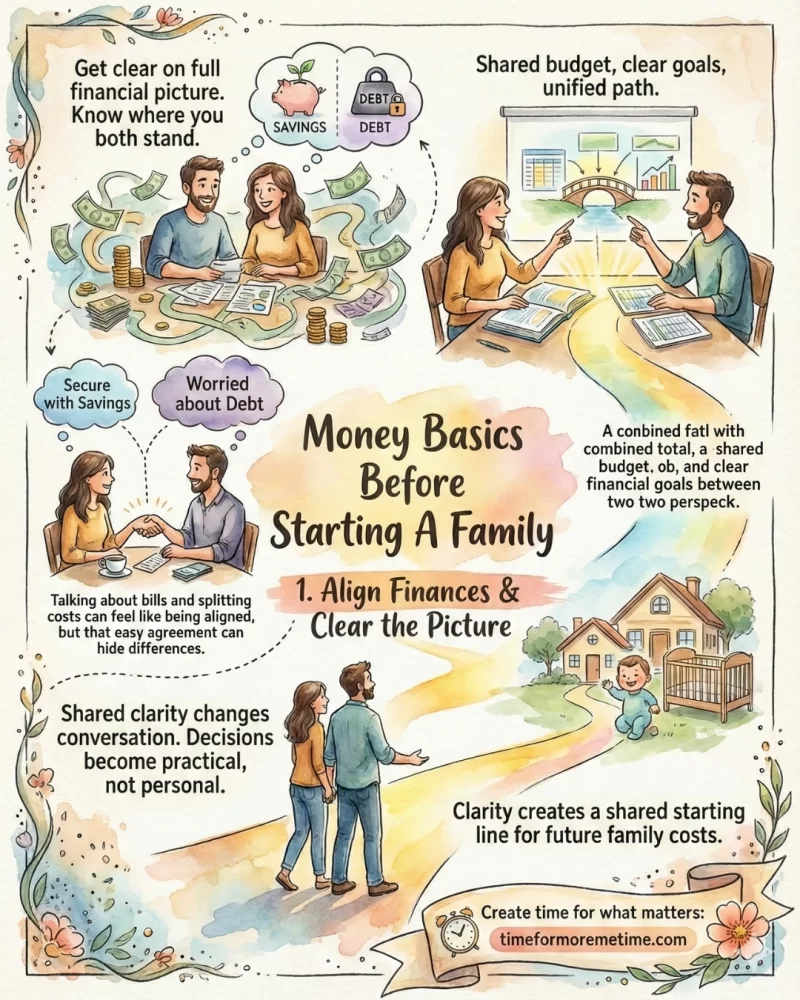

1. Align Your Finances

Get clear on where you both stand financially. Before starting a family, make sure you both know the full financial picture. Talking about bills and splitting costs can feel like being aligned, but that easy agreement can hide differences that only show up when bigger responsibilities arrive.

Partners often misjudge each other’s finances. One felt secure with savings; the other worried about debt—endlessly doing financial monitoring. Neither was wrong as they were just carrying different concerns. When they finally shared everything, the source of the tension became clear.

That moment of clarity usually changes the conversation. When both people understand the full picture, decisions stop feeling personal and start feeling practical. Getting clear early doesn’t fix everything, but it creates a shared starting line before family costs begin to grow.

2. Budget Your Future

Build a budget that fits the life you want. If your spending feels different even though nothing obvious changed, your budget may still balance but no longer matches your priorities or comfort level. Adjust categories and targets so your plan feels right again.

I remember a friend laughing about how they hadn’t changed their lifestyle, yet money seemed to disappear faster. As we talked it through, it became clear that life had quietly shifted. More appointments, more convenience spending, and fewer low-cost days were filling the calendar. None of it stood out on its own, but together it changed how the budget behaved.

That’s the part many couples miss. A budget built for today won’t always fit tomorrow without small adjustments along the way. Across the US, almost half of families reported that a growing share of household income is absorbed by housing and childcare, leaving limited room for savings, food, or unexpected costs. As those fixed expenses rise, financial pressure builds even when income stays the same.

3. Save For Emergencies

Emergency savings are easy to agree with in theory. In practice, we often push them to the back burner when income feels steady and nothing urgent is happening. It’s one of those things couples mean to circle back to later.

I’ve seen people realize how exposed they were only after life slowed them down a bit. An unexpected pause in income or a larger-than-usual expense didn’t ruin anything outright, but it changed the tone of every decision. Bills that were once routine suddenly require people to put extra thought into them. If they don’t have a cushion, even small choices feel heavier than usual.

That experience is more common than many expect, as many US households can barely cover three months of expenses with savings. An emergency fund doesn’t solve problems on its own, but it buys time, and that breathing room often keeps temporary setbacks from turning into lasting stress.

4. Tackle High-Interest Debt

You must deal with high-interest debt fast and early. Debt has a way of blending into everyday life, especially when payments feel manageable. As long as balances move slowly in the right direction, it’s easy to assume everything is under control. That sense of comfort can change once new responsibilities enter the picture.

Many of my childhood friends only realized during family planning how much of their monthly cash flow was already claimed. Small credit card balances started to limit choices and flexibility evaporated faster than expected. The debt didn’t balloon overnight, but its burden felt heavier once other priorities needed space.

That shift is backed by the numbers, where average credit card interest rates in the US remain above 20%. I also felt this when interest quietly eats into income each month, leaving less space to absorb future costs. But when you reduce high-interest debt early, it often restores options that families don’t realize they’re losing.

5. Review Insurance Together

Together, you need to review and check your health and insurance premium. Insurance is easy to push aside when life feels stable. As long as everyone is healthy, it can feel like paperwork that doesn’t need much attention. That mindset tends to change once you’ve seen how quickly health situations can shift.

Working as a dosimetrist, I’ve seen how medical needs can escalate without much warning. Treatment plans evolve, follow-up care adds up, and what starts as a manageable situation can stretch longer than expected. Watching that happen up close makes it clear how exposed families can feel when coverage hasn’t been reviewed in a while.

That perspective carries over at home. When couples take time to understand what their insurance actually covers and where the gaps might be, they’re better prepared for situations they can’t predict. We can’t make health issues easier, but we can remove one layer of financial uncertainty when decisions already feel heavy.

6. Plan Your Time And Money

Include time in your financial planning. Often, financial planning focuses on numbers and monthly utility costs. However, know that time plays just as big a role once family life begins. Work schedules, commuting, appointments, and household responsibilities all start affecting spending in ways couples don’t always expect.

People online say they didn’t expect how much unpaid work would appear when routines change. One partner cut work hours. The other did more at home. At first, each change seemed small. As time got tight, they spent more on convenience. Paying for ease felt like the quickest way to keep up.

Couples can prevent that disconnect by thinking ahead about schedules and workload. When you consider how time pressure influences spending, financial decisions feel easier to explain later. Planning for time alongside money creates a clearer picture of what your family life will actually cost.

7. Understand Child Costs

Many couples delay thinking about the cost of raising children because it feels overwhelming. The numbers sound big, the timelines feel far away, and it’s easier to assume things will work themselves out as they come and live below your means if needed.

I heard this from patients who thought they planned well. They counted childcare and felt ready, but small costs kept coming. Clothes needed replacing sooner. Activities became routine earlier. Doctor visits piled up. Each cost felt reasonable alone, but together they made the monthly budget much heavier.

That’s where awareness helps. When you expect family costs to build gradually instead of arriving all at once, it’s easier to adjust without feeling caught off guard. Couples who approach it this way tend to feel steadier as family spending expands, even when plans change along the way.

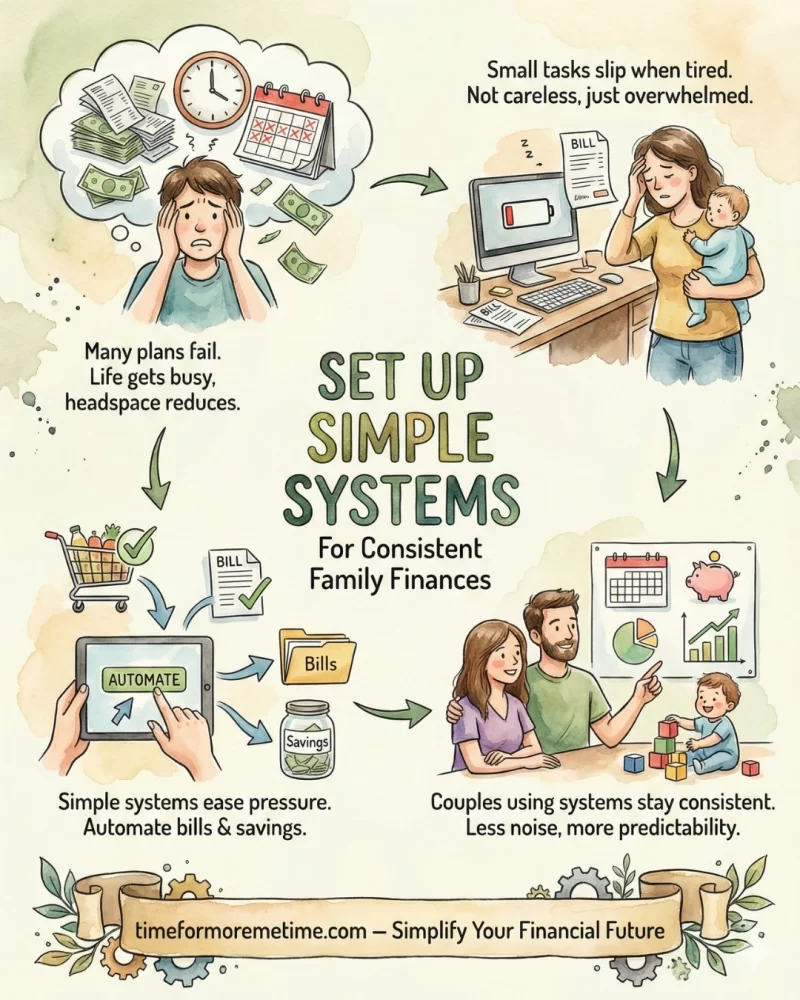

8. Set Up Simple Systems

Set up your money system early and keep it simple. This is where many plans fail. You may plan to pay bills on time, save extra cash, and watch your spending. That works for a while. Then life gets busier and you have less headspace, and it all falls apart.

People often try to manage money by hand when life gets busy. This doesn’t mean they were careless. Usually they are tired from work and family duties. So they put off small tasks like moving money or tracking spending. Over time, things slip—not because they don’t care, but because there is too much to remember.

Simple systems make a big difference. When I automate bills and keep my grocery savings in check, I ease the pressure. Money moves without constant decisions. Couples who use systems—not memory alone—stay more consistent. This helps when family life gets louder and less predictable.

9. Plan For Changes

Prepare for the unexpected. Paychecks can be late, and you might face unpaid time off. Income seems steady until it isn’t. Before starting a family, it’s easy to assume pay keeps coming on schedule and at the same amount. That assumption often gets tested sooner than you expect.

Short delays and unpaid days can cause big problems. Your parental leave might last longer than you expect. Your work hours might be cut for a while. Returning to work may not go as planned. Even if these changes are temporary, they can change your cash flow enough to make your budget feel unfamiliar.

Thinking through those shifts ahead of time helps soften the landing. When you plan for periods of reduced income or time away from work, the adjustment feels intentional instead of reactive. Couples who prepare for these transitions tend to move through them with less stress, even when plans need to change along the way.

Conclusion

Starting a family changes how money behaves. Planning ahead doesn’t remove uncertainty, but it makes it manageable, strengthening stability and reducing stress when life starts moving faster.

If you want more practical guidance on building strong financial habits, read our latest posts, follow us on social media, and visit our YouTube channel for clear advice you can apply with confidence.

Source

- Photo: Pexels:

Jacob Yavin